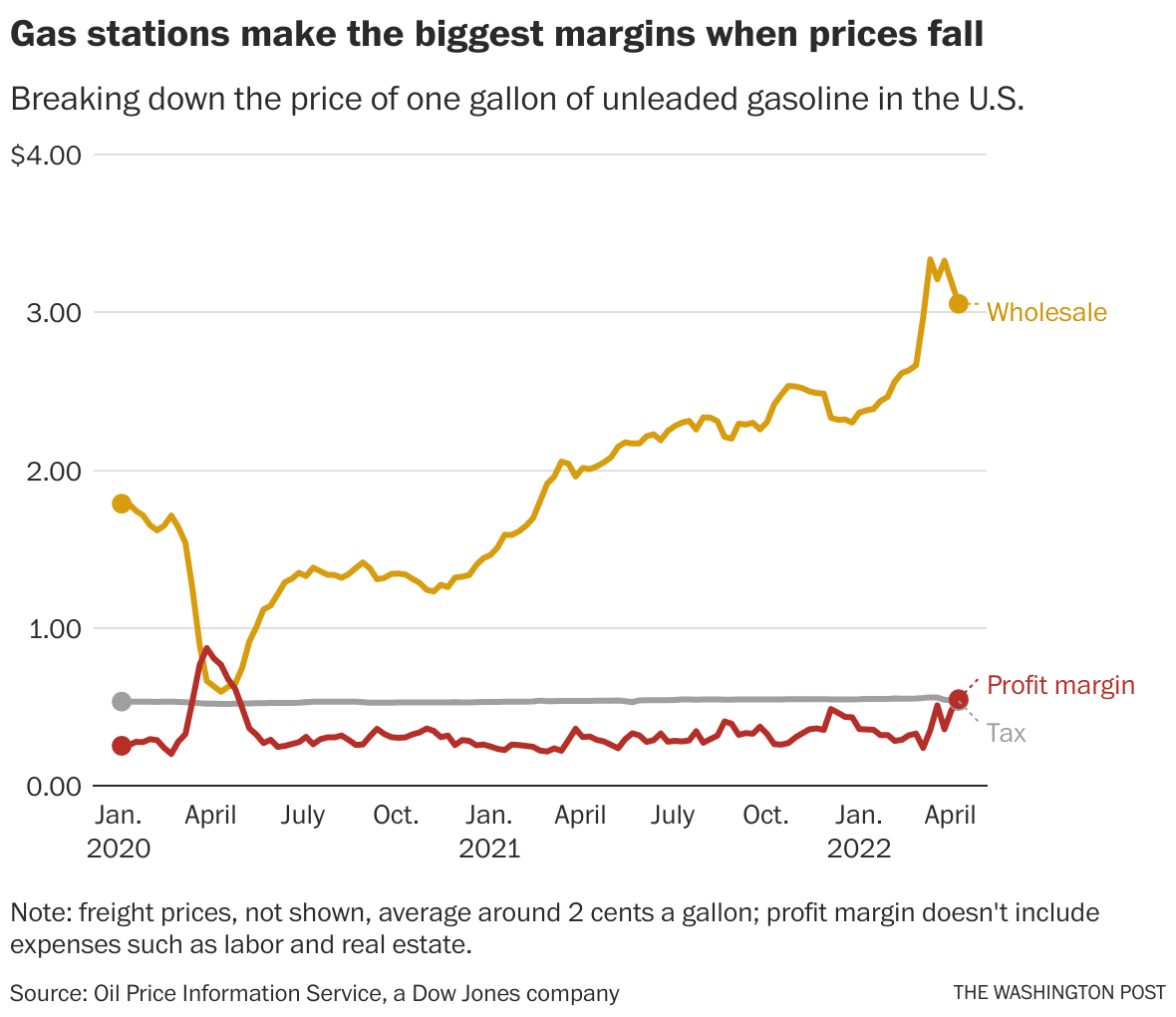

Retail fuel prices often remain elevated long after global crude oil costs decline, a phenomenon frequently attributed to the asymmetric nature of market pricing and the logistical lag in supply chain adjustments. While consumers frequently observe that gasoline prices rise rapidly in response to supply shocks, they often decrease at a significantly slower pace, leading to public frustration and scrutiny of industry pricing strategies. This pricing behavior, often described by economists as “rockets and feathers,” reflects a complex interplay between wholesale market dynamics, local competition, and the strategic management of profit margins by fuel retailers.

The primary driver of the discrepancy between crude oil prices and retail pump prices is the distinction between commodity markets and retail markets. Crude oil is traded on global exchanges, where prices fluctuate second-by-second based on geopolitical events, production quotas set by organizations like OPEC+, and global demand forecasts, according to the International Energy Agency. In contrast, gasoline sold at local stations is a refined product that has undergone complex processing, transportation, and regional taxation, all of which act as “sticky” costs that do not fluctuate as rapidly as the underlying raw material.

Understanding the Mechanics of Retail Fuel Pricing

Fuel retailers operate with relatively thin margins, meaning they are highly sensitive to wholesale price volatility. When wholesale costs rise, stations often pass these increases to the consumer immediately to protect their cash flow and ensure they can afford the next shipment of fuel. However, when wholesale costs drop, retailers may hold prices higher for longer to recover losses incurred during periods of price spikes or to build a buffer against future market instability. This strategy is not necessarily evidence of collusion, but rather a reflection of the competitive landscape in specific regions, where stations weigh the benefits of market share against the need for stable revenue, as noted by the U.S. Federal Trade Commission regarding gasoline price transparency and competition.

Furthermore, the “replacement cost” model plays a significant role in how stations set their prices. A station owner must consider what it will cost to replace the fuel currently in their underground tanks. If a retailer sells their current stock at a lower price point as soon as the global market dips, they risk being unable to afford the subsequent wholesale delivery if prices rebound. Consequently, price adjustments at the pump often trail market movements by several days or even weeks.

The Role of Taxes and Operational Costs

Retail prices are also insulated from crude oil volatility by a high floor of fixed costs. In many European and North American jurisdictions, a substantial portion of the price at the pump consists of excise taxes, environmental levies, and value-added taxes, which remain constant regardless of the price of a barrel of oil. According to the European Commission’s energy price reporting, these non-commodity components can account for more than 50% of the final retail price in some regions, effectively muting the impact of a drop in crude oil prices on the consumer’s final bill.

Operational overhead, including transportation from refineries to terminals and finally to local stations, adds another layer of cost. These logistics costs are largely driven by labor and energy prices—such as the electricity or natural gas required to operate pumps and station facilities—which have remained high despite fluctuations in the global oil market. Because these overheads do not decrease when oil prices fall, the room for retailers to lower prices is inherently limited.

Market Competition and Consumer Behavior

The speed at which prices fall is also influenced by local market saturation. In areas with high competition, stations are more likely to lower prices quickly to attract volume-driven traffic. Conversely, in regions with fewer competitors, there is less pressure to pass on savings to consumers. Retailers are aware that consumers are generally more sensitive to price increases than they are to price decreases, a psychological factor that influences pricing strategies. When prices are high, consumers may cut back on discretionary driving, but once they have adjusted their budgets to a certain price level, retailers may maintain those levels to sustain profit margins, provided that demand does not drop below a critical threshold.

The U.S. Energy Information Administration monitors these retail trends, noting that localized data often reveals significant price disparities even within the same state or city. These variations are frequently linked to differences in regional distribution networks, local regulatory requirements, and the specific procurement contracts individual station owners have with their suppliers.

What Happens Next?

Market analysts continue to monitor global supply levels as a primary indicator for future price trends. Upcoming reports from major energy agencies, including the next scheduled updates on global oil inventories and demand projections, will provide further clarity on whether current retail price levels will stabilize or face downward pressure. Consumers seeking the most accurate information on local fuel pricing should monitor official government energy portals or reputable industry trackers that aggregate real-time data from regional stations. Readers are encouraged to share their observations on local fuel trends in the comments section below or join the ongoing discussion regarding energy market transparency.