In the evolving landscape of American regional banking, Truist Financial Corporation finds itself navigating a complex confluence of macroeconomic pressures. As the financial sector recalibrates in response to shifting interest rate policies, investors and analysts are closely scrutinizing the firm’s balance sheet management and its ability to sustain profitability. Conducting a Truist Financial SWOT analysis reveals a company currently contending with structural headwinds, particularly concerning net interest margins and the ongoing challenge of managing deposit costs in a high-rate environment.

For shareholders and market observers, understanding the mechanics of these pressures is essential. While the bank seeks to optimize its asset-liability positioning, the reality remains that deposit expenses have not declined in lockstep with broader market shifts. This disconnect creates a tightening effect on net interest income, forcing a strategic pivot in how the institution manages its interest-bearing liabilities and asset yields. As we examine the core pillars of the bank’s current position, it becomes clear that liquidity management and operational efficiency are no longer just internal metrics. they are the primary drivers of investor sentiment.

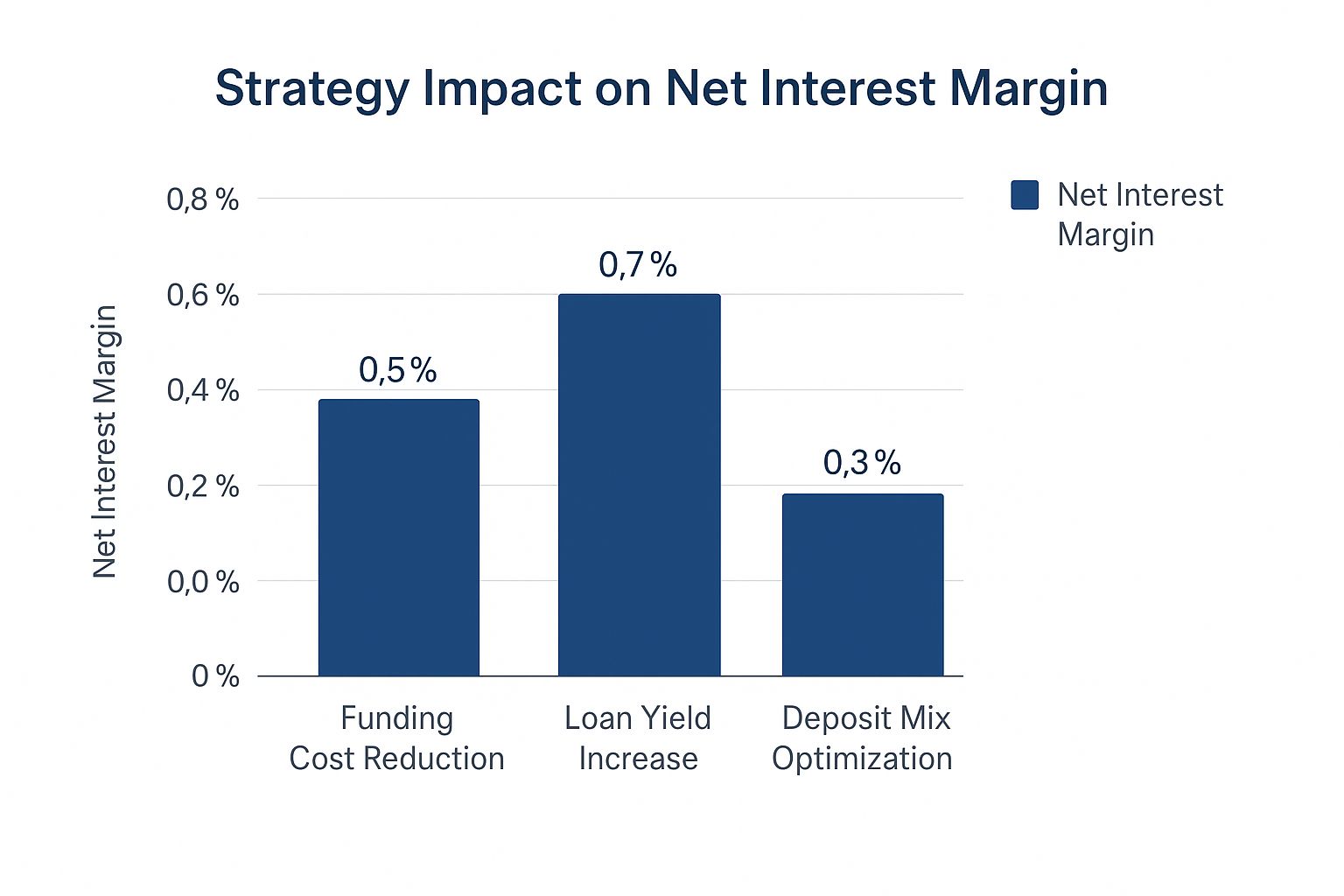

Evaluating the Net Interest Margin Struggle

The primary concern for Truist Financial, and indeed many of its peers in the regional banking space, centers on the sustainability of net interest margins (NIM). The Federal Deposit Insurance Corporation (FDIC) has historically emphasized the critical role of deposit beta—the speed at which a bank adjusts its deposit rates in response to changes in market interest rates—in determining long-term profitability. When deposit costs remain “sticky” while asset yields begin to stabilize or fluctuate, the margin between the two compresses, directly impacting the bottom line.

Truist’s management has signaled a focus on rigorous asset-liability management (ALM) strategies, aiming to recalibrate their funding mix. However, the ability to lower deposit costs is heavily contingent on competitive pressures within their specific geographic footprint and the broader demand for liquidity. According to recent investor relations filings from Truist Financial, the bank is actively seeking to improve its efficiency ratio while maintaining a stable capital base. This balancing act is central to the “Weaknesses” and “Threats” quadrants of any objective SWOT assessment, as it highlights the bank’s vulnerability to external monetary policy decisions that remain outside of its direct control.

Strategic Pillars: Opportunities and Strengths

Despite the prevailing headwinds, Truist maintains a significant market presence, particularly following the merger of equals between BB&T and SunTrust, which formed the current iteration of the company. This scale provides a degree of geographic diversification that smaller regional players lack. The firm’s “Strengths” are rooted in its robust fee-based income streams, which provide a buffer against the volatility of net interest income. By leveraging its diversified business model—encompassing insurance, wealth management, and investment banking—Truist can, in theory, offset some of the margin compression experienced in its core commercial and retail lending segments.

The “Opportunities” for the bank lie in its potential for digital transformation and cost-rationalization programs. As the Federal Reserve continues to monitor systemic liquidity, banks that demonstrate superior technological integration and customer retention strategies are likely to see improved long-term valuation. For Truist, the path forward involves continuing to streamline its branch footprint while simultaneously enhancing its digital banking interface to attract lower-cost deposits, thereby reducing its reliance on more expensive wholesale funding sources.

The Road Ahead: Risk Management and Outlook

Market analysts often point to the “Threats” posed by regulatory scrutiny and potential shifts in credit quality. As economic conditions fluctuate, the pressure on loan portfolios—particularly in commercial real estate—remains a focal point for institutional investors. Truist’s ability to navigate these risks will depend on its conservative underwriting standards and its capacity to maintain robust capital ratios, as mandated by Federal Reserve supervisory guidelines.

Investors should look toward the next quarterly earnings presentation for concrete data regarding the bank’s progress in reducing its cost of funds. Management’s commentary on their “asset-liability management” strategy will provide the clearest indicator of whether they have successfully mitigated the margin compression issues that have plagued recent performance. Monitoring these updates is essential for any stakeholder looking to understand the bank’s trajectory in the coming fiscal year.

As we continue to monitor the financial sector’s recovery and stabilization, we encourage our readers to engage with the latest official SEC filings provided by Truist Financial to ensure they are making decisions based on verified, primary data. We welcome your perspectives on the regional banking sector; please share your thoughts or questions in the comments section below as we continue to track these developments in real-time.