The Slovak residential real estate market is undergoing a structural shift as investment-driven demand increasingly sidelines first-time homebuyers. Recent data indicates that less than half of all property acquisitions are currently made by individuals purchasing their first home, with new residential developments being disproportionately claimed by investors looking to secure assets in an inflationary environment. This trend, coupled with rising mortgage interest rates that reached 3.7% in May, has significantly raised the financial barrier to entry for younger generations, according to reports from the National Bank of Slovakia and industry analysts.

The Shift Toward Investment-Led Demand

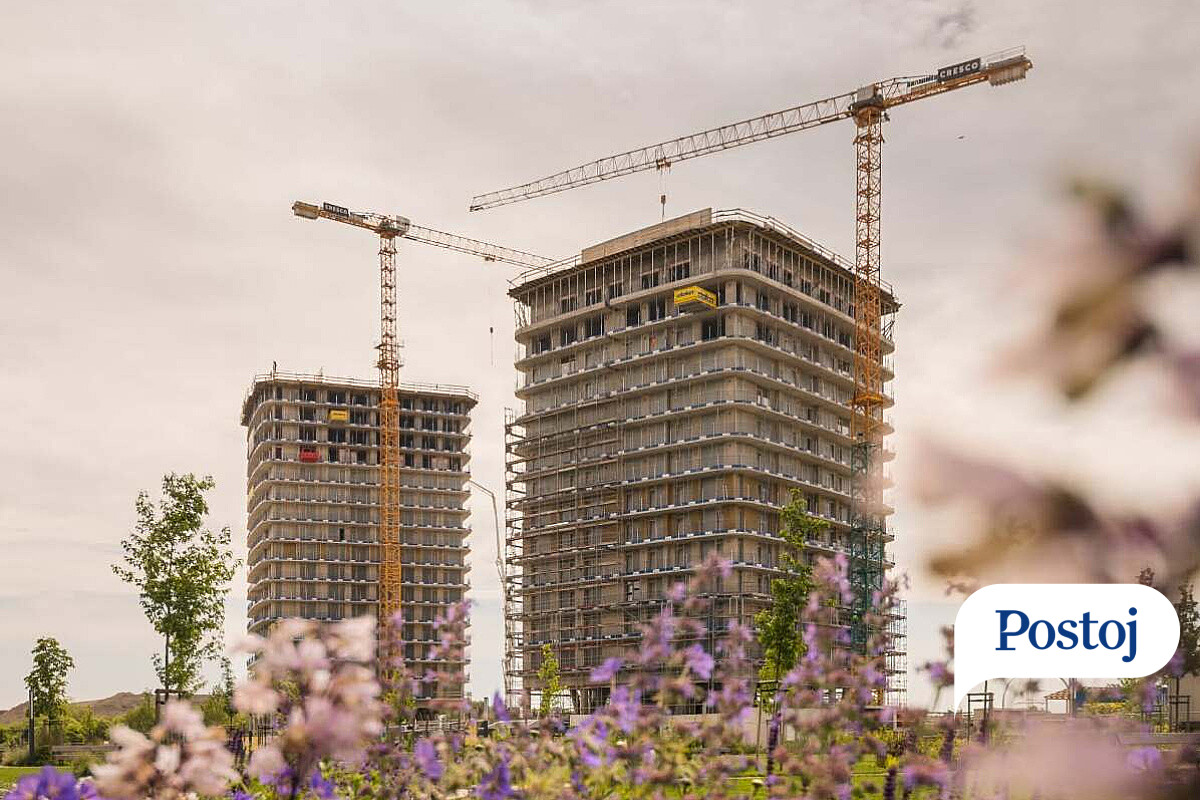

The composition of the buyer pool in the Slovak housing market has changed markedly over the past several years. Where residential units were once primarily the domain of families seeking primary residences, a substantial portion of new supply is now absorbed by buyers who already own real estate. This phenomenon is particularly visible in major urban centers such as Bratislava, where developers report that a significant percentage of units in new projects are sold to investors rather than end-users.

This trend has created a competitive environment where young, first-time buyers must compete against capital-rich investors. The resulting price pressure has contributed to Slovakia experiencing some of the most rapid housing price growth within the European Union over the last decade, as noted in data analyzed by Eurostat. For many young professionals, the combination of high down-payment requirements and the steady appreciation of property values has made the prospect of homeownership increasingly elusive.

Mortgage Costs and Economic Pressure

The affordability crisis is compounded by the volatility of borrowing costs. After a period of historically low interest rates, the cost of financing has seen a marked upward trajectory. In May, average mortgage rates climbed to 3.7%, a figure that reflects the broader tightening of monetary policy intended to combat inflation. This rate increase directly impacts the monthly debt-service-to-income ratio for prospective homeowners, effectively disqualifying many from securing the necessary financing to purchase property at current market prices.

Financial analysts point to the “debt-to-income” constraints mandated by the National Bank of Slovakia as a key factor in the current market dynamics. These regulations, designed to prevent a systemic housing bubble, limit the amount of leverage a household can take on relative to their annual income. While these measures protect the banking sector from high-risk lending, they also place a stricter ceiling on the purchasing power of average households, leaving them unable to match the cash-heavy offers typical of institutional or private investors.

Market Outlook and Sustainability

The sustainability of these price levels remains a subject of intense debate among economists. Some market observers express concern that the reliance on investment-driven demand could signal an overvaluation of the market, particularly if rental yields fail to keep pace with the capital costs of property acquisition. Conversely, others argue that the structural undersupply of housing in Slovakia provides a fundamental floor for prices, regardless of investor activity.

For prospective buyers, the current environment necessitates a cautious approach. Financial advisors frequently emphasize the importance of stress-testing household budgets against further potential rate hikes. The disparity between income growth and property price appreciation remains the most significant challenge for the domestic market. As the European Central Bank continues to monitor regional inflation, the trajectory of Slovak mortgage rates will likely remain tied to broader eurozone policy decisions.

Moving Forward

The next major checkpoint for the real estate sector will be the release of the upcoming Financial Stability Report from the National Bank of Slovakia, which is expected to provide further clarity on household indebtedness and the health of the mortgage market. These official updates serve as the primary indicator for how regulators view the current risks associated with the residential sector.

Readers are encouraged to monitor official communications from the National Bank of Slovakia for the latest updates on macroprudential measures. If you have experience navigating the current housing market, please share your perspective in the comments section below.