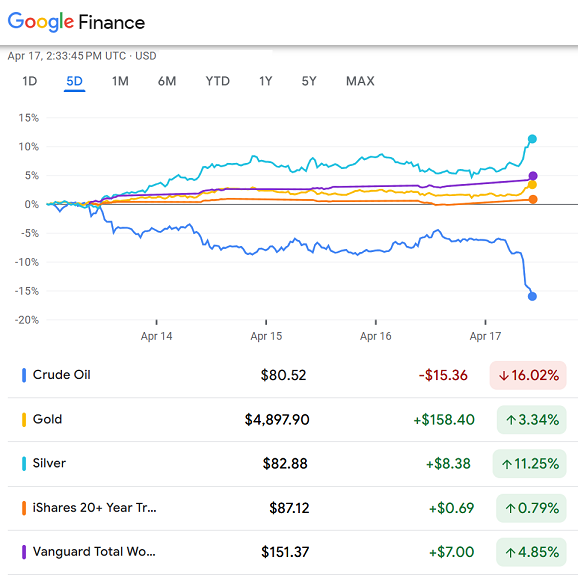

Global financial markets have shown notable shifts following recent developments in the Iran-U.S. Diplomatic landscape, with currency and commodity movements reflecting evolving investor sentiment. After weeks of heightened volatility tied to geopolitical tensions in the Strait of Hormuz, both the U.S. Dollar and gold prices have experienced downward pressure as diplomatic signals suggest a potential de-escalation of conflict. These movements arrive as markets reassess risk premiums previously embedded in asset prices amid fears of prolonged disruption to global oil flows.

The U.S. Dollar index (DXY), which measures the greenback against a basket of six major currencies, retreated from its recent highs after falling 0.53% on Tuesday, according to verified market data. This decline followed comments from President Trump indicating openness to ending the Iran war, reducing demand for the dollar as a safe-haven asset. The index had previously risen amid heightened risk aversion but has since returned to levels last seen in late February, prior to the escalation of military exchanges in the region.

Gold, traditionally viewed as a hedge against geopolitical instability and inflation, also saw its price ease as tensions eased. Spot gold traded lower after reaching multi-week highs earlier in the month, reflecting reduced safe-haven demand. Analysts noted that while gold remains sensitive to real interest rates and central bank policy, short-term fluctuations are often driven by shifts in geopolitical risk perception, particularly in regions critical to energy supply chains.

Broader market reactions have been mixed but increasingly oriented toward risk assets. U.S. Equities showed signs of stabilization, with the S&P 500 and Nasdaq paring earlier losses as investors weighed improving economic indicators against lingering inflation concerns. The Conference Board’s U.S. Consumer confidence index unexpectedly rose to 91.8 in March, surpassing forecasts of a decline to 87.9, suggesting resilience in household spending despite higher borrowing costs.

Meanwhile, energy markets responded to the de-escalation signals with mixed trends. While crude oil prices had surged earlier in the month due to fears of Strait of Hormuz closures, they began to retreat as the likelihood of sustained disruption diminished. However, upstream energy producers continue to monitor OPEC+ output decisions and global demand indicators, particularly from Asia, where industrial activity remains a key determinant of near-term price direction.

In fixed income, U.S. Treasury yields exhibited volatility, with 10-year note yields fluctuating in response to shifting inflation expectations and Federal Reserve communication. Kansas City Fed President Jeff Schmid’s hawkish remarks — emphasizing focus on inflation risks and concern over persistent price pressures near 3% — provided temporary support to the dollar earlier in the week, though this effect was outweighed by broader risk-off sentiment shifts following diplomatic developments.

The Chicago PMI, a key gauge of Midwestern manufacturing activity, came in weaker than expected at 52.8 in March, down from 55.0 forecast, signaling ongoing stress in the industrial sector. Conversely, stronger-than-anticipated consumer confidence and mixed JOLTS job openings data — which showed a slight decline to 6.882 million from 6.890 million — painted a complex picture of U.S. Economic resilience amid sectoral disparities.

Internationally, currency pairs reflected the dollar’s retreat. The euro edged lower against the greenback despite broader risk-aversion trends, influenced by lingering growth concerns in the eurozone and the European Central Bank’s cautious stance on rate cuts. The Japanese yen and British pound also experienced modest fluctuations as traders recalibrated positions based on relative monetary policy outlooks and safe-haven flows.

Market analysts continue to emphasize that while diplomatic progress reduces immediate tail risks, structural challenges remain. Persistent inflation, uneven global growth, and divergent central bank policies are expected to maintain volatility elevated across asset classes. Investors are advised to monitor upcoming inflation reports, central bank minutes, and official statements from diplomatic channels for further clarity on the trajectory of both geopolitical risk and monetary policy.

The next key checkpoint for markets will be the release of the U.S. Personal Consumption Expenditures (PCE) price index for March, scheduled for April 30, 2026 — the Federal Reserve’s preferred inflation measure. This data will play a crucial role in shaping expectations around the timing and pace of potential interest rate adjustments in the coming months.

For ongoing coverage of global market movements, economic policy shifts, and geopolitical developments affecting finance, readers are encouraged to follow trusted financial news sources and official economic calendars. Share your insights on how evolving diplomatic dynamics may influence investment strategies in the comments below.