For many members of Generation Z, the current financial landscape feels less like a stepping stone and more like a barrier. Caught between record-high rents and a volatile labor market, this demographic is navigating a period of acute financial pressure. Yet, beneath the immediate struggle to balance monthly budgets, a massive economic shift is brewing that could redefine the global marketplace.

Recent data suggests a stark paradox: while Gen Z is currently spending twice as much as they are saving, they are positioned to become one of the most influential economic forces in history. This transition from current precarity to future prosperity is driven by a combination of rising incomes and a historic transfer of assets from older generations.

As a sports editor, I have watched the shift in how the younger generation consumes entertainment—moving from traditional stadium seats to eSports and digital interfaces. This same pivot toward a digital-first existence is now mirroring their financial behavior, as they reshape how money is spent, saved and invested on a global scale.

The Immediate Struggle: Rent, Wages, and Labor Volatility

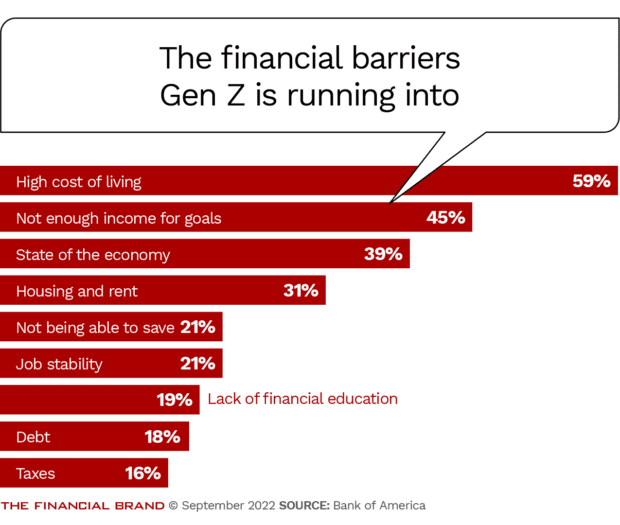

The current economic reality for Gen Z—those born between 1996 and 2016 according to Bank of America Private Bank—is characterized by a high cost of living that often outweighs wage growth. According to the Bank of America Institute, Gen Z is currently spending twice as much as they are saving, largely due to the financial pressure exerted by the cost of living per BofA data.

This financial strain is compounded by an increasingly tricky labor market. While some sectors have seen wage growth, new entrants to the workforce are facing significant headwinds. In February 2025, the number of Gen Z households receiving unemployment benefits grew by nearly 32% year-over-year according to Bank of America Institute analysis. This rise in unemployment among new labor market entrants highlights a precarious start for a generation that is simultaneously driving faster spending growth on both necessary and discretionary items compared to the general population.

Despite these hurdles, Gen Z maintains some resilience. Bank deposit balances have provided a necessary buffer, allowing them to maintain consumption patterns even as the gap between their earnings and expenses widens.

A Digital-First Approach to Consumption

Gen Z is the first generation born into a fully online world, and this “digital native” status is fundamentally altering industry standards. Their preferences extend beyond just technology; they influence the incredibly nature of social and commercial interaction. For instance, this demographic often favors remote interactions over personal ones, even when engaging with friends as noted by BofA Global Research.

This shift is evident in several key areas:

- Commerce: A strong preference for purchasing goods and services exclusively through apps.

- Dining: A trend toward visiting restaurants not just for the meal, but to capture and share photos of the food.

- Entertainment: A marked preference for eSports over traditional sports, signaling a pivot in how the sports industry must engage with future audiences per Bank of America Private Bank.

The Path to Becoming the Richest Generation

While the present is marked by struggle, the long-term projections for Gen Z are staggering. Financial analysts suggest that within a decade, the global wealth of Gen Z is expected to jump from $7 trillion to $30 trillion according to Haim Israel, head of Global Thematic Investing at BofA Global Research.

This wealth surge is not solely dependent on their own earnings. A critical component is the “Great Wealth Transfer,” where Baby Boomers are expected to pass down significant assets to younger generations per Bank of America Institute. This transfer of assets, combined with their own professional growth, will place unprecedented purchasing power in the hands of Gen Z.

The projections for their collective income are equally ambitious. BofA Global Research indicates that in roughly the next five years, Gen Z will have globally amassed $36 trillion in income. By approximately 2040, that figure is expected to surge to $74 trillion according to BofA Global Research.

Key Takeaways: Gen Z’s Economic Trajectory

- Current State: High cost of living and a 32% year-over-year increase in unemployment benefits for Gen Z households as of February 2025.

- Spending Habits: Spending growth is outpacing the general population, with spending currently double the amount being saved.

- Wealth Projections: Global wealth is projected to rise from $7 trillion to $30 trillion within roughly ten years.

- Income Growth: Global income is expected to reach $36 trillion within five years and $74 trillion by 2040.

- Market Drivers: The “Great Wealth Transfer” from Baby Boomers and a preference for app-based, digital-first consumption.

What In other words for the Global Economy

The transition of Gen Z into a dominant economic force will likely force industries to adapt to their specific social values and financial preferences. When a generation with a projected $74 trillion in income by 2040 begins to dictate market trends, the impact will be felt across every sector, from real estate to retail and professional sports.

Investors are already taking note of these shifts. As Haim Israel and Chris Hyzy, Chief Investment Officer of Merrill and Bank of America Private Bank, have discussed, the intersection of Gen Z’s wealth and their unique preferences is set to transform markets per BofA Private Bank.

For the sports world specifically, the preference for eSports and digital engagement means that traditional models of fandom and sponsorship must evolve. The “stadium experience” is no longer the sole gold standard; the digital experience is now a primary requirement for capturing the attention of the next generation of consumers.

The overarching narrative for Generation Z is one of resilience and eventual dominance. While they are currently “squeezed” by the immediate pressures of the economy, their trajectory suggests they will eventually possess the greatest financial leverage of any generation before them.

The next critical checkpoint for monitoring these trends will be the ongoing analysis of labor market data and the pace of the wealth transfer from Baby Boomers, which will determine how quickly these projections materialize.

Do you think the “Great Wealth Transfer” will happen fast enough to offset current cost-of-living pressures? Share your thoughts in the comments below.