As French high school graduates—the nouveaux bacheliers—transition into higher education, banking institutions are increasingly tailoring financial products to meet the needs of young adults. These specialized offerings, often referred to as “coups de pouce” or financial boosts, typically include essential services such as current accounts, mobile payment cards, and digital money management tools, aimed at simplifying the transition to financial independence.

According to the French Ministry of Economy and Finance, young adults aged 18 to 25 have access to specific banking arrangements that account for their limited income and the specific costs associated with student life. While traditional retail banks and online neobanks both compete for this demographic, the primary objective remains the same: providing a digital-first experience that allows students to monitor their spending in real time, often through intuitive smartphone applications.

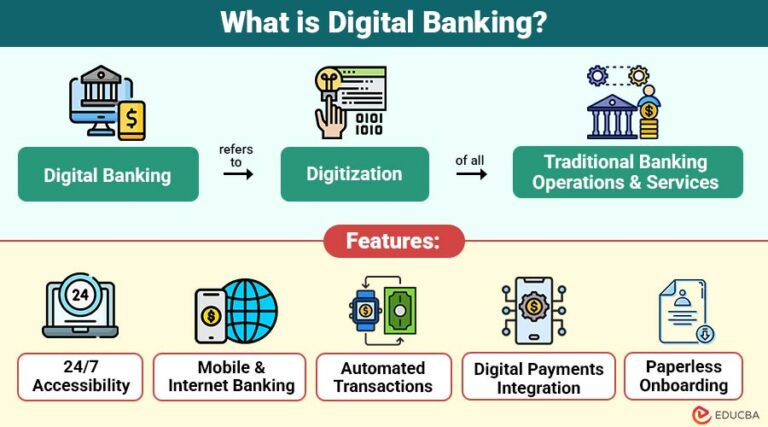

Understanding the Shift Toward Digital Banking for Students

The landscape for student banking has shifted significantly over the past decade, moving away from physical branch reliance toward mobile-centric platforms. Most major financial institutions now offer “student packages” that waive or significantly reduce monthly account maintenance fees. Data from the French Banking Federation (FBF) indicates that these packages are designed to act as an entry point for long-term customer loyalty, providing students with basic credit facilities, international payment capabilities, and overdraft protections tailored to academic calendars.

For many students, the primary appeal of these accounts is the speed of implementation. Unlike traditional banking processes that might require multiple in-person meetings, many modern accounts can be opened entirely online via a smartphone. This process requires a valid identity document and, in some cases, proof of enrollment at a higher education institution to unlock specific student-only benefits.

Key Features of Modern Student Accounts

When selecting a banking provider, new graduates should prioritize specific features that offer both convenience and security. Most competitive student offers currently include the following components:

- No-fee accounts: Many banks eliminate monthly service charges for account holders under the age of 25 or 28, provided they are enrolled in university.

- Real-time notifications: Push alerts for every transaction help students stay within their monthly budgets, a feature emphasized by major digital-native banks.

- International functionality: With many students participating in Erasmus+ or other exchange programs, the ability to make payments abroad without excessive currency conversion fees is a critical consideration.

- Security controls: The ability to instantly freeze a card via an app if it is lost or stolen has become a standard security expectation for this demographic.

The Service-Public.fr portal, the official website for French administrative information, notes that students should carefully review the terms of any overdraft authorization, as interest rates on these short-term loans can vary substantially between institutions.

Comparing Traditional Retail Banks and Neobanks

The choice between a traditional bank and an online-only neobank often depends on the student’s need for physical versus digital services. Traditional banks offer the advantage of a local branch network, which can be beneficial if a student requires assistance with more complex financial products, such as student loans or housing insurance. Conversely, neobanks often provide a more streamlined user interface and lower fees for international transactions.

According to reports from the Banque de France, the central bank of the French Republic, consumers should always ensure their chosen institution is licensed and authorized to operate within the European Union. This regulatory oversight is essential for protecting deposits and ensuring that the institution adheres to strict anti-money laundering and data protection protocols.

Next Steps for New Graduates

For those preparing to open their first independent account, the recommended course of action is to compare at least three different offers based on the specific services required. Many institutions provide online comparison tools, and consumer advocacy groups frequently publish annual reviews of banking fees in France.

The next major regulatory update concerning consumer banking fees in France is expected to be discussed during the annual review by the Comité Consultatif du Secteur Financier (CCSF), which monitors transparency in banking service pricing. Students and their families are encouraged to monitor the CCSF website for updates on fee caps and standardized service definitions. For more information on navigating these financial choices, readers are invited to share their experiences in the comments section below.