As spring unfolds across Europe, a quiet debate is stirring in French real estate circles: despite persistent economic headwinds, does the timeless adage “investir dans la pierre, c’est toujours un bon choix” still hold true? The phrase, which translates to “investing in stone is always a good choice,” has long been a cornerstone of French financial wisdom, reflecting a cultural preference for tangible assets over volatile markets. Now, amid shifting credit dynamics and cautious buyer sentiment, industry observers are re-examining whether this belief remains grounded in reality—or if it risks becoming a nostalgic mantra disconnected from current market mechanics.

The conversation gained renewed traction following reports that France’s residential mortgage market grew by just 0.8% in the first quarter of 2026—a figure that underscores the prevailing “friolité ambiante,” or ambient chill, among lenders and borrowers alike. This near-stagnation in credit expansion contrasts sharply with the robust activity seen in previous years and raises questions about affordability, access to financing, and the broader health of the property sector. While such data points to hesitation, they do not exist in isolation; they reflect a complex interplay of interest rate policies, inflation trends, and evolving consumer confidence that warrants closer inspection.

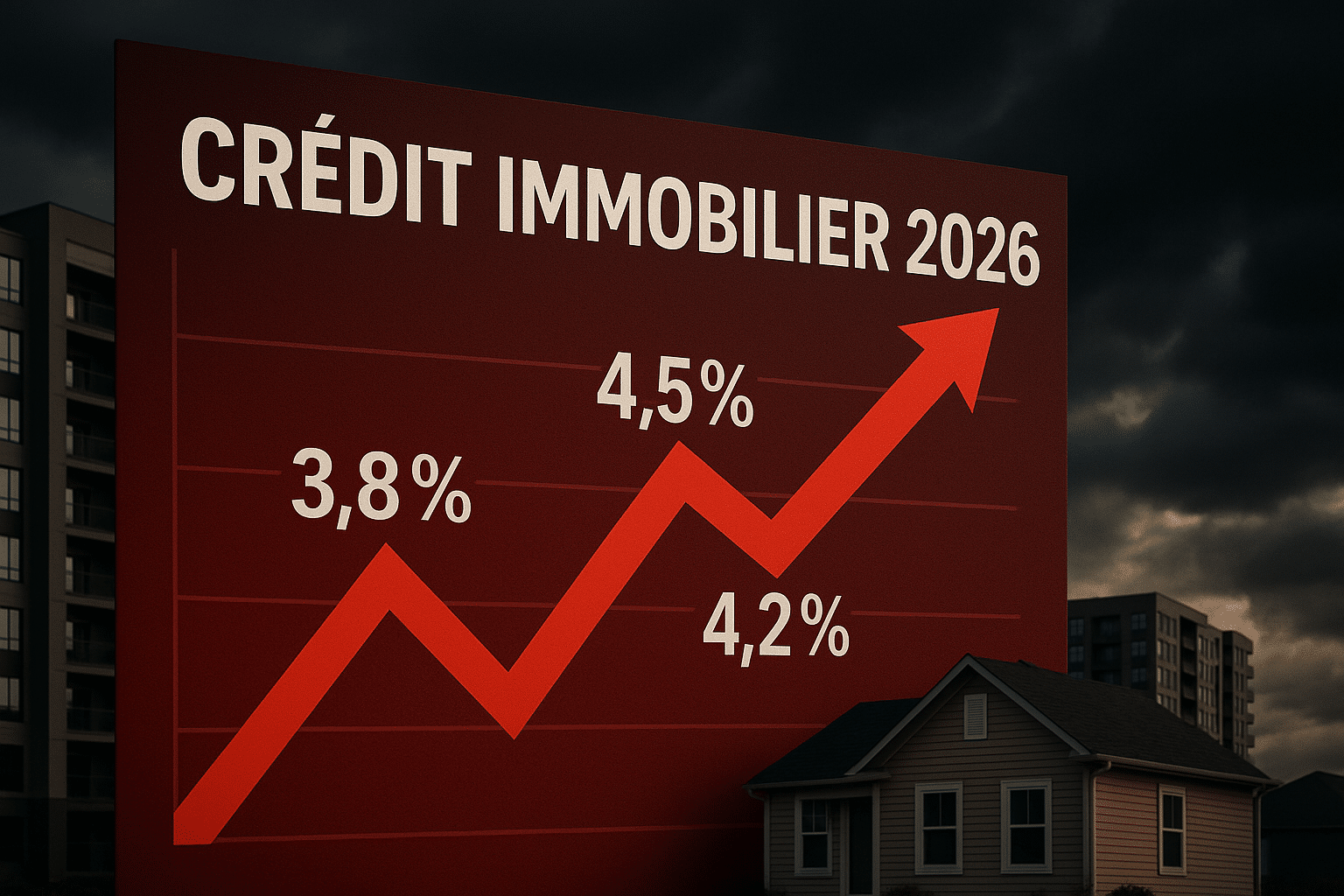

To understand the implications of this sluggish credit growth, it is essential to gaze beyond the headline number and examine the structural forces shaping France’s housing market. According to the Banque de France, the country’s central bank, the average interest rate on modern home loans stood at 3.45% in March 2026, up from 2.90% a year earlier—a rise driven by the European Central Bank’s ongoing efforts to curb inflation through monetary tightening. Whereas rates have stabilized somewhat in recent months, they remain significantly higher than the historic lows of 2021, when borrowing costs dipped below 1.5% for many borrowers. This shift has inevitably increased monthly repayment burdens, particularly for first-time buyers and those purchasing in high-demand urban zones like Paris, Lyon, and Bordeaux.

Yet, even as financing conditions tighten, demand for residential property has not collapsed. Data from the French Notaries’ Council (Conseil supérieur du notariat) shows that existing-home sales declined by only 2.1% year-over-year in Q1 2026, suggesting that while transactions have slowed, the market remains active. In certain regions, particularly rural areas and smaller towns, transaction volumes have held steady or even increased slightly, driven by remote work trends and a continued preference for larger living spaces post-pandemic. This divergence highlights an important nuance: national aggregates can mask significant regional variation, and opportunities may still exist where affordability and lifestyle factors align.

One voice frequently cited in these discussions is Michaël Thouly, a real estate professional who manages a Laforêt franchise office with six agents in central France. While the exact location of his agency was not specified in the original report, Thouly has been quoted in regional media emphasizing that periods of market hesitation often create strategic advantages for prepared buyers. “When credit tightens and prices stabilize,” he reportedly observed in a March 2026 interview with a local economic publication, “it’s not the time to retreat—it’s the time to evaluate, to compare, and to act with clarity.” His perspective reflects a broader sentiment among some industry veterans: that cyclical downturns, while challenging, can reset unrealistic expectations and lay the groundwork for more sustainable long-term growth.

This viewpoint is echoed in analyses by independent housing economists who argue that France’s property market benefits from deep-rooted structural strengths. Unlike some countries where speculative investment dominates, French homebuying is still largely driven by owner-occupancy—approximately 65% of primary residences are owned by their occupants, according to INSEE, the national statistics institute. This high rate of owner-occupation tends to reduce volatility, as households are less likely to sell quickly in response to short-term market fluctuations. France maintains a robust system of tenant protections and rent regulation in high-pressure zones, which helps prevent extreme price spirals while supporting rental market stability.

Another factor often overlooked in credit-centric analyses is the role of household savings. French households have historically maintained one of the highest savings rates in the eurozone, with liquid assets averaging over 15% of disposable income in recent years, per OECD data. This financial buffer enables many families to absorb higher down payments or withstand temporary income disruptions without being forced to sell. The slowdown in mortgage lending may reflect not a loss of confidence in real estate as an asset class, but a rational adjustment to higher borrowing costs—where buyers are simply taking more time to save, compare options, or opt for smaller loans.

Of course, challenges remain. Construction costs have risen due to persistent supply chain pressures and stricter environmental regulations, including the RE2020 standard, which mandates higher energy efficiency for new buildings. These factors have slowed the pace of new housing completions, particularly in urban centers where demand is strongest. According to the Ministry of Ecological Transition, housing starts fell by 4.3% in 2025 compared to the previous year, exacerbating existing shortages and contributing to upward pressure on rents and purchase prices in tight markets. For policymakers, balancing affordability with sustainability goals continues to be a complex challenge.

Despite these headwinds, the enduring appeal of real estate in France is rooted in more than just financial calculation. For many, property ownership represents security, legacy, and a tangible stake in one’s community—a sentiment that transcends quarterly credit fluctuations. As one Paris-based notaire explained in a recent interview, “People don’t buy apartments just for yield; they buy them to live in, to raise families in, to pass on. That changes the calculus.” This emotional and cultural dimension helps explain why, even during periods of economic uncertainty, the French residential market has repeatedly demonstrated resilience.

Looking ahead, market participants will be watching closely for signals from the European Central Bank, whose next policy meeting is scheduled for June 10, 2026. Any indication of a pause or reversal in rate hikes could quickly shift buyer sentiment and unlock pent-up demand. In the meantime, real estate professionals advise prospective buyers to focus on fundamentals: location, long-term affordability, energy performance, and resale potential—not short-term market timing. As Thouly’s Laforêt office continues to counsel clients through this transitional phase, their message remains consistent: patience and preparation, rather than panic, are the hallmarks of successful property investment in any climate.

For readers seeking to stay informed about evolving mortgage trends and housing policy in France, official updates are regularly published by the Banque de France and the French Ministry of Economy, and Finance. These sources provide transparent data on lending volumes, interest rate benchmarks, and regulatory developments that can help individuals make well-grounded decisions in an ever-changing market.

Keep reading