The landscape of medical innovation is currently experiencing a stark divergence. While the overall volume of capital flowing into the sector remains significant, the distribution of those funds has turn into increasingly top-heavy, creating a “winner-take-all” dynamic that favors a handful of established giants over the broader startup ecosystem.

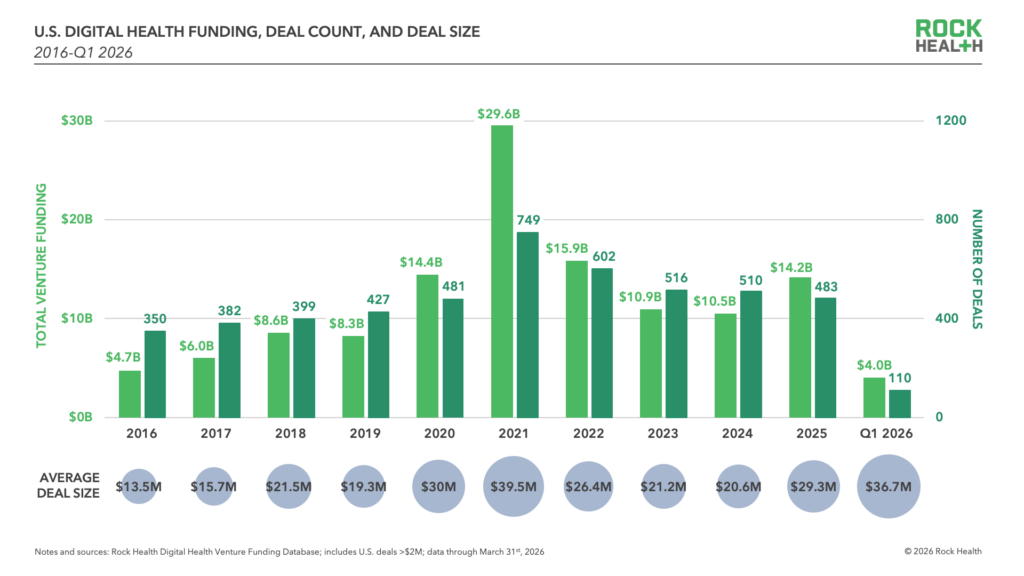

In the first quarter of 2026, U.S. Digital health funding reached $4.0 billion across 110 deals, according to a report from Rock Health. While this represents the strongest first quarter since the pandemic peak, the average deal size of $36.7 million masks a deeper trend: a massive concentration of capital among a tiny elite of companies.

This digital health funding consolidation is creating a bifurcated market. Nearly 60% of the total quarterly funding was captured by just 12 companies that secured “mega deals” of $100 million or more. This leaves the remainder of the industry to compete for a fraction of the available capital, signaling a shift in investor appetite toward proven scale rather than early-stage experimentation.

As a physician and journalist who has spent over a decade navigating the intersection of internal medicine and medical innovation, I view this trend as a maturation of the market. We are moving away from the “growth at all costs” era and into a period defined by clinical integration and operational discipline.

The Rise of the Mega-Deal and the Startup Squeeze

The disparity in funding is most evident when looking at the specific entities attracting nine-figure checks. Companies such as Whoop ($575 million), Verily ($300 million), OpenEvidence ($250 million), and Talkiatry ($212 million) are dominating the capital flow. For these organizations, the influx of cash allows for aggressive expansion and the ability to weather macroeconomic volatility.

For the average founder, however, the environment is increasingly precarious. When a small group of companies absorbs the majority of available funding, the “middle class” of digital health startups finds it harder to secure the series A and B rounds necessary for survival. This creates a high-pressure environment where only those with exceptional clinical outcomes or clear paths to profitability can thrive.

The funding gap is further complicated by a stagnant exit market. The window for Initial Public Offerings (IPOs) remains narrow. High-profile companies like Hinge Health and Omada Health are reportedly biding their time, prioritizing financial discipline over a rushed public debut. This lack of liquidity means that venture capital is staying locked in for longer, further concentrating wealth in the top tier of private companies.

AI as the New Healthcare Operating System

Perhaps the most significant shift in the current investment climate is the conceptual evolution of Artificial Intelligence. In previous years, “AI-enabled” was a category used to attract investors. Now, AI has become “table stakes”—a fundamental requirement rather than a differentiator.

Investors are no longer funding companies simply because they use AI. Instead, capital is flowing toward those performing the “unglamorous” work of clinical integration. This includes embedding AI directly into hospital Electronic Health Records (EHR) and navigating the rigorous regulatory pathways required by the FDA.

This transition reflects a broader movement toward “data liquidity.” With the Department of Health and Human Services (HHS) and the Office of the National Coordinator for Health Information Technology (ONC) enforcing stricter data interoperability, the value has shifted from owning the data to the ability to make that data actionable within a complex clinical workflow.

The Direct-to-Consumer Resurgence and Policy Tailwinds

While institutional funding is consolidating, there is a notable resurgence in the Direct-to-Consumer (D2C) healthcare space. This is driven by a combination of clearer FDA guidance and extended telehealth flexibilities that have persisted since the pandemic.

A new “front door” to healthcare is emerging, where consumer-facing AI platforms—such as OpenAI, Anthropic, and Perplexity—act as orchestrators for biometric data and health records. This creates a streamlined distribution channel for digital health partners who can plug their services into these high-traffic interfaces.

Parallel to this is a shift in how healthcare is paid for. The Centers for Medicare & Medicaid Services (CMS) Innovation Center’s (CMMI) ACCESS Model payment rates have gone live, rewarding operational efficiency and measurable outcomes at scale. As major private payers adopt similar outcome-aligned frameworks, the industry is moving toward a unified payment standard that prioritizes value over volume.

Key Market Takeaways

- Capital Concentration: 12 companies captured nearly 60% of the $4.0 billion in Q1 funding.

- AI Integration: AI is no longer a distinct category but a baseline requirement for all digital health tools.

- Exit Strategy: IPOs remain rare; M&A activity is increasing, often driven by “acquihires” to absorb technical talent.

- Payment Shifts: A move toward outcome-based payment models, influenced by the CMMI ACCESS Model.

The current trajectory suggests that the digital health sector is entering a phase of consolidation. The “mega-deal” trend indicates that investors are betting on a few winners who can integrate AI, manage complex regulatory requirements, and scale within new value-based payment models.

For stakeholders, the next critical checkpoint will be the continued rollout and impact assessment of the CMMI ACCESS Model payment rates, which will determine if outcome-aligned frameworks become the universal standard for digital health reimbursement.

We invite our readers to share their perspectives on the consolidation of health tech funding in the comments below. How is your organization adapting to the shift toward value-based payments?