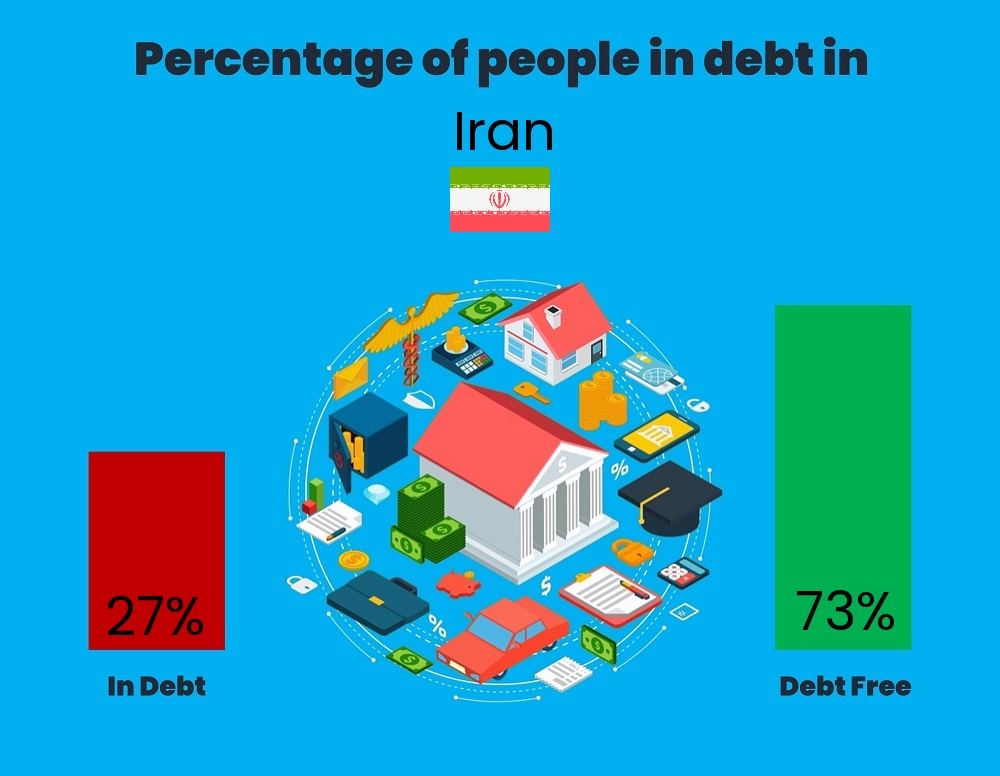

The intersection of geopolitical instability and financial risk in the Middle East has reached a critical juncture, as analysts turn their attention to the internal economic pressures mounting within Iran. The focus has shifted toward the volatility of private debt, a sector increasingly viewed as a barometer for the country’s broader economic resilience in the face of external pressures.

In a recent strategic analysis, Jean-Eudes Clot, a financial strategist at the Banque Cantonale Vodoise (BCV), examined the “clash of opposites” regarding Iranian private debt. The analysis suggests that exogenous shocks are playing a primary role in reshaping the financial landscape, creating a complex environment for investors and policymakers attempting to gauge the stability of the region’s economic foundations.

This focus on internal debt structures comes at a time when the broader market’s understanding of regional conflict is undergoing a significant revision. Financial strategists are now warning that previous assumptions regarding the duration and scope of hostilities in the region may have been overly optimistic, leading to a potential underestimation of long-term market volatility.

The Erosion of Market Assumptions

For several months, global markets operated under the hypothesis that any potential conflict involving Iran would be short-lived, with an estimated duration of four to six weeks. However, this assumption is now eroding. According to Sébastien Gyger of BCV, the unpredictability of the belligerents involved means that multiple, more volatile trajectories must now be considered via BCV markets analysis.

The shift in perspective is significant because the “regional dimension” of the conflict has expanded. As the possibility of a prolonged engagement increases, the pressure on Iran’s internal economy—specifically its ability to manage private debt—becomes a critical vulnerability. When conflict durations extend beyond initial market expectations, the cost of capital typically rises and liquidity tightens, exacerbating the “clash” between private debt obligations and the reality of a constrained economy.

Strategic Analysis of Iranian Financial Risk

The role of the strategist in these volatile periods is to identify the “exogenous shocks” that can trigger systemic failures. Jean-Eudes Clot, who joined the BCV Investment Policy department in 2023, has been instrumental in analyzing how these external pressures manifest within specific financial instruments and debt structures per Allnews profile.

In the context of Iran, the “clash of opposites” often refers to the tension between the state’s attempts to maintain economic stability and the volatile nature of private sector liabilities. As external sanctions and geopolitical tensions fluctuate, the private debt market becomes a primary transmission mechanism for economic shocks, often reacting more violently than state-controlled sectors.

the impact of these regional dynamics extends beyond Iran’s borders, influencing the strategies of central banks. For instance, observers have noted that the Swiss National Bank (BNS) has navigated these effects within its own monetary policy framework, a process Clot has analyzed in the context of the BNS maintaining its policy rate at 0% amidst global uncertainty via Swissinfo.

Key Market Drivers and Impact

The current environment is characterized by several interlocking factors that influence the risk profile of Iranian private debt:

- Conflict Duration: The movement away from the 4-to-6-week conflict hypothesis toward a more open-ended timeline increases the risk of debt defaults.

- Exogenous Shocks: Sudden geopolitical escalations act as catalysts that can destabilize private credit markets.

- Currency Volatility: The interplay between regional instability and currency devaluation often complicates the servicing of debt.

- Monetary Policy Spillovers: The reactions of global central banks to Middle Eastern volatility influence the overall cost of risk.

What This Means for Global Investors

For the global investment community, the situation in Iran serves as a case study in how geopolitical risk is not a monolithic force but one that filters through specific economic channels. The focus on private debt highlights the danger of ignoring internal financial fragilities when assessing the likelihood of a state’s resilience during a conflict.

When a “clash of opposites” occurs—such as high private debt levels meeting a sudden exogenous shock—the resulting instability can lead to rapid capital flight and a breakdown in credit markets. This makes the work of investment policy departments, such as those at BCV, essential for diversifying risk and preparing for “black swan” events in the regional economy.

As the regional dimension of the conflict continues to evolve, the focus will likely remain on whether Iran can stabilize its internal debt obligations or if the erosion of market timelines will lead to a more profound economic crisis.

The next critical checkpoint for market participants will be the upcoming evaluations of regional conflict trajectories and any official updates regarding the Swiss National Bank’s response to these ongoing exogenous shocks.

Do you believe the markets are still underestimating the duration of regional conflicts? Share your thoughts in the comments below or share this analysis with your professional network.