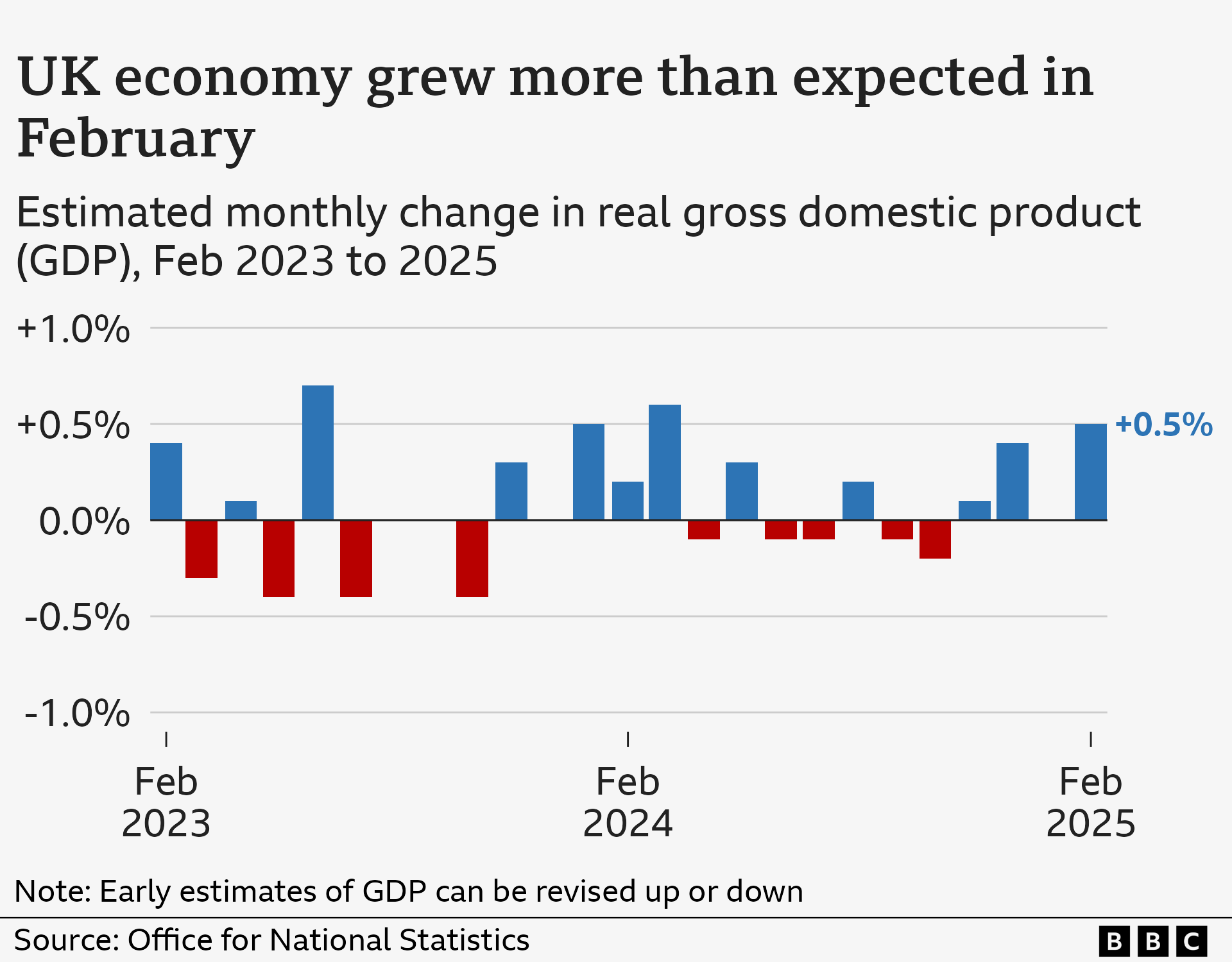

UK shares edged higher on Thursday morning as investors reacted to stronger-than-expected economic data and continued to monitor geopolitical developments in the Middle East. The positive momentum follows the release of February GDP figures, which showed growth driven by robust performance in the services and construction sectors.

The market’s optimism is further bolstered by signals from U.S. President Donald Trump regarding a potential resolution to the conflict with Iran. This combination of domestic economic resilience and the prospect of easing global tensions has created a supportive environment for British equities, particularly as investors recalibrate their expectations for future monetary policy.

The interplay between macroeconomic data and geopolitical stability remains the primary driver for the FTSE 100 and other major indices. While the GDP data provides a fundamental boost, the potential for a ceasefire in the Middle East serves as a catalyst for broader risk appetite across European markets.

Economic Growth Driven by Services and Construction

The primary catalyst for the early gains on Thursday was the release of February GDP data, which exceeded market expectations. This growth was largely attributed to a strong showing in the services sector and the construction industry, suggesting a level of resilience in the UK economy despite broader macroeconomic challenges.

Strong GDP figures typically signal a healthier economy, which can lead to increased corporate earnings and higher investor confidence. When the services sector—the largest component of the UK economy—performs well, it often creates a ripple effect that supports employment and consumer spending, further stabilizing the market.

Geopolitical Focus: U.S.-Iran Negotiations

Beyond the domestic data, market participants are closely tracking the potential for a ceasefire between the United States and Iran. On Wednesday, President Donald Trump indicated in an interview with Sky News that a permanent ceasefire agreement is “very possible,” noting that such a deal could be reached before King Charles visits later this month according to reports on the potential end of the conflict.

The prospect of easing tensions in the Middle East is critical for global markets because geopolitical instability in that region often leads to volatile oil prices. Lower volatility in energy markets generally reduces inflationary pressures, which in turn influences the decisions of central banks regarding interest rates.

The impact of these signals was evident on Wednesday, where some reports indicated the FTSE 100 closed up 1.8% and the FTSE 250 rose 2.2% as investors lowered their expectations for further interest rate hikes by the Bank of England following signals of a potential exit from the Iran war.

Mixed Performance Across European Markets

While the UK market showed strength, the broader European landscape presented a more fragmented picture. On Wednesday, the German DAX index saw modest gains, rising 0.2% in some reports, while the French CAC 40 experienced a decline of 0.6% as European markets moved in opposite directions.

This divergence highlights that while geopolitical easing is a global positive, local economic factors and specific corporate news continue to drive individual national indices. In the UK, the combination of positive GDP data and the specific reactions to U.S. Foreign policy has provided a more concentrated boost to the London markets.

Corporate Developments and Trade Concerns

Amidst the general market movement, specific corporate news has influenced individual stock prices. Aegon Ltd announced the sale of Aegon UK to Standard Life for £2 billion, a move resulting from a strategic review of its UK operations. This transaction includes 1.811 billion shares of Standard Life (a 15.3% stake) and £750 million in cash as part of the strategic divestment.

In the housing sector, Barratt Redrow PLC saw its share price rise by 1.2% after reaffirming its full-year home completion guidance. The company maintained its target of delivering between 17,200 and 17,800 homes for the 2026 financial year, including approximately 600 homes from joint venture projects, despite the uncertainties caused by Middle East conflicts maintaining its 2026 delivery targets.

However, not all news from the U.S. Administration was positive. President Trump suggested he might reconsider the terms of the trade agreement with the UK, citing disagreements with UK domestic policies and Prime Minister Keir Starmer. Trump mentioned that the current agreement was “better” than what he felt he had to give and noted that these terms “can always change” during his Sky News interview.

Summary of Market Drivers

| Driver | Nature | Impact |

|---|---|---|

| February GDP Data | Positive | Strong services and construction sectors pushed stocks higher. |

| U.S.-Iran Relations | Positive | Trump’s hints of a ceasefire reduced geopolitical risk and inflation fears. |

| Trade Policy | Negative/Uncertain | Trump’s comments on renegotiating UK trade terms introduced caution. |

| Corporate News | Mixed | Aegon sale and Barratt Redrow guidance provided specific stock movements. |

Investors will now look toward the actualization of the suggested ceasefire and the upcoming visit of King Charles to see if diplomatic progress translates into sustained market stability. Further updates on GDP trends and official statements regarding trade negotiations will be the next critical checkpoints for the London market.

We invite our readers to share their thoughts on how these geopolitical shifts are affecting your investment strategies in the comments below.