As we navigate the healthcare landscape in 2026, understanding the nuances of Medicare Advantage remains a critical priority for millions of beneficiaries. As a physician and journalist, I have seen firsthand how the complexity of insurance structures can impact patient access to care. Staying informed about the evolving nature of Medicare Advantage plans is not merely a matter of financial planning; it is a fundamental component of managing your long-term health and well-being.

For many, the appeal of Medicare Advantage—often referred to as Medicare Part C—lies in the bundling of hospital, medical, and often prescription drug coverage into a single plan. However, the 2026 coverage year brings specific considerations regarding premiums, out-of-pocket limits, and the administrative hurdles associated with prior authorization. Whether you are currently enrolled or considering a change, the official government portal remains the most reliable resource for comparing plans and identifying providers in your specific area.

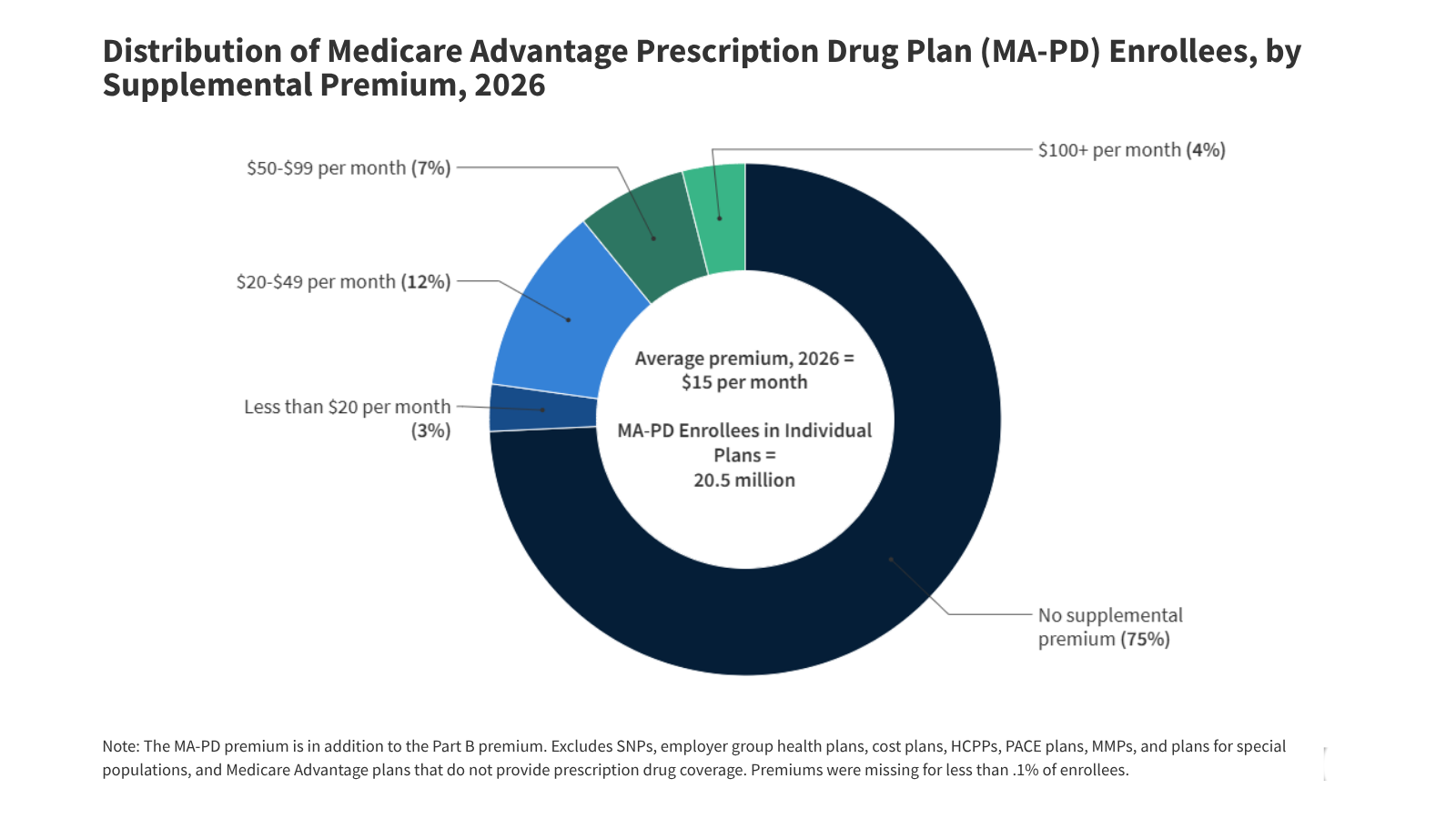

Navigating Costs and Coverage Changes in 2026

One of the most frequent questions I receive from patients concerns the financial trajectory of their coverage. Medicare Advantage premiums are dynamic, influenced by market competition and federal policy adjustments. For the 2026 benefit year, beneficiaries should be aware that while some plans may offer low or zero-premium options, the total cost of care is heavily dependent on out-of-pocket maximums.

Every Medicare Advantage plan is required to set an annual limit on out-of-pocket costs for covered medical services. Once a beneficiary reaches this threshold, the plan pays 100% of the costs for covered services for the remainder of the year. It is essential to review your specific plan’s Evidence of Coverage (EOC) document to understand these limits, as they can vary significantly between carriers and plan types. As noted by federal health authorities, protecting yourself from Medicare fraud is equally important; never share your Medicare Number with unverified callers or through unsolicited digital messages.

Understanding Prior Authorization and Supplemental Benefits

In recent years, the use of prior authorization—a process where your physician must obtain approval from the insurance plan before a specific service or medication is covered—has become a central point of discussion in public health policy. For the patient, this can mean delays in diagnostic testing or specialized treatments. If you are facing a delay, I always advise patients to work closely with their clinical team, as they are often the best advocates for navigating the appeals process.

Beyond standard medical care, many Medicare Advantage plans distinguish themselves through supplemental benefits. These may include coverage for dental, vision, hearing, or even fitness memberships. While these additions can provide significant value, they should never be the sole factor in choosing a plan. It is far more important to ensure that your preferred physicians and hospital systems are within the plan’s network, as out-of-network costs can be prohibitive.

Key Considerations for Beneficiaries

- Verify Network Status: Always confirm that your primary care physician and essential specialists are contracted with the plan.

- Review the Formulary: If you take prescription medications, check the plan’s drug list to ensure your specific prescriptions are covered at a manageable tier.

- Utilize Digital Tools: Use the official Medicare.gov plan finder to compare costs and benefits based on your specific medications and health needs.

- Guard Your Identity: Be wary of anyone asking for your Medicare card details via phone or social media; legitimate representatives will not use these channels to solicit personal information.

Taking Control of Your Health Data

In this digital age, patients have more tools than ever to manage their health information. Medicare now provides an app library that allows beneficiaries to find secure, third-party applications to track health history and manage medications. Integrating these tools can help you stay organized, especially when managing chronic conditions that require coordination between multiple specialists.

As we move through 2026, remember that the goal of these insurance programs is to support your health. Should you encounter issues with coverage denials or billing, the official Medicare resources provide clear pathways for reporting fraud or seeking assistance with appeals. Being proactive about your health insurance is one of the most effective ways to ensure that you receive the care you need, when you need it.

For those looking to stay updated on future changes, I encourage you to monitor the official Medicare alerts during the annual open enrollment periods. If you have questions or experiences regarding your 2026 plan, I invite you to share your thoughts in the comments section below. Your insights help us maintain a robust conversation about the realities of navigating modern healthcare.

Keep reading