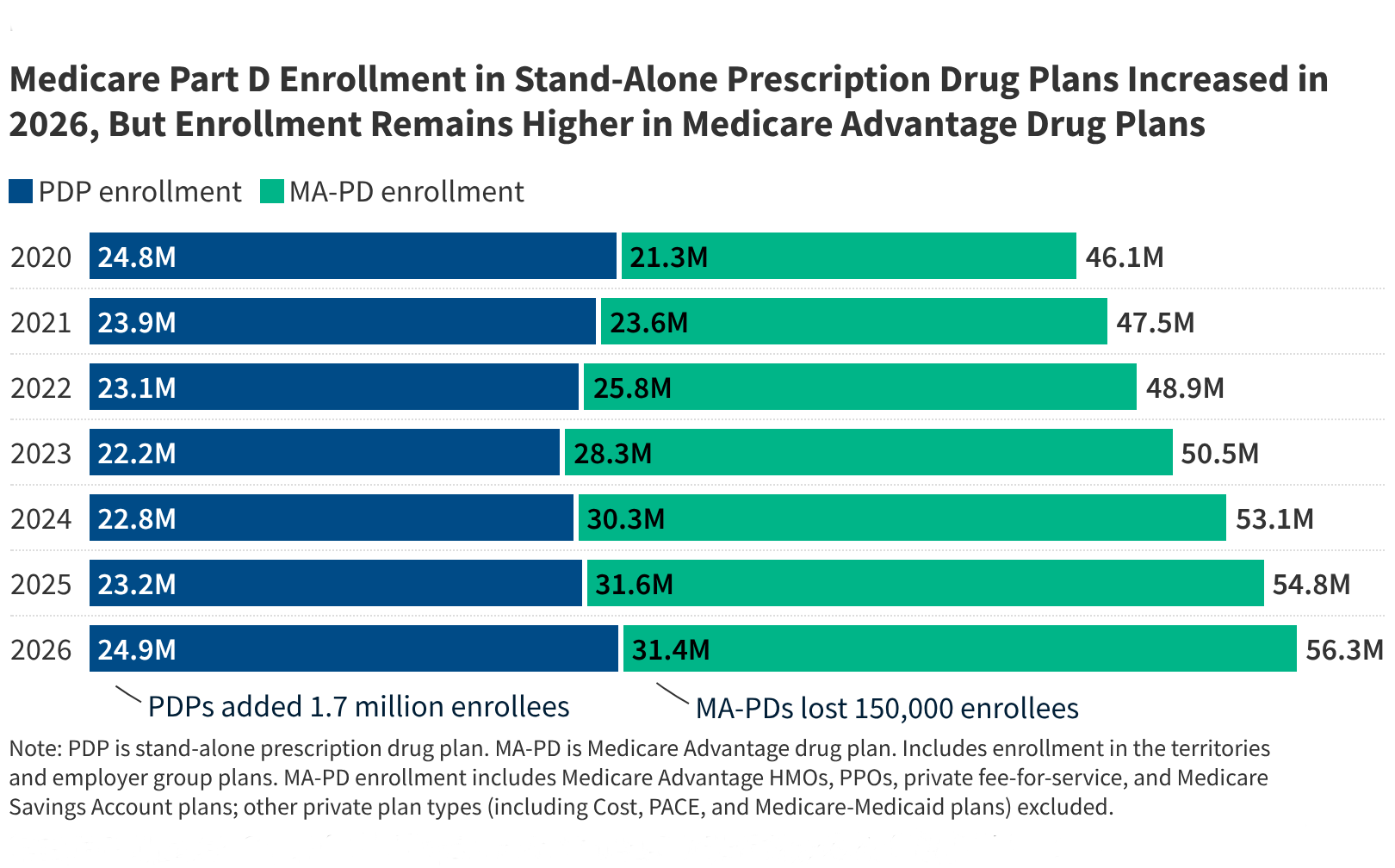

Medicare beneficiaries will encounter significant changes to the Part D prescription drug program in 2026, driven by ongoing implementation of the Inflation Reduction Act of 2022. For the approximately 56 million older adults and individuals with long-term disabilities enrolled in Medicare, the upcoming plan year introduces new caps on out-of-pocket spending and shifts in how insurance carriers manage plan designs, according to the Centers for Medicare & Medicaid Services (CMS).

As the Editor of Health at World Today Journal, I have monitored these policy shifts closely. The 2026 plan year marks a critical juncture where the $2,000 annual out-of-pocket cap on prescription drugs becomes fully operational for all beneficiaries. While this limit provides substantial financial protection for those with high medication costs, it has also prompted private insurers to adjust their monthly premiums and formulary structures to account for the new federal risk-sharing requirements.

Understanding the $2,000 Out-of-Pocket Cap

The most consequential change for 2026 is the implementation of a hard $2,000 limit on what beneficiaries pay out-of-pocket for covered Part D drugs. Under the provisions of the Inflation Reduction Act, this cap ensures that once a patient reaches this threshold, they no longer pay cost-sharing for the remainder of the calendar year. This replaces the previous “catastrophic coverage” phase, which historically required beneficiaries to pay 5% coinsurance even after reaching high spending levels.

For patients managing chronic conditions such as diabetes, rheumatoid arthritis, or cancer, this change removes a significant financial barrier. Previously, the lack of a total spending cap meant that individuals on high-cost specialty medications could face uncapped expenses. By establishing this ceiling, the federal government aims to increase predictability in healthcare budgeting for seniors, as reported by the Kaiser Family Foundation.

Trends in Medicare Part D Premiums

The shift toward a $2,000 cap has altered the financial landscape for private insurance carriers, leading to observable fluctuations in monthly premiums. Because insurers are now responsible for a larger portion of costs once a beneficiary hits the cap, many plans have adjusted their base premiums to maintain profitability and cover the increased actuarial risk. According to CMS data, premium volatility remains a primary concern for beneficiaries during the annual enrollment period.

It is important to note that premiums vary significantly by region and plan type. While some beneficiaries may see modest increases, others may find that their specific plan has consolidated its offerings to remain competitive. The government encourages enrollees to utilize the Medicare Plan Finder tool to compare the total estimated costs—including both premiums and out-of-pocket drug expenses—rather than focusing solely on the monthly premium amount.

Cost Sharing and Formulary Adjustments

Beyond premiums, insurers are refining how they categorize drugs within their formularies to manage the costs associated with the new benefit design. “Cost sharing” refers to the copayments or coinsurance a patient pays at the pharmacy counter. In 2026, many plans have reclassified certain high-cost medications into different tiers, which can change the amount a patient pays before hitting the annual cap.

Beneficiaries should review their plan’s “Evidence of Coverage” document to identify any changes to their specific medications. If a drug has moved to a higher tier, the patient’s copayment may increase, even if the total annual cost is limited by the $2,000 cap. This structural shift highlights the importance of reviewing plan documents annually, as even long-standing plans may alter their pharmacy networks or drug lists to align with current federal guidelines.

Key Takeaways for Beneficiaries

- Annual Cap: All Part D enrollees benefit from a $2,000 annual out-of-pocket maximum on prescription drugs, significantly reducing costs for those with high medical needs.

- Premium Variability: Plan premiums have shifted in response to the new benefit structure; beneficiaries should compare total annual costs rather than monthly premiums alone.

- Formulary Review: Insurers have adjusted drug tiers and pharmacy networks, necessitating a thorough check of each plan’s formulary for specific medications.

- Assistance Programs: Individuals with limited income may still qualify for the Extra Help program, which further subsidizes premiums and cost-sharing.

What Happens Next

The next major milestone for the Medicare program is the conclusion of the 2026 coverage year and the subsequent release of 2027 plan bids by insurance carriers. The Centers for Medicare & Medicaid Services is expected to release updated enrollment statistics and premium trend analysis in early 2027. Beneficiaries are advised to monitor the official Medicare.gov portal for any mid-year guidance or changes to the Medicare Advantage and Part D landscape. If you have questions about how these changes affect your specific coverage, consulting with a State Health Insurance Assistance Program (SHIP) counselor provides personalized, unbiased guidance.

How have these changes influenced your choice of plan this year? Please share your experiences or questions in the comments section below.

Worth a look