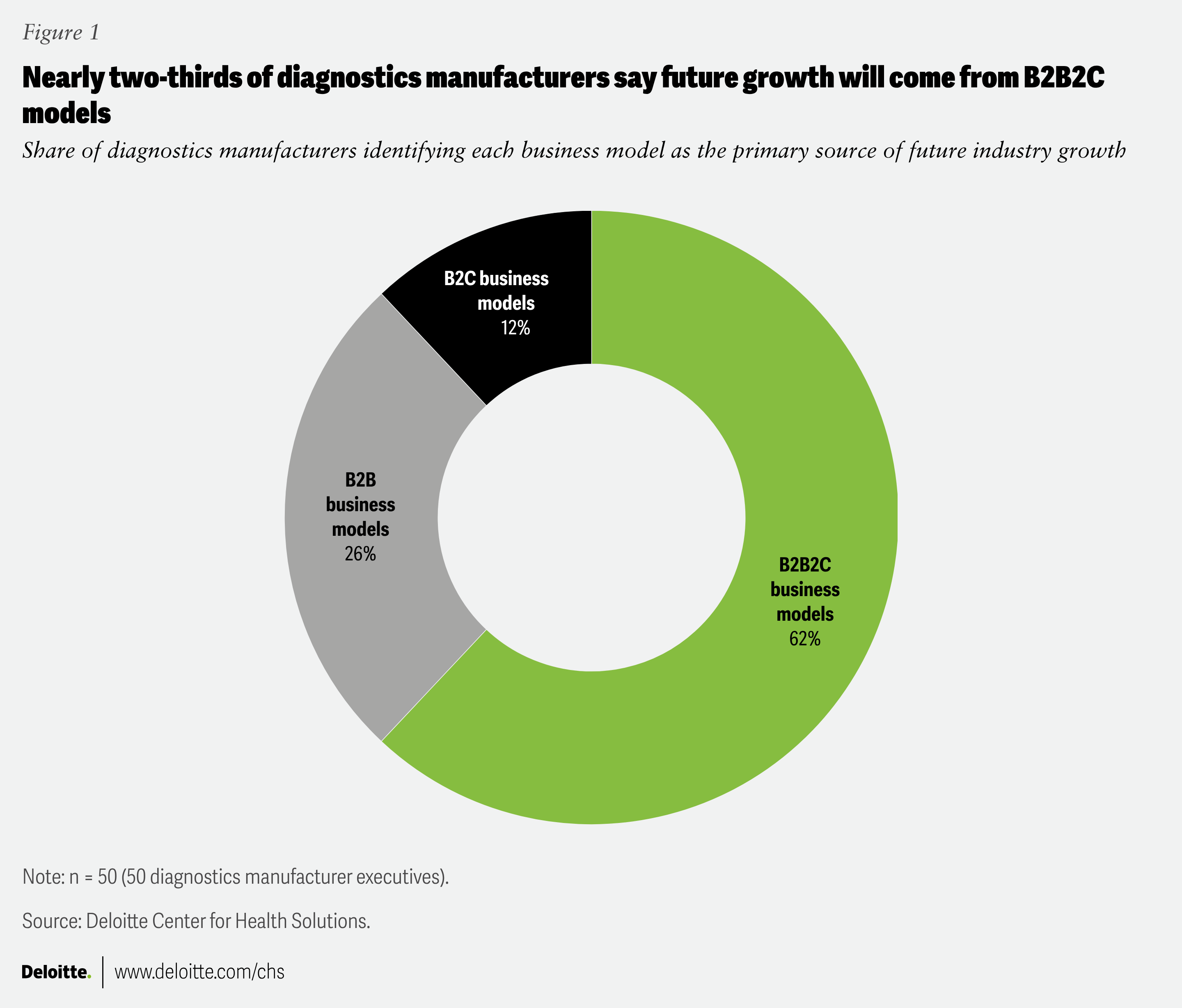

In the rapidly shifting landscape of modern medicine, a significant divide has emerged between those who manufacture diagnostic tools and the healthcare providers who rely on them to treat patients. As the industry grapples with the rise of home-based testing and digital health tools, a new analysis from the Deloitte Center for Health Solutions highlights a critical misalignment: diagnostics manufacturers are struggling to pivot toward a business-to-business-to-consumer (B2B2C) operational model, a transition that 62% of executives in the sector now view as essential for future growth.

This strategic gap is not merely a matter of corporate preference; it represents a fundamental friction in how care is delivered. While manufacturers have historically focused their innovation efforts on the accuracy of result interpretation, healthcare providers—the individuals on the front lines of patient care—report that the actual process of ordering tests remains their single greatest operational hurdle. As patients increasingly demand a more consumer-centric experience, the inability of manufacturers to integrate with existing clinical workflows threatens to leave both parties behind in an era defined by rapid technological disruption.

The Growing Chasm: Manufacturing vs. Clinical Reality

The global diagnostics sector is undergoing a profound transformation. Patients are no longer passive recipients of care; they are increasingly utilizing virtual health portals, direct-to-consumer testing, and wearable devices to monitor their own biological data. This “consumerization” of health is forcing traditional providers—such as hospital systems and independent laboratories—to adapt or risk losing patients to more agile, tech-forward competitors. However, the data suggests that manufacturers are not yet fully synchronized with the needs of these providers.

The research, which surveyed 50 diagnostics manufacturer executives and 50 healthcare provider executives, reveals that while 76% of providers believe consumer-initiated testing will fundamentally alter the market within three years, the support systems required to facilitate this shift are currently lacking. A staggering 74% of providers report that their backend database systems remain entirely un-integrated, creating “data silos” that prevent a seamless, end-to-end diagnostic journey. For manufacturers, the path forward requires moving beyond the role of a traditional product vendor and becoming a true workflow partner.

Addressing the Three Core Disconnects

To successfully transition to a B2B2C model, manufacturers must address three primary areas where their current strategies fail to align with the realities of clinical practice. The first is the problem-solving disconnect. Manufacturers often prioritize the science of the test, but providers are calling for better software solutions that simplify the ordering process. Without automated, intuitive interfaces, the friction of daily clinical operations remains a significant barrier to the adoption of new technologies.

Second, there is a clear stakeholder disconnect. Many manufacturers continue to direct their engagement efforts toward hospital procurement offices—the traditional gatekeepers of contract negotiation. Yet, providers emphasize that the real drivers of long-term product adoption are ordering clinicians, lab directors, and service-line leaders. By focusing solely on the procurement department, manufacturers may be missing the particularly people who dictate how diagnostic tools are used in practice.

Finally, the engagement disconnect highlights a mismatch in communication styles. While manufacturers continue to rely heavily on field sales teams to push their products, providers indicate that they prefer peer-to-peer clinical education, medical conferences, and digital self-service portals. The current sales-heavy approach is often viewed by clinicians as overly frequent and lacking in the clinical value necessary to justify their time.

The Role of AI and Digital Interoperability

The future of diagnostics lies in the ability to create “interoperable moats”—digital ecosystems that connect disparate systems and provide clinicians with a longitudinal view of patient health. As testing moves from the clinic into the home, the need for platform-integrated Artificial Intelligence (AI) becomes paramount. Rather than offering standalone algorithms, manufacturers that embed their technology directly into Electronic Health Record (EHR) workflows will be better positioned to support the modern, distributed care network.

Currently, the fragmentation of the tech stack is a major impediment. With 66% of provider executives identifying personalized workflow integration as a top priority for the next three to five years, the demand for manufacturers to provide “actionable next steps” rather than just raw data is clear. Consumers, empowered by their own wearable devices, expect visual and contextually relevant results. Manufacturers that fail to integrate their products into these automated, patient-centered loops risk being relegated to the status of commodity vendors, losing both their influence over diagnostic decisions and their visibility into the changing consumer landscape.

Key Takeaways for the Diagnostics Industry

- Prioritize Workflow over Product: Focus innovation on solving the clinical friction associated with test ordering, not just result interpretation.

- Engage the Right Stakeholders: Shift focus from procurement offices to the clinicians and lab directors who directly influence product utilization.

- Modernize Communication: Move away from high-frequency sales visits toward digital, peer-to-peer, and evidence-based clinical education.

- Integrate AI into EHRs: Embed diagnostic tools directly into existing digital workflows to ensure seamless data interoperability.

- Embrace the B2B2C Model: Recognize that the consumerization of healthcare is a permanent shift, and align business strategies to support providers in this new environment.

As the healthcare sector continues to evolve, the ability of diagnostics manufacturers to bridge these gaps will likely determine their long-term viability. The transition to a more integrated, consumer-facing model is not optional; it is a fundamental requirement for those looking to thrive in an increasingly data-driven, patient-centered, and digitally connected global health market.

For further developments on how digital health standards and interoperability mandates are shaping the future of clinical diagnostics, stay tuned to the World Today Journal. We will continue to track the latest industry reports and policy shifts as they emerge. Have thoughts on how your clinic is managing these changes? Share your experiences in the comments below.

Worth a look