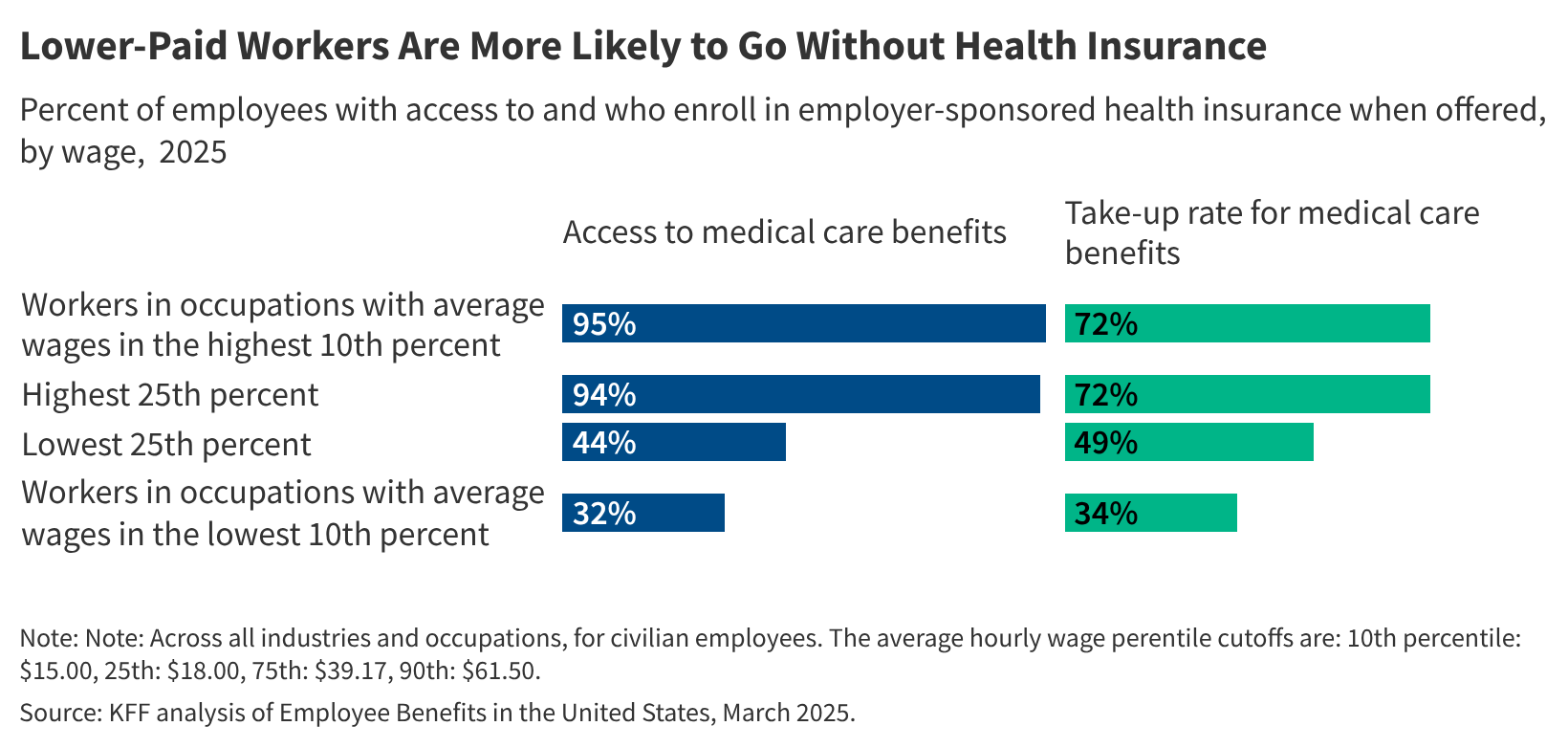

For millions of workers earning lower wages across the United States, access to affordable health insurance remains a critical yet often elusive component of economic security. While employer-sponsored coverage is the primary source of health insurance for most Americans, significant gaps persist for those in hourly, part-time, or service-sector jobs. Recent data from the Kaiser Family Foundation shows that in 2023, only 47% of workers in the lowest wage quartile (<$15/hour) were offered health benefits by their employers, compared to 89% in the highest wage bracket.

This disparity has real-world consequences: uninsured or underinsured low-wage workers are more likely to delay care, face medical debt, and experience poorer health outcomes. Yet a growing number of employers—particularly in industries like retail, hospitality, and healthcare—are implementing innovative strategies to expand coverage access for their lowest-paid staff. These efforts range from premium subsidies and tiered contribution models to partnerships with Medicaid and state-based marketplaces.

Understanding how and why some companies are closing this gap offers valuable insight into the evolving role of employers in the U.S. Healthcare system. As policymakers debate national reforms, workplace-based solutions are emerging as a practical avenue for improving equity in health access—especially for the 41 million Americans who earn less than $15 an hour and often lack alternatives to job-based coverage.

One of the most effective tools employers use to support lower-waged workers is premium cost-sharing. According to a 2023 survey by the International Foundation of Employee Benefit Plans, 68% of large U.S. Employers now offer premium assistance programs specifically designed for hourly or seasonal employees, up from 52% in 2020. These programs typically cover a percentage of the employee’s monthly premium based on income level or job classification.

For example, Amazon’s Career Choice program includes healthcare benefits for eligible part-time associates after 90 days of employment, with the company covering 95% of tuition and fees for in-demand fields—including healthcare certifications that often lead to roles with better benefits. While not direct health insurance, such upskilling initiatives indirectly improve access to higher-wage positions that include coverage.

Similarly, Starbucks provides health benefits to both full- and part-time employees who work at least 20 hours per week—a threshold significantly lower than the industry norm. The company reports that over 90% of its U.S. Workforce is eligible for coverage, including baristas and shift supervisors. This policy, maintained since 2002, has been cited as a model for inclusive benefits design in low-wage sectors.

Another approach gaining traction is the use of health reimbursement arrangements (HRAs), particularly Individual Coverage HRAs (ICHRAs), which allow employers to reimburse employees for individual market premiums and qualified medical expenses. Under the 2020 federal rule expanding ICHRA availability, companies of any size can offer this alternative to traditional group plans. A 2024 analysis by the Employee Benefit Research Institute found that 29% of employers with fewer than 50 workers now use ICHRAs, many citing flexibility in supporting diverse workforces, including lower-wage and hourly staff.

ICHRAs can be especially beneficial for employees in states with robust Medicaid expansion or active state marketplaces, where premium tax credits may further reduce out-of-pocket costs. For instance, a hospital system in Ohio implemented an ICHRA for its dietary and environmental services staff, allowing workers to select plans via Healthcare.gov while receiving monthly reimbursements averaging $300—effectively eliminating premium costs for many.

Employers are also leveraging public programs to bridge gaps. In states that have expanded Medicaid under the Affordable Care Act, some companies actively assist eligible employees in enrolling. A 2023 study published in Health Affairs found that firms in expansion states were 18% more likely to provide Medicaid enrollment assistance than those in non-expansion states, particularly in industries with high proportions of low-wage workers.

Walmart, the nation’s largest private employer, has partnered with state agencies to help associates access Medicaid or subsidized marketplace plans when employer coverage is unaffordable or inaccessible due to eligibility rules. While the company offers health plans to full- and part-time employees working 30+ hours weekly, it also provides resources to help those who fall short of hours thresholds navigate public options.

Beyond financial support, employers are addressing administrative barriers that deter enrollment. Complex paperwork, confusing terminology, and lack of language access can prevent eligible workers from signing up—even when coverage is offered and affordable. To combat this, companies like CVS Health have introduced multilingual benefits navigators and simplified enrollment portals during open season, resulting in a 22% increase in participation among hourly staff in 2023, according to internal reports.

Technology is also playing a role. Mobile apps that allow employees to compare plans, estimate costs, and enroll via smartphone are being adopted by firms with large deskless workforces. For example, the restaurant chain Chipotle uses a benefits app that sends push notifications about enrollment deadlines and offers side-by-side plan comparisons in English and Spanish—tools particularly useful for workers with limited access to desktop computers during shifts.

Despite these advances, challenges remain. Affordability continues to be the primary obstacle: even with employer contributions, out-of-pocket costs like deductibles and copays can deter utilization. A 2023 Commonwealth Fund survey found that 40% of insured low-wage workers skipped needed care due to cost, compared to 22% of higher-wage insured workers.

eligibility thresholds based on hours worked often exclude those with fluctuating schedules—a common feature of retail, food service, and gig-adjacent employment. Some employers are experimenting with “look-back” measurement methods or monthly eligibility determinations to capture workers whose hours vary week to week but average above the threshold over time.

Policy experts suggest that tying public incentives to equitable benefit design could accelerate progress. For example, expanding the Small Business Health Care Tax Credit to prioritize firms that offer coverage to part-time and low-wage employees might encourage broader adoption. Others advocate for state-level wage supplements or benefits boards that could help standardize access in sectors like home care and agriculture.

As the U.S. Healthcare landscape continues to evolve, the workplace remains a vital point of intervention for reducing disparities in health access. Employers who invest in inclusive, affordable coverage not only support worker well-being but also see returns in retention, productivity, and morale. A 2022 study by Harvard T.H. Chan School of Public Health found that companies offering comprehensive benefits to low-wage employees experienced 31% lower turnover than industry peers.

Looking ahead, the next major opportunity for progress lies in the implementation of proposed federal rules aimed at increasing transparency in health plan pricing and network adequacy—measures that could empower lower-wage workers to make more informed choices. The Department of Health and Human Services is expected to release final guidance on these provisions by late 2024, following a public comment period that closed in March.

For workers navigating their options, official resources such as Healthcare.gov, state Medicaid websites, and the Employer Assistance and Resource Network on Disability Inclusion (EARN) provide tools to assess eligibility and compare plans. Employers seeking guidance can consult the Society for Human Resource Management (SHRM) or the International Foundation of Employee Benefit Plans for best practices and compliance updates.

expanding health access for lower-waged workers is not just a matter of corporate responsibility—it is a public health imperative. When employers design benefits with equity in mind, they help build a healthier, more resilient workforce and contribute to a fairer system for all.

Stay informed about developments in workplace health policy and share your thoughts on how companies can better support equitable access to coverage. Join the conversation below.

Related reading

- Red Fruits: Health Benefits, Cancer Protection, and Heart Health for Summer

- How the Tailfer Plant Transforms River Water into Drinking Water

- RAP vs. IBR: What Your New Student Loan Bill Actually Costs (daybreakwire.com)

- New Study Links GLP-1 Medications Like Wegovy and Ozempic to Health Risks (archyde.com)