Homeowners facing damages from severe weather, flash floods, and heavy rain must distinguish between different insurance categories to determine if they will receive payouts, as standard policies often exclude specific types of water ingress. According to the German Insurance Association (GDV), while storm and hail damage are typically covered under building insurance, “elementary damages” such as floods and heavy rainfall require specific additional coverage known as Elementarschadenversicherung.

The distinction between “piped-in water” (Leitungswasser) and “natural hazards” (Elementarschäden) is the primary point of legal contention in insurance claims. Building insurance generally covers water that escapes from a burst pipe inside the home, but it does not cover water that enters from the outside via surface runoff or groundwater rise unless the policyholder has explicitly added an elementary hazards rider.

This gap in coverage becomes critical during “Starkregen” (heavy rain) events, where water accumulates on the surface and flows into basements. In these cases, insurers may argue the damage was caused by insufficient drainage or a lack of preventative measures, leading to disputes over whether the event was an “unavoidable natural disaster” or a result of negligence.

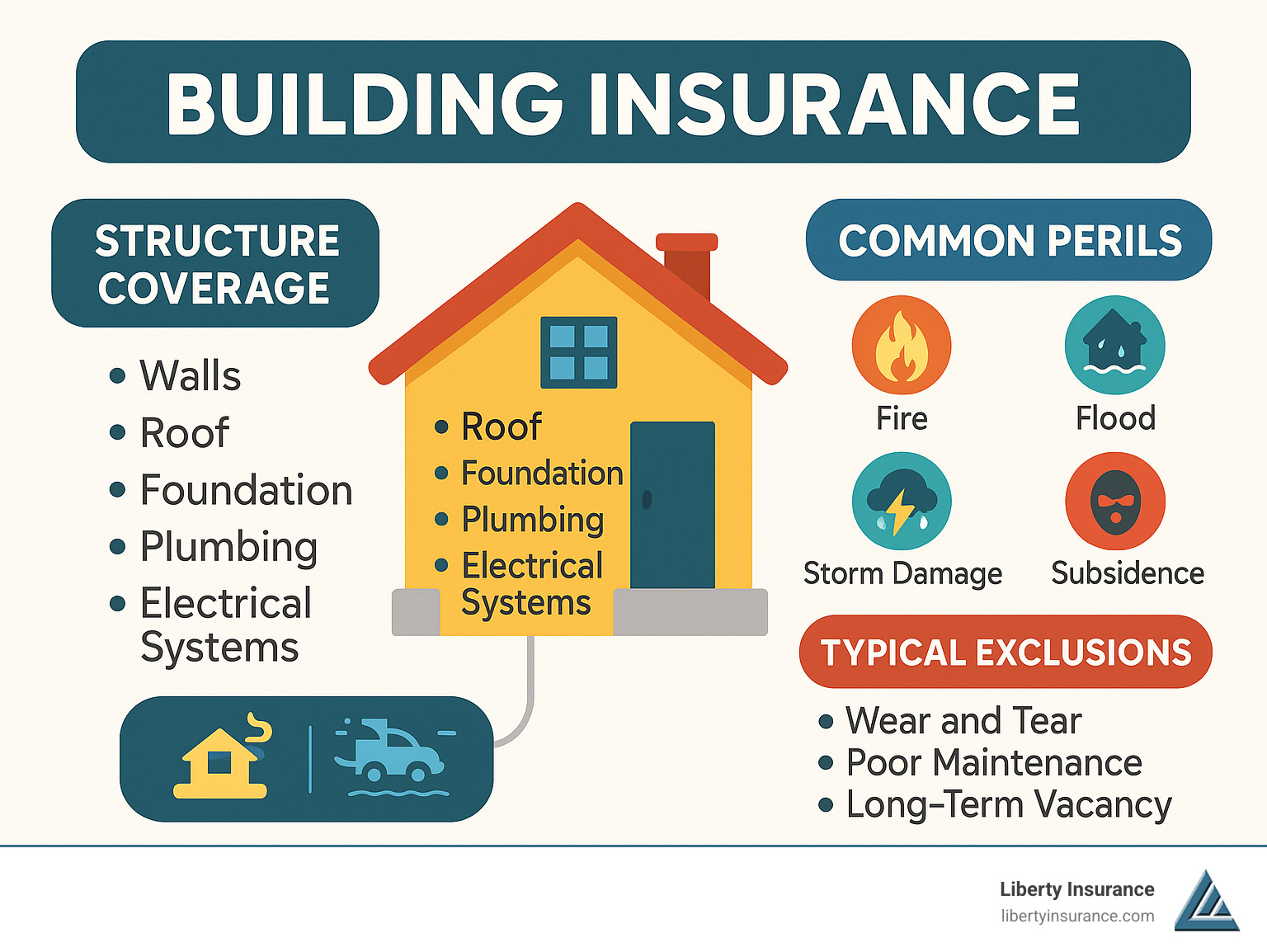

What does building insurance actually cover during a storm?

Standard building insurance (Wohngebäudeversicherung) typically covers “storm and hail” damage, but only when the weather reaches a specific intensity. Under German industry standards, a “storm” is generally defined as wind speeds exceeding 80 km/h (approximately 50 mph). If wind speeds are lower, insurers may classify the event as a “strong breeze,” which might not trigger a full payout for certain types of structural damage, according to GDV guidelines.

Coverage usually extends to the roof, windows, and external walls if they are damaged by flying debris or wind pressure. However, if rain enters the home through a window that was left open or a roof that was already in a state of disrepair, the insurer may deny the claim based on a failure to maintain the property. The German Insurance Association (GDV) emphasizes that the “cause-and-effect” relationship must be clearly documented to ensure a successful claim.

Water damage from pipes (Leitungswasserversicherung) is a separate pillar. This covers the cost of repairing the pipe and the resulting damage to the building’s fabric, such as soaked drywall or ruined flooring. It does not, however, cover the contents of the home; that falls under the remit of household contents insurance (Hausratversicherung).

Why is “Elementary Damage” insurance different from standard policies?

Elementary damage insurance is an optional extension that covers specific natural perils: floods, heavy rain, groundwater rise, earthquakes, and landslides. Without this rider, a homeowner whose basement is flooded by a river overflowing its banks or by rainwater flooding a street will likely receive no compensation from their building insurance provider.

The legal complexity arises during “heavy rain” (Starkregen) events. Unlike a river flood, heavy rain causes water to pool on the surface and seep into buildings through cracks in the foundation or via the sewage system. Insurers often scrutinize whether the water entered through “backflow” (Rückstau) from the sewer. If the homeowner failed to install a required non-return valve (Rückstauklappe), the insurer may reduce the payout or deny it entirely, citing a breach of the duty to mitigate risk.

For those living in designated flood-risk zones, the cost of this insurance is higher, and some providers may refuse coverage entirely if the property is located in a high-risk area (HQ100 zone, meaning a flood that occurs on average once every 100 years). The German Environment Agency (Umweltbundesamt) provides flood risk maps that insurers use to calculate these premiums and determine eligibility.

How to handle a claim after a natural disaster

The immediate aftermath of a storm or flood is the most critical period for securing a payout. Insurers require “mitigation of loss” (Schadensminderungspflicht), meaning the homeowner must take reasonable steps to prevent further damage. This includes pumping out water or covering a hole in the roof with a tarp.

Documentation is the cornerstone of any successful insurance claim. Experts recommend the following steps:

- Photographic Evidence: Take detailed photos and videos of the water levels, the point of entry, and all damaged items before beginning cleanup.

- Detailed Lists: Create an inventory of damaged furniture, electronics, and structural elements.

- Professional Assessment: In cases of disputed causes (e.g., whether water came from a pipe or the street), hiring an independent certified surveyor (Sachverständiger) can provide the necessary evidence to counter an insurer’s denial.

- Timely Notification: Claims must be reported “without undue delay.” Waiting several weeks to notify the insurer can lead to a reduction in benefits.

Comparing the three main types of water-related coverage

Understanding the difference between these coverages prevents the common mistake of assuming “water insurance” covers all scenarios. The following table outlines the primary distinctions:

| Coverage Type | What it Covers | What it Excludes |

|---|---|---|

| Building Insurance (Standard) | Storm (>80km/h), Hail, Fire | Surface water, Floods, Groundwater |

| Piped-in Water (Leitungswasser) | Burst pipes, Leaking joints | Rainwater entering through walls/windows |

| Elementary Damage (Optional) | Flash floods, Heavy rain, Earthquakes | General wear and tear, Lack of maintenance |

What happens if the insurer denies the claim?

When an insurer denies a claim, they usually cite one of three reasons: the event was not covered by the policy, the damage was caused by “gross negligence” (e.g., ignoring a known leak for years), or the damage is below the deductible (Selbstbeteiligung).

If a homeowner believes the denial is unjustified, the first step is to request a written statement of reasons. Under German law, the burden of proof often shifts depending on the type of damage. For elementary hazards, the policyholder must prove the event occurred and caused the damage. If the insurer claims the damage was caused by a lack of maintenance, the insurer must provide evidence of that deficiency.

Legal recourse typically involves an appeal to the insurance ombudsman (Versicherungsombudsmann), a free arbitration service that mediates between consumers and insurance companies. If arbitration fails, the matter can be taken to civil court. In these cases, the court will often appoint its own independent expert to determine whether the water entered the building via a “natural hazard” or a “structural failure.”

The next critical checkpoint for homeowners is the annual review of policy limits. As climate patterns shift and “extreme weather” becomes more frequent, the Federal Network Agency and other regulators continue to monitor infrastructure resilience, which may influence future insurance mandates and premium adjustments for high-risk regions.

Do you have experience disputing a weather-related insurance claim? Share your insights in the comments below.