For many aspiring homeowners and investors, the prospect of purchasing a foreclosed home in Spain presents a compelling opportunity to enter the Mediterranean real estate market at a significant discount. These properties, often held by financial institutions after previous owners fail to meet mortgage repayments, can offer a path to homeownership that is more affordable than traditional market listings.

However, the allure of a bargain price often masks a complex landscape of legal and structural risks. While the potential for a “bargain” is real, the process of buying a foreclosed home in Spain requires a rigorous approach to due diligence to avoid inheriting the previous owner’s debts or facing unexpected legal battles.

From navigating the Official State Gazette’s auctions to negotiating with major lenders like Santander or BBVA, the journey from search to signing involves specific steps that differ from a standard residential purchase. Understanding these nuances is critical for anyone looking to secure a stable investment in the Spanish market.

Where to Find Foreclosed Properties in Spain

Finding bank-owned properties requires looking beyond standard real estate listings. You’ll see several reliable channels for identifying these assets, ranging from official government portals to specialized bank divisions.

The most direct route is through the real estate platforms operated by the banks themselves. Major Spanish institutions, such as BBVA and Santander, maintain dedicated divisions that list their foreclosed homes, often providing detailed information on available financing options and property specifications through official bank channels.

For those seeking a broader overview, specialized real estate portals like idealista categorize bank-owned flats by area or entity, allowing buyers to compare options across different lenders. The Official State Gazette’s BOE auctions serve as a highly reliable source for finding foreclosed homes, as these official listings provide a transparent record of properties being sold via public auction via the BOE auctions.

The Advantages and Financial Incentives

The primary draw of a repossessed property is the price. Because banks are often motivated to liquidate these assets quickly to recover debts, they may be open to offers well below the current market value. In some cases, particularly with “distressed properties”—developments that were repossessed after developers went bankrupt following the 2007 market collapse—discounts can range from 30% to 50% below market value on distressed property discounts.

Financing can similarly be more flexible when dealing directly with the holding bank. Lenders may be more willing to offer higher mortgage values or more favorable terms to incentivize a quick sale. In certain instances, banks may even provide financing covering up to 100% of the property’s price on bank financing options.

there is often a level of clarity regarding the legal title. Since the bank typically clears its own loans off the property during the repossession process, the title is generally free of the specific mortgage that triggered the foreclosure, which can simplify the eventual transfer of ownership.

Critical Risks and Necessary Due Diligence

Despite the financial advantages, buying a foreclosed home in Spain is considered a riskier venture than a standard purchase. Buyers must be vigilant about “hidden traps” that may not be immediately apparent in a listing.

Legal and financial liabilities are a primary concern. Even when buying from a bank, a property may approach with unpaid taxes, outstanding community fees, or debts owed by the previous owner. There is also the risk of encountering squatters in the property, which can complicate the handover process.

To mitigate these risks, it is essential to employ a qualified Spanish conveyancing lawyer to perform full due diligence. A legal professional can verify that the property is free of liens and that all administrative requirements are met before the contract is signed.

Beyond the legalities, the physical condition of the property can be a gamble. Many foreclosed homes have been vacant for extended periods or were neglected by the previous owners. It is strongly advised to hire an architect, building surveyor, or professional builder to inspect the property for major structural problems before committing to a purchase.

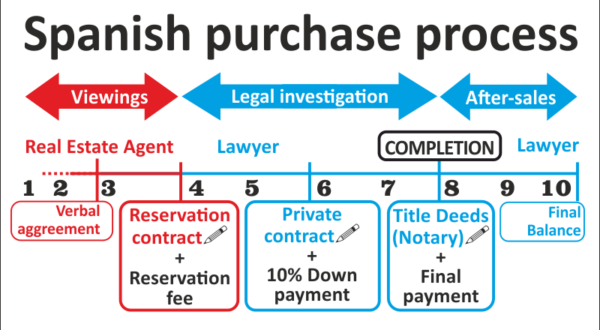

The Purchase Process: From Search to Deed

The process of acquiring a repossessed property follows a trajectory similar to a standard home purchase, but with an initial emphasis on the buyer’s financial standing.

- Credit Assessment: The lender first assesses the buyer’s creditworthiness to determine if they qualify for the bank’s internal financing.

- Reservation: Once approved, a reservation is made to secure the property and take it off the market.

- Contract Signing: The buyer and the bank sign a purchase contract detailing the agreed price and conditions.

- The Deed: The process concludes with the signing of the public deed, which officially transfers ownership.

Viewing the properties has become more accessible. buyers no longer necessitate to visit bank offices to schedule tours, as most repossessed homes are listed online with photo galleries and virtual tours.

Key Takeaways for Buyers

- Search Sources: Use bank-owned portals, specialized sites like idealista, and the BOE official auctions.

- Pricing: Appear for opportunities in “distressed” developments where discounts can reach 30-50%.

- Legal Protection: Never proceed without a qualified Spanish conveyancing lawyer to check for unpaid taxes and community debts.

- Physical Inspection: Always engage a surveyor or architect to identify structural issues.

- Financing: Check if the holding bank offers preferential mortgage terms or high-value loans.

Potential buyers should remain cautious and prioritize thorough verification over the speed of the transaction. While the financial rewards can be significant, the legal complexities of the Spanish real estate market demand professional guidance.

For those tracking these opportunities, the next step is typically the monitoring of new listings on bank portals and the BOE auction calendar for upcoming foreclosures.

Do you have experience buying property in Spain? Share your thoughts or questions in the comments below.

Keep reading