Worldline, Crédit Agricole, and Mastercard are collaborating on a pilot program to deploy agentic payment systems—where digital agents autonomously execute transactions based on predefined user criteria. The initiative, announced this month, marks a significant step toward AI-driven financial automation, with potential to reshape how consumers and businesses interact with banking services. According to a joint statement from the three companies, the pilot will allow users to delegate specific payment tasks to AI agents, such as managing event budgets or subscription renewals, without manual intervention. The program builds on Mastercard’s existing work in AI-driven payments and Worldline’s expertise in transaction processing, while Crédit Agricole brings its extensive retail banking network to the test.

This development comes as financial institutions increasingly experiment with generative AI and autonomous systems to streamline operations. While still in early stages, the pilot could offer a glimpse into how agentic technology—where AI acts on behalf of users—might transform everyday banking. For now, the focus remains on controlled testing, with no immediate plans for widespread consumer rollout.

Here’s what we know about the pilot, its technical underpinnings, and the broader implications for digital finance.

How the Agentic Payments Pilot Works

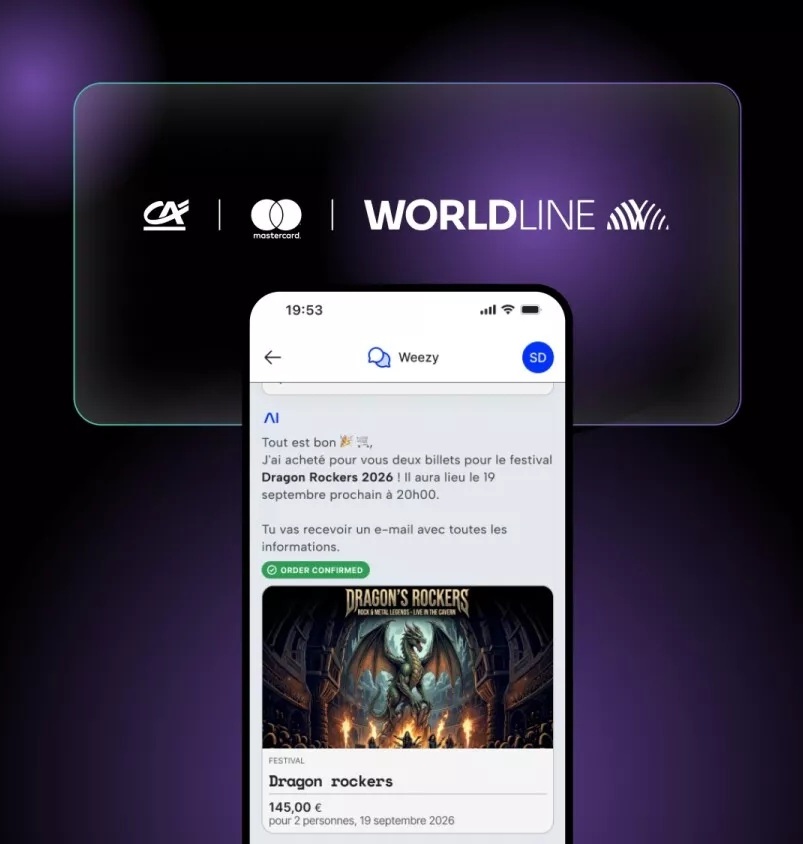

The pilot leverages AI agents to handle transactions autonomously, based on rules set by the user. For example, a festival-goer could delegate budget management to a digital agent, which would then handle ticket purchases, transport bookings, and merchant payments—all while adhering to a predefined spending limit. This approach contrasts with traditional payment systems, where users manually authorize each transaction.

Mastercard has previously explored similar concepts through its AI-driven payment solutions, including partnerships with AI startups like AI21. Worldline, a European leader in payment processing, brings its infrastructure expertise, while Crédit Agricole’s retail banking footprint ensures real-world applicability. The pilot is expected to run through late 2024, with results to be analyzed for potential broader adoption.

According to a Worldline press release, the technology will initially focus on controlled environments, such as corporate expense management and event planning, before expanding to other use cases.

Why This Matters: The Rise of Agentic Banking

Agentic payments represent a shift from passive transaction processing to proactive financial management. Unlike traditional AI chatbots or rule-based automation, these systems operate with a degree of autonomy, making decisions in real time based on user preferences and contextual data. This aligns with broader trends in AI-driven enterprise automation, where businesses are increasingly relying on autonomous agents to handle complex tasks.

For consumers, the potential benefits include reduced friction in managing finances—imagine an AI agent automatically adjusting subscriptions based on income fluctuations or canceling unused services. For businesses, agentic systems could streamline expense reporting and vendor payments. However, the pilot also raises questions about regulatory oversight and cybersecurity risks, as autonomous agents interact with financial systems.

Crédit Agricole’s involvement is particularly notable, as the French banking group has historically been cautious about rapid digital transformation. Its participation signals growing confidence in AI’s role in retail banking, even as the sector grapples with EU regulatory scrutiny over AI in financial services.

Key Players and Their Roles

- Worldline: Provides the payment infrastructure and transaction processing capabilities. As a subsidiary of Atos, Worldline operates in over 40 countries, handling billions of transactions annually. Its expertise in secure payment networks is critical to ensuring the pilot’s scalability.

- Crédit Agricole: Acts as the retail banking partner, offering real-world testing through its customer base. The bank’s focus on sustainable finance could also influence how agentic systems prioritize transactions, such as favoring eco-friendly merchants.

- Mastercard: Brings its global payment network and AI research, including collaborations with firms like AI21. Mastercard’s recent AI initiatives position it as a leader in integrating machine learning with financial services.

The collaboration also reflects a broader industry trend: financial institutions are increasingly partnering with tech firms to accelerate innovation. For example, JPMorgan Chase’s AI-driven fraud detection and Bank of America’s AI chatbot, Erica, demonstrate how banks are adopting AI to enhance customer experiences.

What Happens Next: Timeline and Next Steps

The pilot is expected to conclude by the end of 2024, with findings to be shared in early 2025. If successful, the partners may expand the program to additional use cases, such as:

- Automated expense management for small businesses.

- Dynamic budgeting for personal finance (e.g., adjusting spending based on income cycles).

- Integration with open banking APIs to pull real-time financial data.

Regulatory approval will be a key hurdle. The EU AI Act, set to take full effect in 2025, imposes strict requirements on high-risk AI systems, including those used in financial services. The pilot’s results will likely influence how the partners navigate compliance, particularly around transparency and user consent.

Mastercard has previously stated that it expects AI-driven payments to become mainstream within the next five years, provided regulatory frameworks adapt accordingly. Worldline’s CEO, Philippe Jamet, has emphasized that the pilot is a step toward “democratizing access to intelligent payment solutions.”

FAQ: Agentic Payments Explained

Q: What is an agentic payment system?

An agentic payment system uses AI to autonomously execute transactions based on predefined rules. Unlike traditional payments, where users manually approve each step, agentic systems act on behalf of the user, making decisions in real time (e.g., adjusting a budget for an event).

Q: How secure are agentic payments?

Security is a top priority for the pilot. Worldline and Mastercard’s existing fraud prevention tools will be integrated, alongside Crédit Agricole’s banking-grade encryption. However, as with any AI system, there are risks of adversarial attacks or unintended behaviors—hence the controlled testing phase.

Q: Will this be available to consumers soon?

Not immediately. The pilot is focused on controlled environments, with no timeline yet for consumer rollout. Even if expanded, adoption would depend on regulatory approval and technical refinements.

Q: How does this differ from existing AI in banking?

Most AI in banking today is reactive—e.g., fraud alerts or chatbots. Agentic systems are proactive: they don’t just analyze data but act on it. For example, an AI agent could automatically book a train ticket if weather forecasts predict delays, whereas today’s systems would only notify the user.

Broader Implications for Digital Finance

The pilot underscores a fundamental shift in financial services: from transactional to advisory. As AI agents become more capable, the line between banking and personal assistance may blur. For instance:

- Personal Finance: AI could manage savings goals, investment allocations, and even tax optimization—effectively acting as a digital financial advisor.

- Corporate Payments: Businesses could delegate vendor payments, expense approvals, and even supply chain financing to autonomous agents.

- Cross-Border Payments: Agentic systems might optimize currency conversions and payment routing in real time, reducing fees for international transactions.

However, challenges remain. The IMF has warned that AI in finance could exacerbate inequality if not designed inclusively. Additionally, the UK Financial Conduct Authority (FCA) has highlighted concerns over AI bias and explainability in financial decision-making.

For now, the Worldline-Crédit Agricole-Mastercard pilot serves as a case study in how financial institutions can experiment with agentic technology while mitigating risks. The results will likely influence whether other banks follow suit—or whether regulators impose stricter guardrails before widespread adoption.

Next Steps: What to Watch

The next confirmed checkpoint is the public release of pilot findings in early 2025, which will detail performance metrics, user feedback, and technical lessons learned. Key dates to monitor:

- Q4 2024: Completion of pilot testing phase.

- Q1 2025: Expected publication of results and next steps.

- 2025–2026: Potential regulatory submissions for broader deployment (timing dependent on EU AI Act compliance).

In the meantime, financial institutions and tech partners are encouraged to share their perspectives. Worldline, Crédit Agricole, and Mastercard have not yet confirmed plans for public demonstrations, but industry observers expect updates as the pilot progresses.

This collaboration marks a pivotal moment in financial technology. As AI agents move from theory to practice, the question for consumers and businesses alike is not if agentic payments will arrive—but how soon.

Have questions or insights on agentic payments? Share your thoughts in the comments below or reach out to our Business team for further analysis.