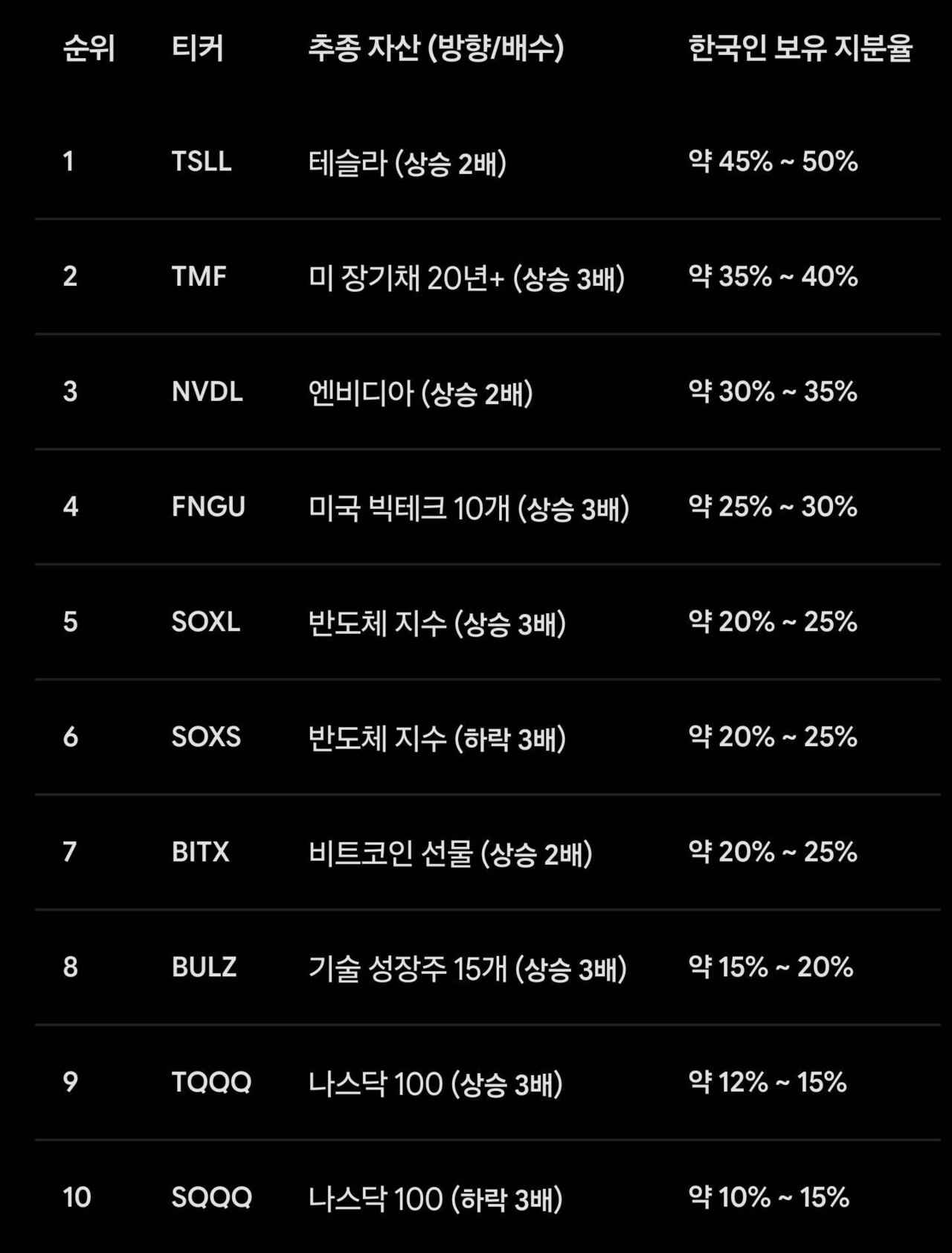

South Korean retail investors have established a dominant presence in the global market for leveraged exchange-traded products (ETPs), frequently accounting for the highest trading volumes in high-risk, high-reward instruments relative to the country’s population size. Data indicates that these investors, often referred to as “Seohak Ants” when investing in overseas markets, show a marked preference for aggressive, short-term betting strategies, particularly in U.S.-listed leveraged and inverse ETFs that track indices like the Nasdaq-100 or the semiconductor sector.

This trend has drawn significant attention from financial regulators and market analysts, who point to the unique intersection of high digital literacy, a pervasive “all-in” investment culture, and the rapid adoption of mobile trading platforms as primary drivers. While the appetite for risk is a documented global phenomenon, the intensity of South Korean participation in volatile assets has become a distinct feature of the domestic financial landscape, often sparking debates regarding investor protection and the long-term sustainability of such high-stakes trading behaviors.

The Mechanics of High-Intensity Retail Participation

The prevalence of South Korean retail investors in leveraged trading is not merely anecdotal; it is reflected in cross-border capital flow data. According to reports from the Korea Securities Depository (KSD), the volume of foreign stock holdings by South Korean individuals has surged over the past five years, with a significant portion of this capital flowing into triple-leveraged ETFs, which aim to provide three times the daily return of an underlying index. The Korea Exchange (KRX) has frequently monitored these inflows, noting that the retail segment often acts as a contrarian force, doubling down on positions during periods of extreme market volatility.

Financial analysts suggest that this behavior is rooted in a cultural paradigm that prioritizes rapid wealth accumulation. In a society where real estate prices have historically outpaced wage growth, many younger investors view the stock market—and specifically leveraged derivatives—as one of the few viable avenues for significant upward mobility. This “gamified” approach to finance is facilitated by low-commission trading apps and a highly connected social media environment where investment tips and success stories regarding leveraged gains circulate rapidly.

Regulatory Oversight and Investor Risks

The Financial Supervisory Service (FSS) in South Korea has issued multiple warnings regarding the inherent risks of leveraged and inverse products. These instruments are mathematically designed for short-term holding; due to the effects of “volatility drag” and daily rebalancing, holding these assets over extended periods can lead to significant capital erosion, even if the underlying index remains relatively stable. The Financial Supervisory Service has implemented mandatory education requirements and stricter eligibility criteria for retail investors attempting to trade certain high-risk derivatives to mitigate these outcomes.

Despite these interventions, the allure of outsized returns remains a powerful motivator. Market participants often focus on the potential for quick profits, sometimes discounting the mathematical reality of compound losses. Institutional observers have noted that while the high level of participation demonstrates a sophisticated understanding of digital trading tools, it also exposes a vulnerable demographic to systemic market shocks, particularly when leveraged positions are held through major corrections.

Demographic Shifts and the Future of Trading

The demographic profile of these investors is notably skewed toward the younger generation, specifically those in their 20s and 30s. This cohort is characterized by a high degree of comfort with online forums and community-driven investment strategies. Platforms like Blind, an anonymous professional network, have become hubs for this discourse, where users share real-time updates on their leveraged positions and coordinate sentiment around specific tickers. This collective behavior has occasionally been compared to the retail-driven “meme stock” phenomenon seen in other global markets, though with a more sustained focus on index-linked derivatives rather than individual company equities.

The trend shows little sign of abating as long as global indices remain volatile, providing the price swings that leveraged traders seek. However, the long-term impact on the personal balance sheets of these investors remains a primary concern for policymakers. As the OECD continues to monitor household debt and financial literacy levels across member nations, the South Korean case study of retail leverage serves as a prominent example of how technology-enabled access to complex financial products can reshape national investment patterns.

Next Steps for Market Observers

Market analysts will be looking toward the next quarterly report from the Korea Securities Depository for updated figures on retail foreign stock holdings and trading turnover. Additionally, any forthcoming policy adjustments from the Financial Services Commission (FSC) regarding the accessibility of overseas leveraged products will be a critical indicator of how the government intends to balance market freedom with the mandate for investor protection. Readers interested in tracking these shifts can find official policy updates and market data releases on the Financial Services Commission official website. We invite readers to share their observations on these market trends in the comments section below.