The global economy is currently navigating a complex transition, attempting to move past the volatile shocks that defined the early 2020s. For investors and policymakers, the primary challenge lies in determining whether the current trajectory represents a sustainable stabilization or a fragile truce with inflation. Understanding the global economic outlook requires a retrospective look at the unique pressures of 2022, a year that fundamentally shifted the macroeconomic landscape for developed and emerging markets alike.

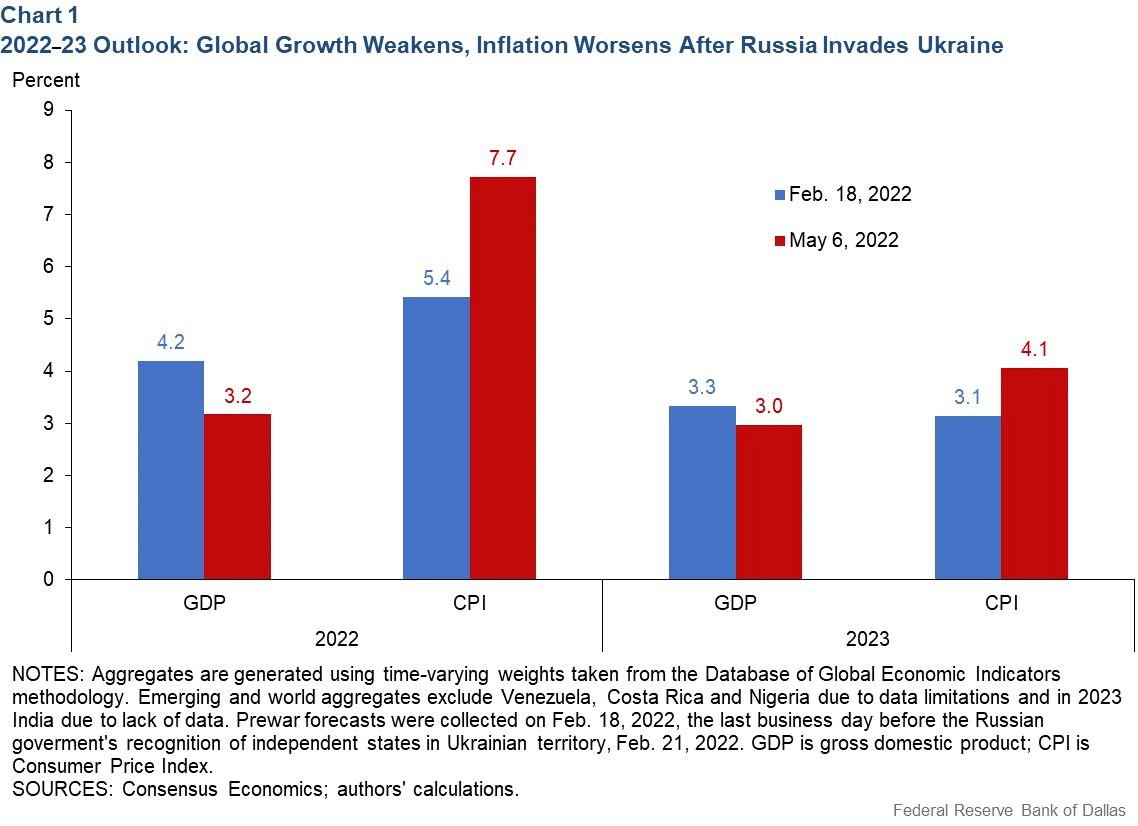

In 2022, the world faced a “accumulation of crises,” where exogenous factors collided to create a perfect storm of supply chain disruptions and price surges. The aftermath of the Covid-19 pandemic intersected with the outbreak of the war in Ukraine, leading to severe shortages in energy and cereal sectors. This period marked a definitive end to the era of relative price stability that had characterized the global economy since the 1980s, forcing central banks to pivot aggressively to combat rising costs.

The scale of this disruption was profound. In advanced economies, inflation reached levels not seen in decades, with price increases exceeding 7% in 2022, a stark contrast to the 1.2% average seen between 2014 and 2020 according to Encyclopædia Universalis. This shift was not merely a temporary glitch but a systemic shock that challenged the long-held assumption that globalization would keep prices permanently low.

The 2022 Convergence: Supply Shocks and Demand Excess

To analyze today’s economic environment, one must first dissect the specific mechanics of the 2022 crisis. The global economy suffered from a simultaneous “supply shock” and an “excess of demand.” The supply shock was driven largely by the war in Ukraine and the subsequent sanctions imposed on Russia, which crippled the flow of essential commodities. This led to a dramatic spike in raw materials; for instance, the average price of crude oil rose by 50%, climbing from 60 to 90 dollars per barrel in 2022 as detailed by Encyclopædia Universalis.

Agricultural markets faced similar volatility. The price of soft wheat surged from 200 to 300 euros per tonne during the same period. These increases were not isolated incidents but were amplified by the “cost of living crisis,” which left millions of households struggling to afford basic necessities. The OECD reported that this period represented the most significant shock to the energy market since the 1970s.

Whereas supply constraints pushed prices up, the “excess of demand” was a lingering effect of the pandemic recovery. Pent-up consumer spending, combined with previous fiscal stimulus packages, created a demand surge that the crippled global supply chain could not meet. This combination fueled “galloping inflation,” a term used by the OECD to describe the rapid and uncontrolled rise in prices that forced a global reconsideration of monetary policy.

Divergent National Trajectories in a Volatile Market

The impact of these crises was not uniform across the globe. Different regions adopted varying strategies to manage the fallout, leading to a fragmented economic recovery. In the United States, the focus shifted toward aggressive policy turns to curb inflation, while Europe experienced “atypical performances” and a temporary macroeconomic respite despite its heavy reliance on external energy sources according to Encyclopædia Universalis.

In Asia, the narratives were equally varied:

- China: The economy faced a notable slowdown in growth, complicating its role as a global manufacturing hub.

- India: While reporting growth, some analysts characterized this expansion as a “mirage,” questioning the underlying sustainability of the numbers.

- Japan: Maintained a “singular trajectory,” continuing to diverge from the monetary trends seen in other G7 nations.

Meanwhile, emerging markets in the “Global South” faced the most severe consequences. These nations dealt with a “cumul of extreme crises,” where the combination of high food prices, rising debt costs, and climate-related disasters created a precarious environment for economic stability as noted by Encyclopædia Universalis. Brazil, for example, saw a paradoxical mix of economic improvement alongside significant environmental disasters.

The Role of Monetary and Fiscal Calibration

As the world moved beyond the immediate shock of 2022, the focus shifted to the “calibration” of policy. The International Monetary Fund (IMF) emphasized that the future of the global economy depends heavily on how well monetary and fiscal policies are tuned to bring inflation down without triggering a deep recession. The IMF’s October 2022 outlook warned that the slowdown in global economic activity was more widespread and marked than previously expected.

The challenge for central banks has been a delicate balancing act. Raising interest rates too aggressively could stifle growth and increase the burden of debt for developing nations, while moving too slowly could allow inflation to become embedded in the economy. This tension is particularly acute in the context of the war in Ukraine, which continues to act as a volatile variable in global energy and food security.

Key Economic Indicators (2020-2022)

| Indicator | Pre-Crisis/Baseline | 2022 Peak/Impact | Primary Driver |

|---|---|---|---|

| Advanced Economy Inflation | 1.2% (2014-2020) | Over 7% | Supply shocks & demand excess |

| Crude Oil Price (Avg) | $60 per barrel | $90 per barrel | War in Ukraine / Sanctions |

| Soft Wheat Price | 200 euros/tonne | 300 euros/tonne | Agricultural disruptions |

| Global Growth Trend | Steady/Recovering | Widespread Slowdown | Exogenous shocks |

What Happens Next: The Path to Stabilization

The current economic context is viewed as distinct from the 2022 period because the immediate “shock” phase has evolved into a management phase. However, the “recul de la mondialisation”—the retreat of globalization—remains a persistent underlying trend. The shift toward “friend-shoring” or “near-shoring” suggests that the era of ultra-cheap imports, which helped maintain low inflation for forty years, may be permanently over.

For global investors, the focus now rests on the “good calibration” of policies. The ability of governments to maintain fiscal discipline while supporting vulnerable populations will determine whether the global economy achieves a “soft landing” or enters a period of prolonged stagnation. The interplay between geopolitical tensions and economic policy continues to be the primary driver of market volatility.

The next critical checkpoint for global markets will be the upcoming releases of updated World Economic Outlook reports and OECD economic forecasts, which will provide the data necessary to determine if inflation has truly stabilized or if new exogenous shocks are emerging. We encourage our readers to share their perspectives on how these global shifts are affecting their local businesses in the comments below.

Related reading