Navigating the complexities of the Italian real estate market requires more than just a keen eye for architecture; it demands a strategic approach to financing. For many aspiring homeowners, whether they are local residents or international investors, the process of securing a mutuo (mortgage) can feel like a daunting bureaucratic hurdle. However, understanding the current lending landscape in 2026 reveals a market that, while rigorous, offers diverse pathways to property ownership.

In recent digital trends, short-form content has grow a primary gateway for financial literacy, with creators attempting to distill complex banking processes into accessible snippets. While these “shorts” often highlight the immediate desire to open a mortgage

, the reality of the Italian banking system involves a detailed interplay of credit scoring, collateral requirements and regulatory compliance overseen by the Banca d’Italia.

As a financial journalist with nearly two decades of experience in global markets, I have observed that the Italian mortgage market is uniquely characterized by its stability and its adherence to conservative lending ratios. For those looking to enter the market today, the journey begins not with the application, but with a comprehensive assessment of financial solvency and the specific type of loan that aligns with their long-term economic goals.

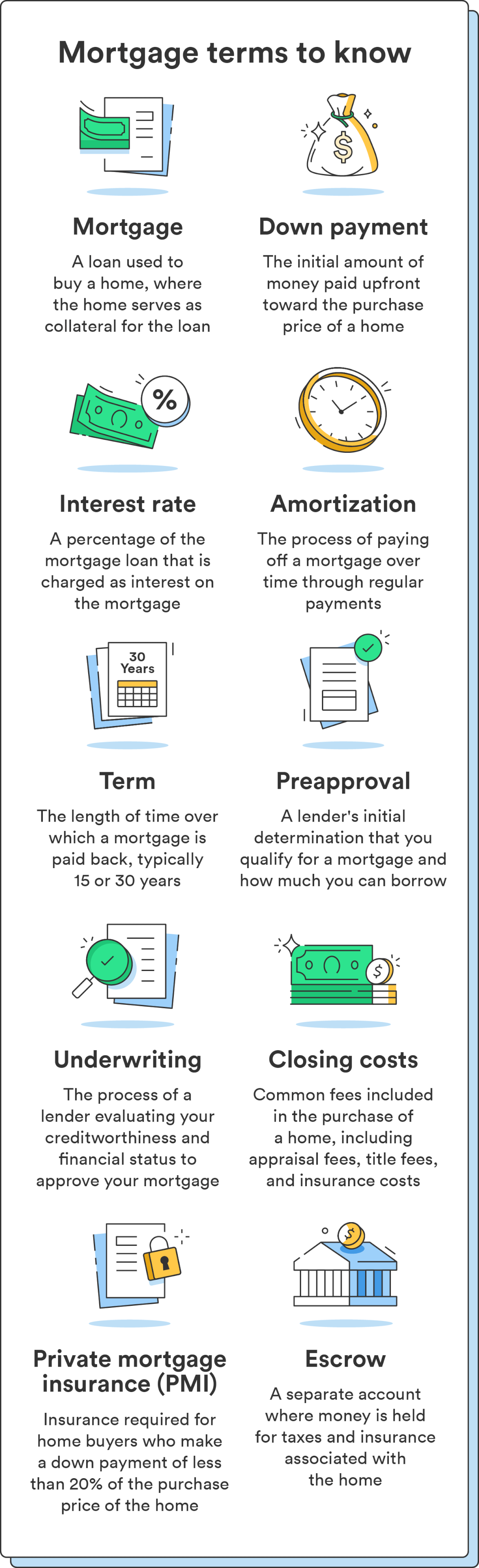

Understanding the Italian Mutuo: Core Mechanics

A mutuo ipotecario is a medium-to-long-term loan, typically spanning from 5 to 30 years. Unlike a standard personal loan, a mortgage is secured by the property itself, which serves as collateral. According to the Banca d’Italia, the borrower generally receives the total sum in a single disbursement and repays it over time through installments that may be fixed or variable.

The choice between these two primary structures is the most critical decision a borrower makes:

- Fixed-Rate Mortgages (Tasso Fisso): The interest rate remains constant throughout the entire duration of the loan. This provides maximum predictability and protection against rising inflation or central bank rate hikes.

- Variable-Rate Mortgages (Tasso Variabile): The rate fluctuates based on a market index, most commonly the Euribor. While these often start with lower initial payments, they expose the borrower to the risk of increasing costs if market rates climb.

For many first-time buyers, particularly those under 36, the Italian government has historically provided support through the Fondo di garanzia mutui per la prima casa

(First Home Loan Guarantee Fund). Managed by Consap and established under the Ministry of the Economy and Finance, this fund provides a public guarantee that allows eligible borrowers to access higher loan-to-value ratios than would typically be permitted by private banks alone, as noted by the Associazione Bancaria Italiana (ABI).

The Challenge for International Buyers

For non-residents or expatriates, the process of securing a mortgage in Italy involves additional layers of scrutiny. While there are no legal restrictions preventing foreign nationals from borrowing, Italian banks often apply stricter lending criteria to those with income sourced from outside the European Union.

International buyers typically face a lower Loan-to-Value (LTV) ratio. While a resident might secure a mortgage for 80% of the property’s value, a non-resident may be required to provide a down payment of 30% to 50%. This ensures the bank has a significant cushion against potential defaults in jurisdictions where debt recovery is more complex.

To bridge this gap, many investors utilize specialized credit brokerage firms. These intermediaries help align the buyer’s documentation—such as foreign tax returns and proof of income—with the specific requirements of Italian credit institutes. Such services are essential for navigating the “paperwork” phase, which includes obtaining a Codice Fiscale (tax code) and opening a local bank account.

Key Requirements for a Successful Application

Regardless of residency, banks in 2026 prioritize a sustainable debt-to-income ratio. Generally, monthly mortgage payments should not exceed 30% to 35% of the household’s net monthly income. To satisfy this requirement, applicants must provide:

- Proof of Income: Recent payslips, employment contracts (permanent contracts are highly preferred), or certified tax returns for the self-employed.

- Credit History: A clean record with no history of defaults or late payments.

- Property Appraisal: A formal valuation conducted by a certified technician to ensure the property’s market value supports the loan amount.

Strategic Considerations for 2026

In the current economic climate, the “cost of borrowing” is influenced heavily by the European Central Bank’s (ECB) monetary policy. Prospective borrowers should be aware that the total cost of a mortgage extends beyond the interest rate. Closing costs, including notary fees, registration taxes, and bank administrative charges, can add significantly to the initial investment.

the rise of “green mortgages” (mutui verdi) has introduced more favorable terms for those purchasing or renovating energy-efficient homes. Properties with high energy ratings (Class A or B) may qualify for lower interest rates or specialized subsidies, reflecting a broader European shift toward sustainable urban development.

Comparison of Mortgage Types in Italy

| Feature | Fixed Rate (Tasso Fisso) | Variable Rate (Tasso Variabile) |

|---|---|---|

| Payment Stability | Constant throughout the term | Fluctuates with market indices |

| Risk Level | Low (protected from rate hikes) | Moderate to High (market dependent) |

| Initial Cost | Generally higher starting rate | Generally lower starting rate |

| Ideal For | Risk-averse buyers, long-term stays | Short-term owners, falling rate environments |

Final Steps Toward Home Ownership

The transition from searching for a property to signing the final deed (rogito) involves a precise sequence of events. Once a mortgage is pre-approved, the buyer typically signs a preliminary contract (compromesso), which outlines the terms of the sale and the deposit paid. The bank then performs a final audit of the property and the borrower’s financial status before the funds are released at the notary’s office.

For those overwhelmed by the process, the most effective strategy is to seek a “pre-approval” or voucher from a bank. This document confirms the maximum amount the bank is willing to lend, turning the buyer into a more competitive bidder in a tight real estate market.

The next critical checkpoint for many borrowers will be the upcoming quarterly updates from the European Central Bank regarding interest rate trajectories, which will directly influence the competitiveness of variable-rate offers throughout the remainder of 2026.

Do you have experience navigating the Italian banking system, or are you planning a property purchase in Italy? Share your thoughts and questions in the comments below.