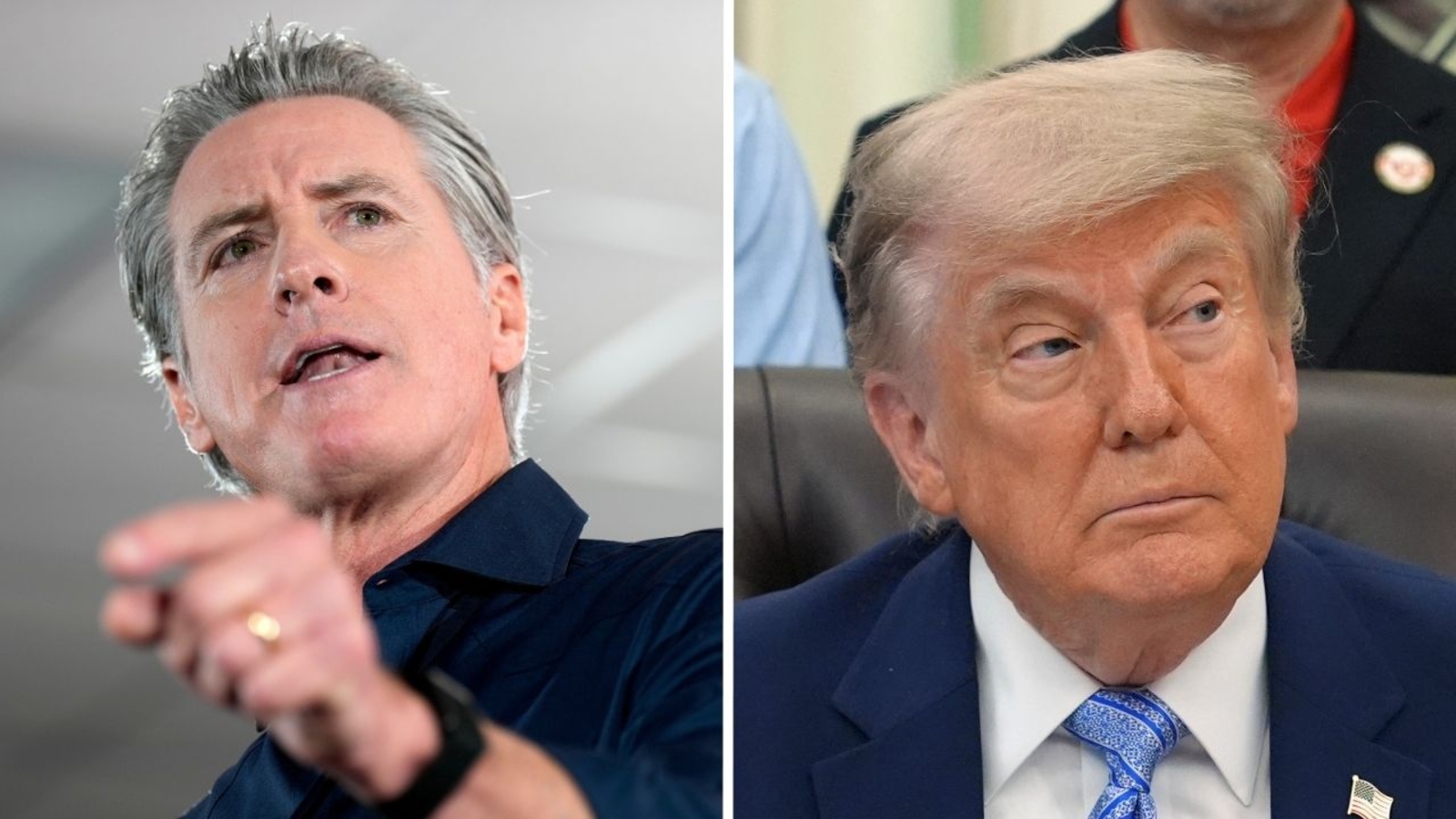

California Governor Gavin Newsom has announced a legislative strategy aimed at imposing a 100% tax on payments originating from a $1.8 billion fund established by supporters of President-elect Donald Trump. The proposed measure, which the Governor’s office has characterized as an effort to ensure accountability for political activities, targets the financial structure of what has been described in various filings as an effort to combat the perceived weaponization of the federal government. This move represents a significant escalation in the ongoing policy friction between the Democratic leadership in Sacramento and the incoming federal administration.

The core of this legislative proposal centers on the taxation of specific disbursements. According to statements from the Governor’s office, the state intends to utilize its fiscal authority to levy a 100% tax on any individual or entity within California that receives funds from this specific $1.8 billion initiative. This policy, if enacted, would effectively neutralize the financial utility of these payments for recipients residing in the state, creating a substantial hurdle for the fund’s operational reach within California’s jurisdiction. Detailed information regarding the Governor’s legislative priorities and state fiscal policies can be found through the Official Website of the Governor of California.

As the political landscape shifts toward the next presidential term, this development highlights the broader tension surrounding political fundraising and the use of private capital to influence federal oversight and institutional policy. The proposal is currently being framed by supporters as a necessary check on private influence, while critics have questioned the legal viability of a state-level tax targeted at specific political activities. The legal framework governing political action committees and non-profit fiscal structures is overseen by the Federal Election Commission, which maintains comprehensive records on campaign finance and organizational disclosures.

Understanding the Legislative Strategy

The proposal to tax the $1.8 billion fund—frequently referenced in media reports as an anti-weaponization initiative—is part of a broader push by the California administration to align state policy with its stance on federal accountability. By targeting the tax code, the Governor is attempting to exercise state sovereignty in a manner that directly impacts the efficacy of national political spending. Under the current California Revenue and Taxation Code, the state has broad authority to adjust tax brackets and introduce new levies, provided they meet constitutional muster. For those tracking the evolution of state tax laws, the California Franchise Tax Board provides ongoing updates on legislative mandates and tax compliance requirements.

The term “weaponization,” as used in the context of this fund, typically refers to the arguments made by organizers that federal agencies have been utilized for partisan political ends. By seeking to tax the disbursements of this fund, California officials are signaling a direct opposition to the movement’s stated goals. This legislative maneuver follows a series of public comments from Governor Newsom regarding the need for “Trump-proofing” state policies, a strategy aimed at insulating California’s environmental, immigration, and reproductive rights laws from potential federal changes. A summary of the state’s legislative session and policy tracking can be accessed via the California Legislative Information portal.

Legal and Constitutional Considerations

Legal experts have noted that any attempt to levy a 100% tax on specific financial transfers may face significant challenges in the federal courts. The U.S. Constitution, particularly the Supremacy Clause and the First Amendment, provides robust protections for political expression and spending. A tax that appears to target specific ideological groups or political movements could be viewed as a violation of equal protection or free speech rights. Historically, cases involving the taxation of political organizations have been litigated at the highest levels, including precedents set by the Supreme Court regarding the limits of state intervention in federal political activity, as documented by the Supreme Court of the United States.

the interplay between state and federal tax codes is complex. If the funds in question are classified under federal law as tax-exempt, the imposition of a state-level tax could trigger a preemption battle. The Internal Revenue Service (IRS) maintains strict guidelines regarding the tax-exempt status of various entities, and any conflict between state and federal classifications would likely require intervention by the federal judiciary. For those interested in the intricacies of tax-exempt status and political activity, the Internal Revenue Service provides detailed guidance on the limitations and requirements for 501(c) organizations.

The Path Forward: What Happens Next

As of this writing, the proposal remains in the early stages of the legislative process. For the measure to become law, it must be drafted into a formal bill, introduced in the California State Assembly or Senate, and successfully navigate the committee system before reaching the Governor’s desk for a signature. Observers expect that the introduction of such a bill would be met with immediate legal challenges from the organizations involved in the fund, potentially leading to a stay on implementation while the courts determine the constitutionality of the tax.

The next major checkpoint in this developing story will be the formal introduction of the legislative text, which will provide clarity on the scope of the tax, the definitions of the entities covered, and the mechanisms for enforcement. We will continue to monitor the legislative calendar and court filings as this situation evolves. We invite our readers to share their perspectives on the balance between state regulatory authority and federal political activity in the comments section below.