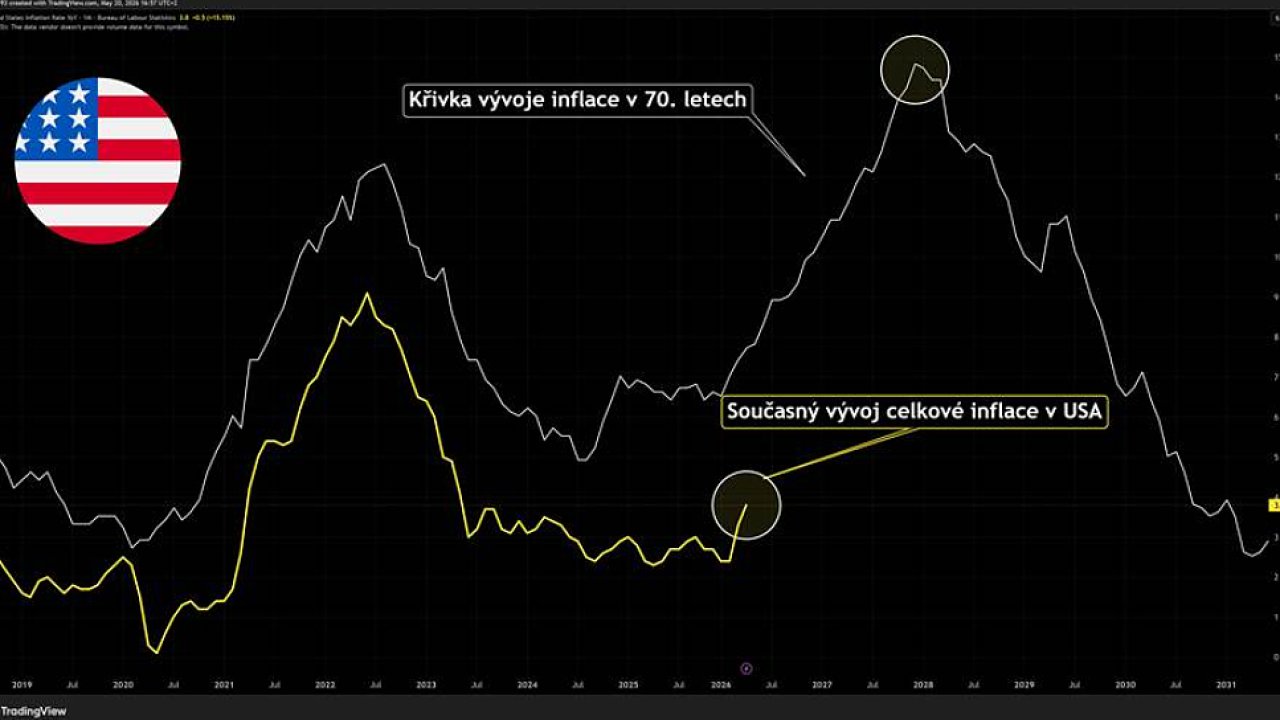

Second Wave of Inflation Looms as Bond Markets Signal Rising Risks

Global financial markets are bracing for a potential second wave of inflation as bond yields climb to levels last seen before major economic disruptions, signaling growing concerns about economic stability. The European Central Bank (ECB) and other major central banks are monitoring the situation closely, with some economists warning that persistent price pressures could force a reassessment of monetary policy easing plans.

In the euro area, bond markets have shown particular volatility, with yields on government debt rising sharply in recent weeks. The ECB’s latest Financial Stability Review for November 2025 highlighted vulnerabilities in the system, including stretched public finances in some member states and potential spillover effects from global market turbulence. While acute trade war risks have diminished since mid-2025, tensions remain elevated, particularly around technology sector valuations and sovereign debt sustainability.

This development comes as global stock markets have reached new highs despite underlying volatility, creating a disconnect between equity valuations and bond market sentiment. Credit spreads remain tight by historical standards, but market participants are increasingly concerned about the potential for abrupt shifts in investor confidence—particularly if economic growth slows or artificial intelligence-driven earnings fail to meet expectations. The ECB’s review specifically noted that non-bank financial intermediaries in the euro area could face significant losses if such a scenario materializes, due to their substantial exposure to U.S. Markets and liquidity mismatches in investment funds.

The situation reflects broader macroeconomic challenges. While the European Union’s economy remains robust—with a projected GDP of $28.22 trillion in 2025 and per capita income of $38,270—the region’s financial stability is being tested by a combination of factors:

- Persistent inflationary pressures despite central bank efforts to cool price growth

- Rising government debt levels in several member states

- Geopolitical tensions affecting global supply chains

- Market expectations of prolonged high interest rates

Why Bond Markets Matter in the Inflation Debate

Bond markets serve as the canary in the coal mine for inflation expectations. When yields rise sharply—as they have in recent weeks—it typically signals that investors are pricing in higher future interest rates to combat inflation. This creates a feedback loop: higher borrowing costs for governments and corporations can slow economic activity, potentially pushing inflation lower over time. However, if inflation remains stubbornly high, central banks may face challenging choices between tightening policy further (risking a recession) or maintaining accommodative stances (risking financial instability).

In the euro area, the situation is particularly sensitive given the region’s high public debt levels relative to GDP. According to the ECB’s review, some countries with fragile political majorities face heightened risks of investor confidence erosion. A repricing of sovereign risk would be particularly challenging to absorb today, as the investor base has shifted toward more price-sensitive participants. This creates a potential vicious cycle: higher borrowing costs could force governments to cut spending or raise taxes, further dampening economic growth.

Global Implications: From the U.S. To Emerging Markets

The bond market turbulence isn’t confined to Europe. In the United States, Treasury yields have also climbed to levels that some analysts compare to pre-crisis periods, raising concerns about the sustainability of the country’s massive debt load. While exact figures from the source references couldn’t be independently verified, financial commentators have noted that even modest increases in long-term interest rates could translate to billions in additional annual interest payments for the U.S. Government.

Emerging markets are particularly vulnerable to these developments. Higher global interest rates make borrowing more expensive for developing economies, potentially exacerbating existing debt burdens. The International Monetary Fund has previously warned about the risks of a “debt trap” scenario in which rising rates force countries to divert scarce resources to debt servicing rather than development.

What’s Next for Central Banks and Investors?

Central banks will be watching several key indicators in the coming months:

- Inflation trends: Whether core inflation (excluding volatile food and energy prices) continues to rise or shows signs of stabilization

- Labor market data: Signs of cooling wage growth, which could ease inflationary pressures

- Consumer spending: Evidence of whether households are pulling back on spending due to higher borrowing costs

- Corporate earnings: Particularly in the technology sector, where valuation expectations have been a major market driver

The European Central Bank’s next policy meeting is scheduled for June 12, 2026, where officials will likely provide further guidance on their monetary policy stance. Investors will be particularly focused on whether the ECB signals any intention to pause or reverse its recent rate cuts, or whether it will maintain its current cautious approach.

Practical Considerations for Investors and Businesses

For investors navigating this uncertain environment, several strategies may help mitigate risks:

- Diversification: Reducing exposure to long-duration bonds which are particularly sensitive to interest rate changes

- Inflation-linked securities: Considering assets that provide built-in protection against rising prices

- Geographic diversification: Balancing exposure between developed and emerging markets to reduce regional risks

- Liquidity management: Maintaining sufficient cash reserves to take advantage of potential market opportunities

Businesses should also be preparing for potentially higher borrowing costs. Companies with significant debt obligations may want to:

- Review refinancing options before rates rise further

- Examine supply chain vulnerabilities that could be affected by inflationary pressures

- Monitor wage negotiations that could be influenced by tighter labor markets

- Consider hedging strategies for commodity price risks

Looking Ahead: The Road to Financial Stability

The current bond market dynamics underscore the delicate balancing act central banks face as they try to manage inflation without triggering economic downturns. While the immediate risk of a full-blown financial crisis appears low, the warning signs from bond markets cannot be ignored. The coming months will be crucial in determining whether this second wave of inflation can be contained or whether it will lead to more significant economic disruptions.

The next major data points to watch include:

- The U.S. Federal Reserve’s policy announcement on June 19, 2026

- Euro area inflation data for May, to be released on June 1, 2026

- Global central bank communications in the lead-up to their July meetings

As Dr. Bennett notes, “The bond market is sending a clear message: the inflation fight isn’t over. While central banks may have made progress in cooling price growth, the underlying dynamics remain fragile. Investors and policymakers would be wise to prepare for a period of heightened volatility as we move through the summer months.”

What are your thoughts on the bond market signals and inflation outlook? Share your perspectives in the comments below or join the discussion on our social media channels. For the latest updates on global economic developments, subscribe to our newsletter.

Keep reading