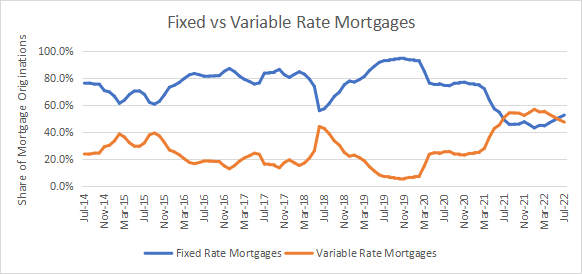

Reports regarding the Italian housing market indicate a shift in borrowing patterns within the Lazio region, where the average amount requested for mortgages is reportedly on the rise. This trend coincides with a growing interest in variable rate mortgages, a move analysts suggest is closely tied to current interest rate trajectories.

For borrowers navigating this landscape, the choice between fixed and variable options remains a critical financial decision. Recent data points to specific financing scenarios, such as loans of 126,000 euros extended over 25-year terms, as benchmarks for those seeking the most competitive rates in the current environment.

As Chief Editor of Business at World Today Journal, I have observed that such regional shifts often mirror broader economic sentiments. When borrowers lean toward variable rates, they are typically betting on a stabilizing or declining interest rate environment, hoping to benefit from lower initial payments compared to the security of a fixed-rate loan.

The Mechanics of Variable Rate Mortgages

To understand why borrowers in regions like Lazio might be shifting their strategy, it is essential to understand how a variable rate mortgage actually functions. Unlike a fixed-rate loan, where the interest remains constant for the duration of the term, a variable rate is fluid, fluctuating based on the movements of the financial market.

The primary benchmark for these loans in Europe is the Euribor (Euro Interbank Offered Rate). According to guidance from BNL, the interest rate of a variable mortgage is determined by the sum of the Euribor index and a “spread”—a fixed percentage added by the bank to ensure profitability.

The Euribor index can have different maturities, typically 1, 3, or 6 months, depending on the specific terms of the loan’s installment plan. This means that if the Euribor rate rises, the monthly mortgage payment increases; conversely, if the Euribor falls, the borrower benefits from a lower monthly installment.

Balancing Risk and Reward in Home Financing

The appeal of the variable rate often lies in the “entry price.” Historically and typically, the initial interest rate for a variable mortgage is lower than that of a fixed-rate alternative. For a household in Lazio looking to maximize their purchasing power at the start of a loan, this can make the difference between qualifying for a home or being priced out of the market.

But, this lower starting point comes with inherent volatility. Because the rate can change throughout the entire amortization period, borrowers are exposed to market risk. If global economic conditions drive interest rates upward, the monthly financial burden on the homeowner increases, which can strain household budgets over a 25-year horizon.

For those comparing current offers, platforms such as MutuiOnline provide tools to track the lowest available rates and calculate potential installments based on current market conditions.

Market Implications for the Lazio Region

The reported increase in the average loan amount requested in Lazio suggests a potential increase in property valuations or a higher appetite for risk among local buyers. When the average requested amount grows, it indicates that buyers are either targeting more expensive properties or are feeling confident enough in their long-term financial stability to take on larger debts.

The link between these larger loan amounts and the preference for variable rates suggests a strategic calculation. In a scenario where a borrower is requesting a significant sum—such as the 126,000 euro figure mentioned in recent reports—the difference between a fixed and variable rate can result in substantial monthly savings during the initial years of the loan.

Key Comparison: Fixed vs. Variable Rates

| Feature | Fixed Rate | Variable Rate |

|---|---|---|

| Interest Rate | Constant throughout the term | Fluctuates based on Euribor + Spread |

| Initial Cost | Generally higher | Generally lower |

| Predictability | High (payments never change) | Low (payments vary with market) |

| Market Risk | Protected from rate hikes | Exposed to rate hikes |

What This Means for Global Borrowers

While the current focus is on the Lazio region, the dynamics are universal. The tension between the desire for lower initial costs and the need for long-term certainty is a hallmark of global real estate markets. Borrowers are encouraged to evaluate their risk tolerance carefully before committing to a variable structure, especially for long-term loans exceeding 20 years.

Prospective homeowners should prioritize understanding the specific Euribor maturity tied to their loan (1, 3, or 6 months), as this dictates how quickly their payments will react to market changes. Consulting with financial advisors to stress-test a budget against potential rate increases is a prudent step for anyone opting for a variable path.

The next critical checkpoint for borrowers will be the upcoming updates to European central bank policies and the subsequent movement of the Euribor index, which will determine whether the current trend toward variable rates in Italy remains sustainable.

Do you believe variable rates are a calculated risk or a dangerous gamble in today’s economy? Share your thoughts in the comments below or share this analysis with your network.