Navigating the complexities of Italian tax legislation can be a daunting endeavor for many families, particularly those managing the daily challenges of disability. Central to the Italian welfare framework is Legge 104, a landmark piece of legislation designed to provide support, social integration and rights to individuals with disabilities. For many, understanding exactly which financial obligations are waived or reduced under this framework—often summarized as “Legge 104, cosa non pagare”—is not merely a matter of administrative curiosity, but a vital component of household financial planning.

As a financial journalist, I have spent nearly two decades analyzing how economic policies intersect with the lives of citizens. In Italy, the provisions associated with Law 104/1992 offer significant fiscal relief, yet the criteria for these exemptions are precise and strictly regulated by the Agenzia delle Entrate (the Italian Revenue Agency). Misunderstandings regarding which taxes are exempt, such as the bollo auto (car tax) or potential municipal levies, often lead to missed opportunities for legitimate savings or, conversely, administrative penalties for those who claim benefits for which they do not qualify.

It is essential to clarify that “Legge 104” is not a blanket tax exemption. Rather, it is a comprehensive legal framework that grants specific tax benefits—such as deductions, reduced VAT rates, and exemptions—contingent upon the severity of the disability and the specific type of expenditure. Below, we break down the current landscape of these exemptions based on official government guidelines.

Understanding Tax Exemptions: The Bollo Auto and Vehicle Benefits

One of the most widely discussed benefits under the umbrella of disability legislation is the exemption from the bollo auto, or vehicle registration tax. According to the official guidance provided by the Agenzia delle Entrate, this exemption is not automatic for every individual holding a Law 104 certificate. It is strictly reserved for individuals with specific physical or sensory disabilities, including those with limited motor capacity, blindness, deafness, or those with significant intellectual disabilities who require constant assistance.

The exemption applies to vehicles with engine displacements up to 2,000 cc for gasoline engines or 2,800 cc for diesel engines. Crucially, the vehicle must be used, either exclusively or prevalently, for the benefit of the disabled person. If the disabled individual is not the driver, the vehicle must be registered in their name or the name of the family member who provides primary care, and support. This is a critical distinction, as the law is designed to facilitate the mobility of the person with the disability rather than providing a generalized tax break for the household.

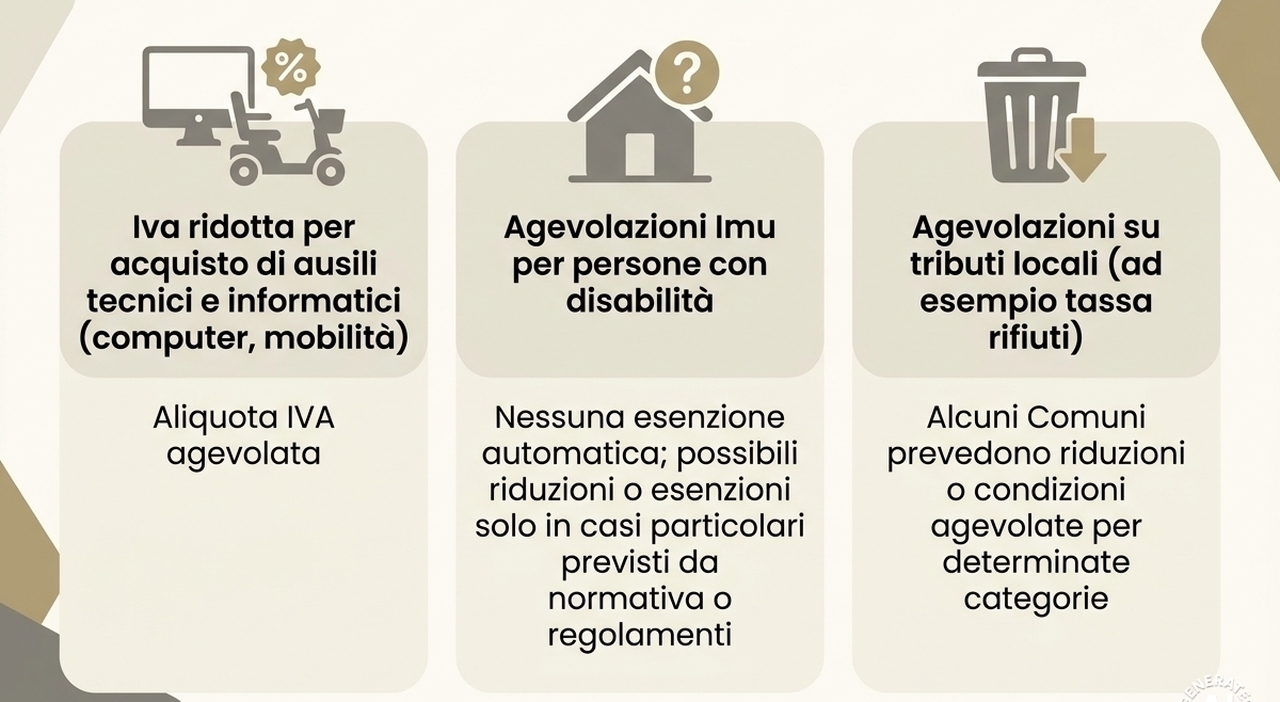

the purchase of such vehicles may also qualify for a reduced VAT rate of 4% (down from the standard 22%) and a deduction of 19% on the IRPEF (personal income tax) for the purchase cost, subject to specific limits. These benefits are regulated under the provisions set by the Law 104/1992, as amended by subsequent financial acts. It is imperative to check the most recent updates on the Agenzia delle Entrate portal annually, as thresholds and documentation requirements can be subject to legislative adjustments.

Addressing Common Misconceptions: IMU and Property Taxes

A frequent point of confusion among taxpayers concerns the IMU (Imposta Municipale Propria), the municipal tax on properties. A persistent question is whether Law 104 status grants an automatic exemption from IMU on a primary residence. The reality, as established by the Italian Ministry of Economy and Finance, is that disability status does not, in itself, provide an exemption from IMU.

However, there is an important nuance regarding the classification of the property. If a property is deemed a “luxury” home (categorized as A/1, A/8, or A/9), it is generally subject to IMU. For properties that are not luxury homes, the primary residence is typically exempt from IMU for all citizens, regardless of their disability status. The confusion often arises when a disabled person moves into a residential care facility (RSA). In such cases, if the municipality has passed specific bylaws, the former primary residence may be considered an “assimilated primary residence” and thus exempt from IMU, provided the person is a resident of the care facility and the property is not rented out. This is a matter of municipal autonomy, and taxpayers are advised to consult their local council’s specific regulations.

Key Takeaways for Taxpayers

To ensure you are managing your fiscal obligations correctly, keep these verified points in mind:

- Exemptions are targeted: Law 104 provides specific tax relief rather than total tax immunity. Always verify if your specific disability grade meets the criteria for the tax in question.

- Documentation is mandatory: Keep your verbale di invalidità (disability certification) updated and accessible. This document is the cornerstone of all claims.

- Vehicle limitations: The bollo auto exemption is tied to engine displacement and the requirement that the vehicle serves the disabled person’s mobility needs.

- Municipal variations: Always check with your local municipality (Comune) regarding property tax (IMU) policies for residents in care facilities.

- Use official portals: Rely exclusively on the Agenzia delle Entrate website for updates. Avoid third-party forums or unofficial blogs, as tax laws change frequently.

Frequently Asked Questions

Does Law 104 exempt me from all income taxes?

No. Law 104 provides specific deductions and tax credits for medical expenses and assistance, but it does not exempt an individual from paying personal income tax (IRPEF) on their overall earnings.

Can I claim the vehicle tax exemption for multiple cars?

Generally, the exemption is limited to one vehicle. If you replace your vehicle, you must inform the authorities to transfer the exemption to the new registration.

Where can I find the most recent forms for these exemptions?

All official forms and procedural guides can be downloaded directly from the Modulistica section of the Agenzia delle Entrate website. Always ensure you are using the most current version of any form.

As we look ahead, the Italian government periodically reviews welfare and fiscal policies in the annual Budget Law (Legge di Bilancio). Taxpayers should monitor official announcements in late autumn for any potential shifts in tax thresholds or administrative procedures. I encourage our readers to engage with their local tax professionals or the CAF (Centri di Assistenza Fiscale) for personalized guidance regarding their specific circumstances. If you found this analysis helpful, please share it with others who may be navigating these complex systems. I welcome your questions in the comments section below.

Related reading