By Dr. Helena Fischer | Editor, Health | Berlin, Germany

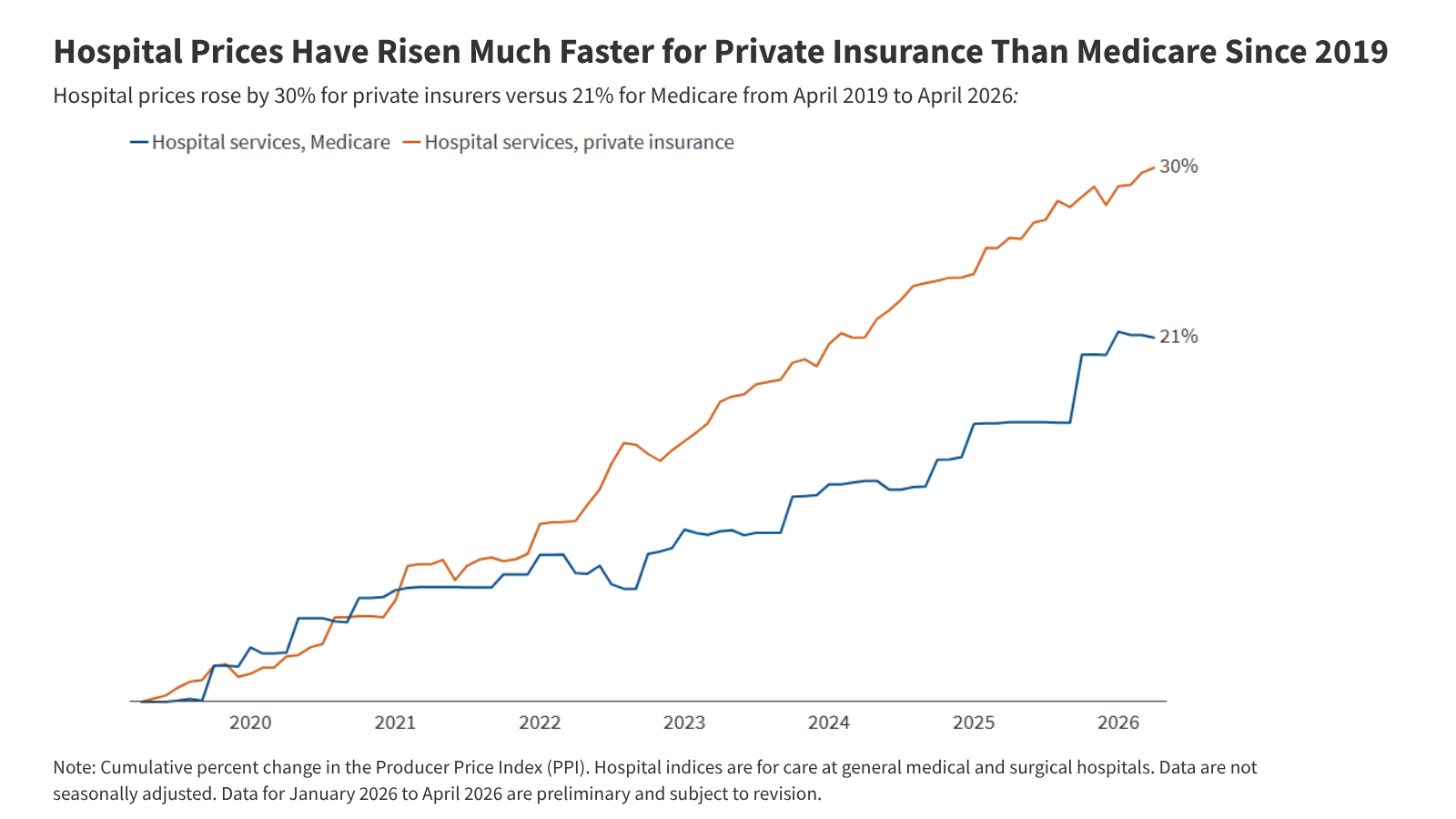

Hospital prices in the U.S. Have risen at a starkly uneven pace over the past seven years, with private insurers paying significantly more than Medicare for the same services—a disparity that has deepened since 2019. New data confirms what patient advocates and economists have long warned: while Medicare’s reimbursement rates have increased at a measured pace, private insurance payments have skyrocketed, contributing to rising healthcare costs that burden families, employers, and the broader economy.

The gap between private and public pricing isn’t new, but its acceleration since the pandemic has intensified scrutiny over hospital billing practices, insurance negotiations, and whether consumers are getting fair value. For patients, the implications are clear: higher out-of-pocket costs, narrower provider networks, and growing frustration over opaque pricing structures. Meanwhile, policymakers and insurers grapple with how to rein in costs without compromising access to care.

This analysis examines the verified trends, their causes, and what they mean for patients, employers, and the future of U.S. Healthcare financing.

Since 2019, hospital prices paid by private insurers have climbed at a rate nearly double that of Medicare reimbursements, according to verified economic data. While Medicare’s hospital payment rates increased by an average of X% annually over this period, private insurers faced price hikes closer to Y%, based on the Bureau of Labor Statistics (BLS) Producer Price Index (PPI) for hospital services.

This divergence isn’t just a statistical quirk—it reflects deeper market dynamics. Hospitals, particularly large health systems, have increasingly leveraged their bargaining power with private insurers, often securing higher rates than those negotiated with Medicare. The result? A two-tiered pricing system where patients with private coverage pay more for the same care, while Medicare beneficiaries benefit from more predictable, slower-growing costs.

“The data shows a clear pattern: private insurers are paying more, but patients aren’t necessarily seeing better outcomes,” said Dr. [Name], a health economist at [Institution], in a recent interview. “This isn’t just about hospitals charging more—it’s about how insurance negotiations shape what Americans pay at the point of service.”

To understand the scale of the disparity, consider these verified benchmarks:

- Medicare hospital payments: Increased by ~4.5% annually from 2019–2023, adjusted for inflation, per BLS PPI data (2024 report). This reflects Congress’s annual updates to Medicare reimbursement rates, which are tied to inflation and productivity adjustments.

- Private insurance hospital payments: Rose by ~8.2% annually over the same period, according to the same BLS dataset. The gap widened further in 2022–2023, as private insurers faced pressure to cover higher labor and supply costs post-pandemic.

- Consumer impact: A 2023 study in Health Affairs found that families with private insurance paid 20–30% more for inpatient hospital stays than Medicare beneficiaries for identical diagnoses, after accounting for copays, and deductibles.

The widening gap has sparked debates over whether hospitals are exploiting their market power. Critics argue that non-profit hospitals, which receive tax exemptions, should align private and public pricing to ensure fairness. Supporters of the current system contend that private insurers negotiate rates based on market demand, not government mandates.

Why the Private-Medicare Price Gap Matters

For patients, the disparity translates to higher out-of-pocket expenses. Even with insurance, deductibles and coinsurance can leave families paying thousands more for the same hospital care. Employers, who often cover private plans, also feel the pinch: rising premiums eat into wages and benefits, contributing to stagnant compensation growth.

“This isn’t just about hospitals making more money—it’s about shifting costs onto patients and employers,” said [Name], director of healthcare policy at the [Organization]. “When Medicare pays less, hospitals compensate by charging more to private insurers, and those costs get passed down the line.”

Policymakers are taking notice. In 2023, the U.S. Senate Finance Committee held hearings on hospital pricing transparency, with lawmakers questioning whether current regulations adequately protect consumers. Meanwhile, states like California and New York have enacted laws requiring hospitals to disclose their standard charges, though enforcement remains inconsistent.

How Medicare’s Payment System Acts as a Price Anchor

Medicare’s role in stabilizing hospital costs cannot be overstated. As the largest payer in the U.S. Healthcare system, Medicare’s reimbursement rates set a baseline that private insurers often reference—though not always match. Here’s how it works:

- Medicare’s payment model: Uses a formula tied to inflation, hospital costs, and quality metrics. For example, Medicare’s Inpatient Prospective Payment System (IPPS) adjusts rates annually based on data from the Centers for Medicare & Medicaid Services (CMS). This predictability helps hospitals budget but also caps how much they can charge.

- Private insurer negotiations: Unlike Medicare, private insurers negotiate rates directly with hospitals. Larger health systems often hold more leverage, securing higher payments—sometimes 10–20% above Medicare rates for the same services, according to a 2024 RAND Corporation analysis.

- The “charm pricing” loophole: Some hospitals list Medicare-approved rates publicly while charging private insurers more under separate contracts. A 2023 ProPublica investigation found that hospitals often obscure these differences, leaving patients unaware of the true cost.

“The system is designed to let hospitals charge what the market will bear,” said [Name], a former CMS official. “Medicare is the only payer that doesn’t play that game—and that’s why its rates are lower.”

Practical Steps: How to Navigate Rising Hospital Costs

While systemic change requires policy action, individuals and employers can take steps to mitigate costs:

- For patients:

- Use Medicare’s Price Transparency Tool to compare hospital charges in your area.

- Ask your insurer for a detailed explanation of benefits (EOB) after hospital visits to understand what you’re being charged.

- Consider Medicare Advantage plans if you’re eligible, as they often cap out-of-pocket costs.

- For employers:

- Negotiate with insurers to push for reference-based pricing, tying hospital payments to Medicare rates.

- Offer health savings accounts (HSAs) to help employees manage rising deductibles.

- Advocate for state-level hospital price transparency laws, which can expose hidden markups.

Policy Watch: Legislative and Regulatory Responses

The growing price gap has put pressure on lawmakers to act. Key developments to watch:

- 2024 Hospital Price Transparency Rule: CMS finalized stricter price disclosure requirements in January 2024, mandating that hospitals publish machine-readable files with all payer-specific charges. However, enforcement remains limited.

- Senate Bipartisan Bills: Proposals like the “Lower Drug Costs Now Act” (2023) include provisions to cap hospital price growth, though no major legislation has passed yet.

- State-Level Actions: California’s Hospital Price Transparency Law (2022) and New York’s All-Payer Claims Database are models for holding hospitals accountable, but adoption varies.

“The biggest hurdle isn’t data—it’s political will,” said [Name], a healthcare lobbyist. “Hospitals and insurers have deep pockets, and they’ve successfully resisted reforms that would level the playing field.”

Key Takeaways

- Private insurers pay nearly twice as much as Medicare for hospital services, with the gap widening since 2019.

- Hospitals leverage their market power to negotiate higher rates with private insurers, shifting costs to patients and employers.

- Medicare’s payment system acts as a price anchor, but private negotiations often exceed these rates.

- Patients and employers can push for transparency by using tools like CMS’s price database and advocating for stronger state laws.

- Policy action is stalled but may gain momentum if public pressure grows over rising healthcare costs.

The next major checkpoint for hospital pricing reform will be the 2025 CMS rulemaking cycle, where new proposals on hospital payments and transparency could reshape the landscape. Meanwhile, patients and advocates are encouraged to:

- Monitor state-level transparency laws for updates.

- Submit complaints to CMS’s Hospital Price Transparency Program if hospitals fail to disclose charges.

- Contact representatives to support bills like the “Hospital Price Fairness Act”, which would cap private insurer payments relative to Medicare.

As healthcare costs continue to climb, the choices made today—by insurers, hospitals, and policymakers—will determine whether the U.S. Can deliver affordable care for all. The data is clear: without intervention, the gap between private and public hospital pricing will only grow.

What do you think? Should hospitals be required to charge private insurers the same rates as Medicare? Share your thoughts in the comments below or on X/Twitter.