The U.S. Federal Reserve is navigating a complex economic landscape where the desire to ease monetary policy is colliding with stubborn inflationary pressures and geopolitical volatility. While markets have long anticipated a pivot toward lower rates, recent analysis suggests the central bank may be forced to maintain a restrictive stance—or even consider further tightening—to keep inflation from regaining momentum.

The tension centers on the Fed’s “dual mandate” to promote maximum employment and stable prices. Currently, these two goals are pulling in opposite directions: a cooling labor market suggests a need for rate cuts, but accelerating inflation, driven by energy shocks and regional conflicts, argues for a more cautious, “patient” approach. This shift in sentiment is prompting a reassessment of the timeline for any potential Federal Reserve interest rate cuts in 2026.

Recent projections from financial institutions highlight this uncertainty. Wells Fargo economists have adjusted their outlook, noting that the Fed may delay easing in response to rising oil prices and persistent inflation via FXStreet. While some analysts still anticipate a total reduction of 50 basis points for the year, the path to those cuts has become significantly more clouded.

Geopolitical Risks and the Inflationary Spike

A primary driver of the Fed’s current hesitation is the instability in the Middle East. Geopolitical risks associated with conflict in the region have created a “fog” of uncertainty that complicates monetary policy. Analysts at the Wells Fargo Investment Institute stated on April 5, 2026, that they no longer expect interest rate cuts this year due to this ambiguity and the risks surrounding inflation via CNBC Arabia.

The impact of these conflicts is most visible in energy markets. A sudden shock in energy prices acts as a new source of downside risk for the economy while simultaneously pushing inflation higher. This creates a paradox for policymakers: while the economy may need support, the risk of “entrenching” inflation makes the Federal Reserve wary of cutting rates too early.

some officials have warned that U.S. Inflation could potentially exceed 3% as a direct result of war-related disruptions. Such a scenario would likely solidify a “hawkish” stance, where the priority remains price stability over economic stimulation.

The Battle Between the Labor Market and Price Stability

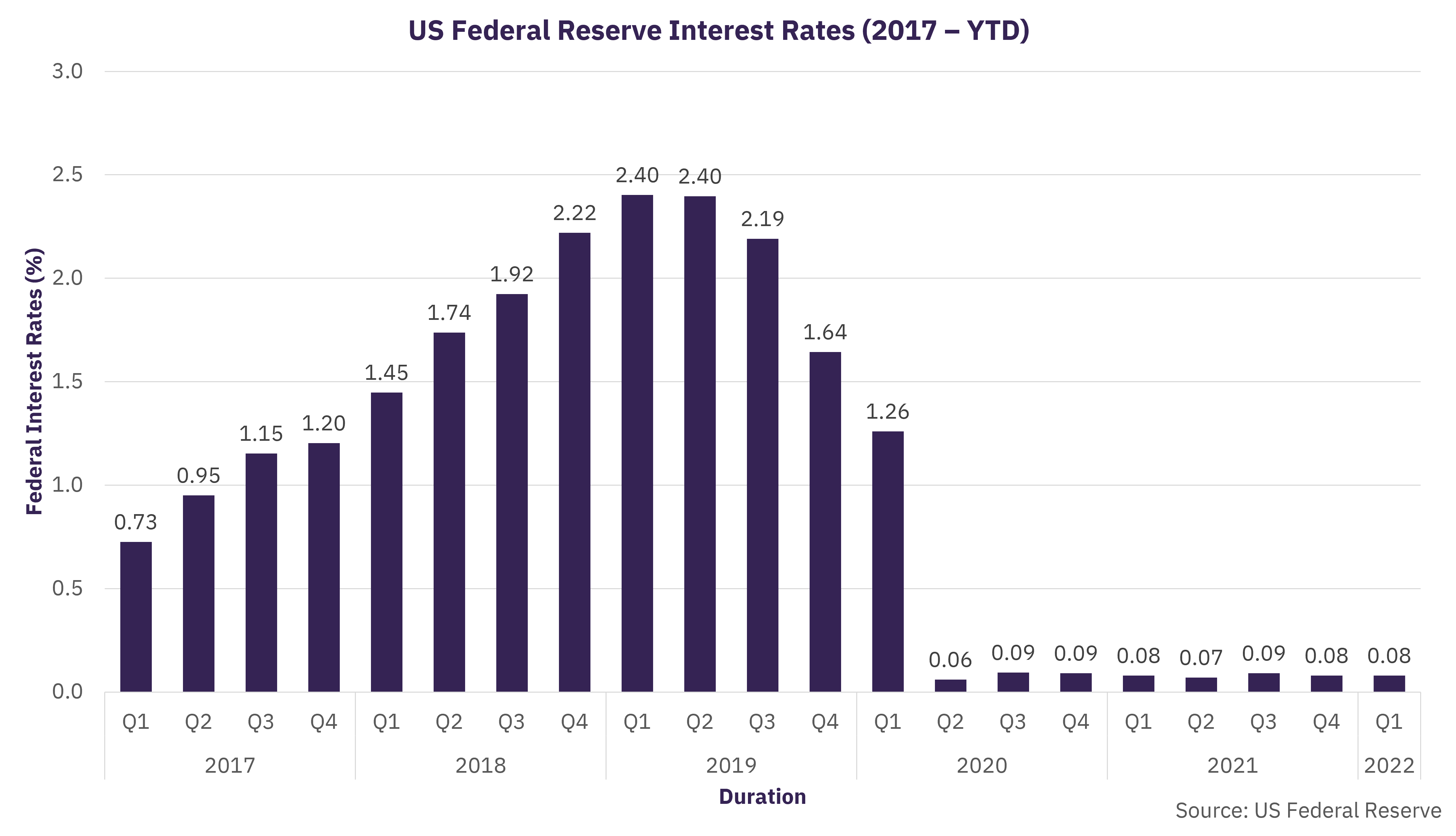

The Federal Reserve is currently balancing a labor market that is described as being on the “moderately negative side” of full employment against a price index that refuses to hit the 2% target. This tug-of-war is reflected in the current federal funds rate, which remains in a restrictive zone.

To understand the “restrictive” nature of current policy, economists compare the immediate federal funds rate—approximately 3.625%—against the long-term average estimate of 3.125% as noted in the September Summary of Economic Projections (SEP) via FXStreet. When the current rate is significantly higher than the long-term average, it is designed to slow down economic activity to curb inflation.

The risk of “patiently” waiting too long is that the labor market could deteriorate further. However, the risk of cutting too early is a resurgence of inflation that could require even more aggressive rate hikes in the future to correct. What we have is why the Fed is exhibiting what analysts call “abundant patience.”

Key Factors Influencing the Fed’s Decision

- Energy Price Shocks: Rising oil prices contribute directly to consumer price indices and transportation costs.

- Geopolitical Volatility: Conflict in the Middle East disrupts supply chains and creates market instability.

- Labor Market Cooling: A gradual slowdown in hiring provides some room for the Fed to keep rates high without causing a severe recession.

- Inflation Persistence: The difficulty of bringing inflation down to the 2% target suggests that the “last mile” of disinflation is the hardest.

Market Expectations vs. Central Bank Reality

There is often a gap between what the financial markets desire and what the Federal Reserve is willing to do. Market “swaps” and trading patterns indicate a desire for easing, but the Fed’s internal deliberations—often revealed in meeting minutes—suggest a more rigid adherence to inflation targets.

For instance, while Wells Fargo previously expected two rate cuts this year, they shifted their view on April 5, 2026, citing a “marked increase in inflation,” even if that increase is likely temporary via CNBC Arabia. This adjustment mirrors a broader trend among institutional investors who are realizing that the “pivot” to lower rates may be delayed or smaller than previously hoped.

Other institutions, such as Citigroup, have also pushed back their timelines for rate cuts, citing unexpected increases in U.S. Job openings and the lingering threat of inflation via CNBC Arabia. This suggests a consensus among major banks that the Federal Reserve is unlikely to rush into easing.

What This Means for Global Markets

Since the U.S. Dollar serves as the world’s primary reserve currency, the Fed’s decision to keep rates high has global repercussions. Higher U.S. Rates generally strengthen the dollar, which can put pressure on other currencies and increase the cost of dollar-denominated debt for emerging markets.

For investors, the “higher for longer” narrative means that the cost of borrowing will remain elevated. This affects everything from corporate capital expenditures to mortgage rates for consumers. The shift from expecting rapid cuts to accepting a “restrictive” environment requires a fundamental adjustment in portfolio management and corporate financial planning.

The Path Forward: What to Watch

As the Federal Reserve continues to monitor the data, the focus will remain on the “core” inflation numbers—which strip out volatile food and energy prices—to see if the underlying trend is truly descending. If core inflation remains sticky, the possibility of “holding” rates at current levels for the remainder of the year becomes the baseline scenario.

The Fed’s communication strategy will be critical. By signaling “patience,” they are attempting to manage market expectations and prevent a premature rally in stocks and bonds that could actually fuel further inflation. The goal is a “soft landing”—bringing inflation down without triggering a severe economic contraction.

For those tracking these developments, the most critical indicators will be the monthly Consumer Price Index (CPI) reports and the Federal Open Market Committee (FOMC) meeting minutes. These documents provide the most direct insight into whether the Fed is leaning toward a “hawkish” (aggressive) or “dovish” (easing) posture.

The next major milestone will be the upcoming FOMC meetings in September and December. While some analysts still hold out hope for 25-basis-point cuts during these sessions via FXStreet, those moves are now contingent on a confirmed downward trend in inflation and a stabilization of energy prices.

We encourage our readers to share this analysis and join the discussion in the comments below. How is the “higher for longer” interest rate environment affecting your business or investment strategy?