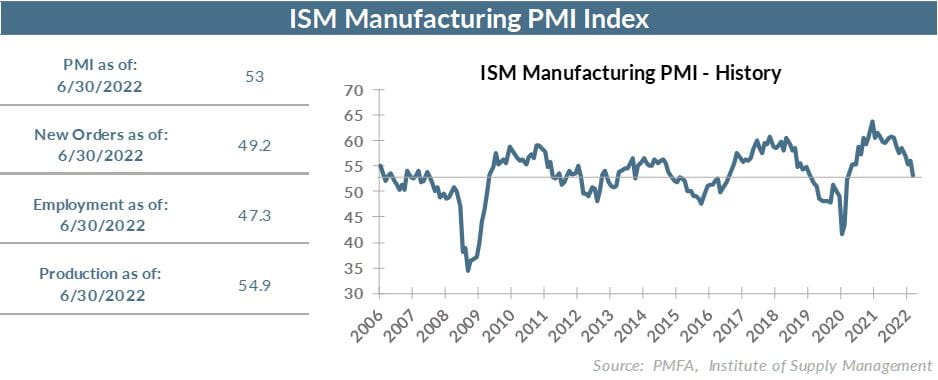

The United States manufacturing sector continued to expand in June, marking the sixth consecutive month that the Institute for Supply Management (ISM) Manufacturing Purchasing Managers’ Index (PMI) has remained above the 50-point threshold. While the index signals ongoing growth, recent data indicates a slight deceleration in activity, reflecting broader shifts in market demand and supply chain conditions.

According to the latest report from the Institute for Supply Management, the manufacturing PMI for June reached 53.3, a figure that highlights the complex nature of the current economic environment. This reading follows a period where analysts and market participants closely monitored the intersection of persistent inflationary pressures and cooling demand for new orders. The index, which remained above the 50-point mark, contrasts with some earlier expectations for sustained higher output, illustrating the volatility inherent in the current industrial landscape.

Understanding the Current Manufacturing Climate

The manufacturing sector serves as a vital barometer for the health of the U.S. economy, and the June data highlights a nuanced performance across various sub-indices. Economic monitors often look to the ISM report to gauge capital expenditure and inventory management strategies. In June, the decline in the overall index was largely attributed to a softening in new orders and a cautious approach toward production levels among manufacturers.

Despite the dip in the headline figure, the industry continues to grapple with input costs. The cost of raw materials remains a critical factor for producers. Businesses are currently navigating a environment where input prices are sustained at high levels, forcing many to evaluate their pricing power and profit margins as they head into the second half of the year.

Factors Influencing Industrial Performance

Economic indicators such as the PMI are influenced by a wide array of variables, including global trade dynamics, labor market conditions, and interest rate policies set by the Federal Reserve. The Federal Reserve maintains a close watch on these manufacturing reports, as they provide insight into inflationary trends. When manufacturing activity slows, it often suggests that companies are becoming more conservative with their hiring and investment plans in anticipation of a potential shift in consumer spending.

The decline in the June index represents a 0.7 percentage point drop from previous levels, a shift that caught the attention of market analysts tracking the recovery trajectory. This movement is not occurring in a vacuum; it follows a period of significant fluctuation in the global supply chain, where companies previously struggled to meet demand due to material shortages and labor constraints. Today, the challenge has shifted from availability to cost management and demand forecasting.

Comparative Analysis of Economic Benchmarks

It is important to note that different methodologies can lead to varying interpretations of the sector’s health. The ISM report, which focuses on a broad survey of supply executives, often shows different results compared to other private sector indices like the S&P Global Manufacturing PMI. While the ISM index remained above the 50-point expansion threshold in June, other reports have occasionally shown more resilient, albeit cooling, data.

Investors and policy makers often perform a comparative analysis between these indices to filter out statistical noise. Discrepancies between the ISM and other surveys often stem from the composition of the panels, which may include different weightings of large versus small enterprises. By examining these datasets in tandem, observers gain a more comprehensive view of whether the manufacturing sector is facing a temporary setback or a more sustained structural correction.

What Lies Ahead for the Manufacturing Sector

Looking toward the coming months, the focus remains on whether the manufacturing sector can regain its momentum. The next major update from the Institute for Supply Management is scheduled for the first business day of the following month, when the July data will be released. This report will be essential for determining if the June dip was an anomaly or the beginning of a cooling trend in industrial output.

Market participants are encouraged to monitor upcoming filings and official statements, which provide detailed reports on durable goods orders and industrial production. These documents offer the granular data necessary to understand the drivers behind the PMI figures. As the economic narrative evolves, the ability of firms to manage input costs while maintaining competitive pricing will likely define the sector’s performance through the remainder of the year. Please share your insights in the comments below as we continue to track these developments.