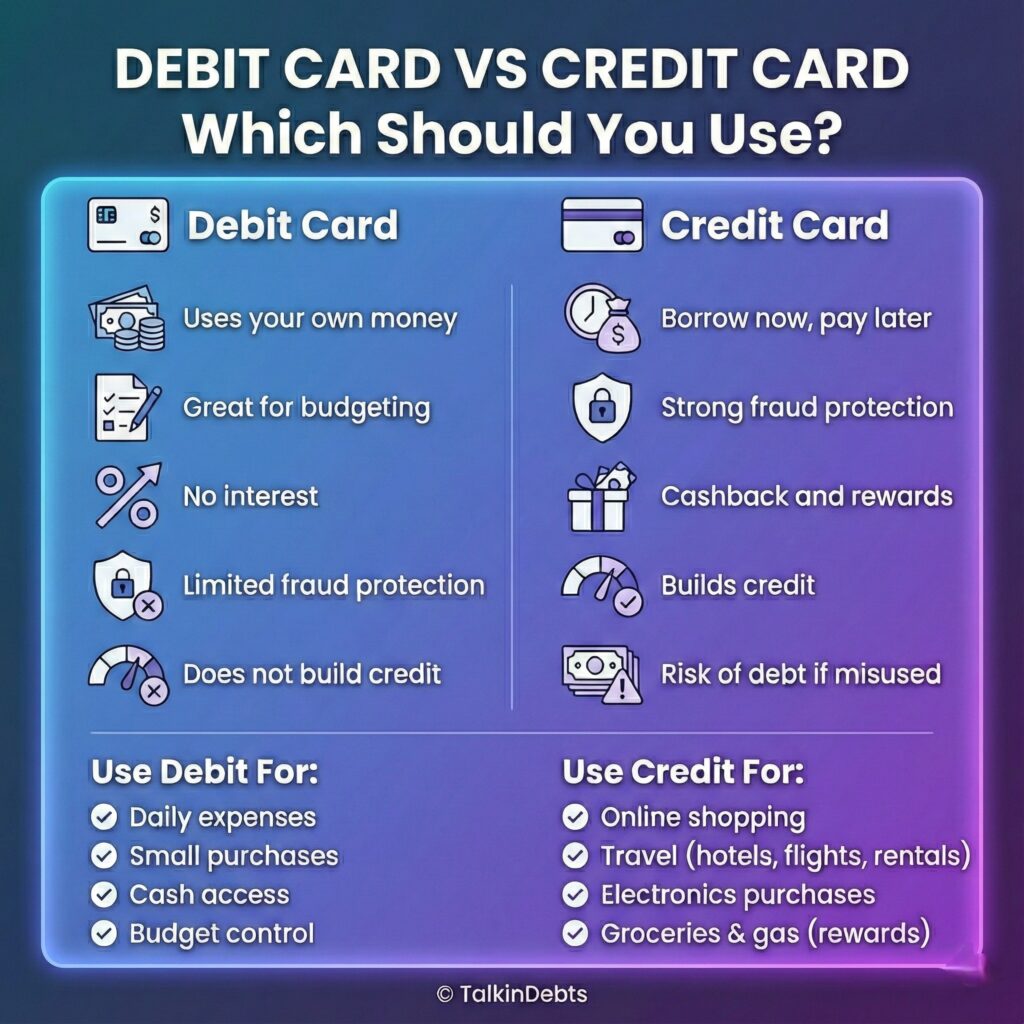

Navigating the complexities of modern banking can often perceive like deciphering a foreign language, especially when the terms we use in daily conversation don’t align with the technical reality of our plastic cards. Many consumers use the term “credit card” as a catch-all for any piece of plastic used for payments, but in the European regulatory landscape, the distinction between a credit card and debit card is not just semantic—We see a matter of legal classification and financial impact.

For the average consumer, understanding these differences is the first step in avoiding unnecessary fees and managing liquidity more effectively. Whether you are tracking daily spending or leveraging a monthly grace period, the type of card in your wallet determines how your money moves from your account to the merchant and, crucially, whether you are spending your own funds or borrowing from a financial institution.

Under European regulations, all banking cards must now clearly display their category—”débit,” “crédit,” or “carte de crédit”—on the front of the card to ensure transparency. This mandate helps users identify at a glance how their transactions are processed and whether they are subject to interest charges or immediate balance deductions.

Understanding the Debit Card: Immediate Access and Control

A debit card is fundamentally a tool for accessing funds you already possess. It is linked directly to your current account, meaning that when you develop a purchase, the money is drawn from your existing balance. According to La Banque Postale, You’ll see three primary variations of debit cards, each offering a different level of control over spending.

The first category is the immediate debit card with systematic authorization. These cards are designed for maximum budget discipline; for every single transaction, the bank checks the account balance in real-time. If the funds are insufficient, the transaction is declined. This mechanism effectively prevents the account holder from entering an unauthorized overdraft.

The second type is the immediate debit card without systematic authorization. These offer more flexibility, as the bank does not verify the balance for every single purchase. Instead, transactions are typically deducted from the account immediately or within a maximum window of 48 hours, as noted by Comparabanques. While convenient, this lack of real-time verification means users must be more vigilant to avoid accidental overdrafts.

Finally, there are deferred debit cards. While these are categorized under “credit” labels on the card face in some jurisdictions, they function differently from traditional credit lines. With a deferred debit card, all expenditures over a set period—usually a month—are accumulated and then deducted as a single lump sum from the current account at the end of the cycle. As specified by Crédit Mutuel, these transactions are generally processed without interest charges, providing a way to manage monthly cash flow without incurring debt.

The Mechanics of Credit Cards and Revolving Credit

True credit cards operate on a fundamentally different principle than debit cards. Rather than drawing from a current account, a credit card allows the user to tap into a “renewable reserve” of money lent by the bank. This means the user is spending the bank’s money up to a certain limit, rather than their own.

The primary characteristic of a true credit card is the application of interest. While deferred debit cards simply move the date of the deduction, a credit card involves a loan. According to Comparabanques, these cards provide greater flexibility and payment freedom but reach with the cost of interest payments on the borrowed funds.

To avoid confusion, European regulations require these specific instruments to carry the explicit mention “carte de crédit” on the recto of the card. This distinguishes them from “deferred debit” cards, which may simply say “crédit” but do not involve a revolving credit line with interest.

Comparison of Card Types and Their Impact

| Card Type | Label on Card | Funding Source | Timing of Deduction | Interest Charges |

|---|---|---|---|---|

| Immediate Debit | Débit | Current Account | Immediate to 48 hours | No |

| Deferred Debit | Crédit | Current Account | Once per month | No |

| Credit Card | Carte de Crédit | Bank Credit Line | Variable/Monthly | Yes |

Choosing the Right Tool for Your Financial Strategy

The choice between a credit card and debit card often depends on the user’s priority: visibility or flexibility. Those who prioritize a clear, real-time view of their spending often prefer immediate debit cards. This is particularly true for those using systematic authorization cards, which provide a hard stop against overspending.

Conversely, those who require more “breathing room” in their monthly budget may find deferred debit cards appealing. These allow for a single monthly payment, simplifying accounting and providing a temporary window of liquidity without the risk of interest charges. For those who need access to funds beyond their current balance for larger purchases or emergencies, a true credit card is the only option, provided the user is comfortable with the associated interest rates.

In France, the preference for debit instruments is significant, with approximately 70% of issued banking cards being debit cards, according to data from Comparabanques. This trend reflects a broader consumer preference for spending within their means and avoiding the complexities of revolving debt.

Key Takeaways for Consumers

- Check the Label: Look at the front of your card. “Débit” means immediate deduction; “Crédit” usually indicates deferred debit; “Carte de Crédit” indicates a loan with interest.

- Authorization Matters: If you struggle with budgeting, a “systematic authorization” debit card is the safest tool to prevent overdrafts.

- Avoid Interest: If you aim for the convenience of monthly billing without paying interest, opt for a deferred debit card rather than a revolving credit card.

- Monitor Timelines: Be aware that “immediate” debit can still grab up to 48 hours to reflect in your balance depending on the card’s specific terms.

As banking regulations continue to evolve toward greater transparency, the responsibility lies with the consumer to verify the specific terms of their agreement with their financial institution. Understanding whether your card is a tool for spending your own money or a tool for borrowing someone else’s is the most critical distinction in personal finance.

For those looking to change their card type, most banks allow a transition from debit to credit (or vice versa) through their mobile application or a request to their account manager, subject to a credit review for credit-based products.

We invite our readers to share their experiences with different banking instruments in the comments below. Which card type best fits your monthly budgeting strategy?