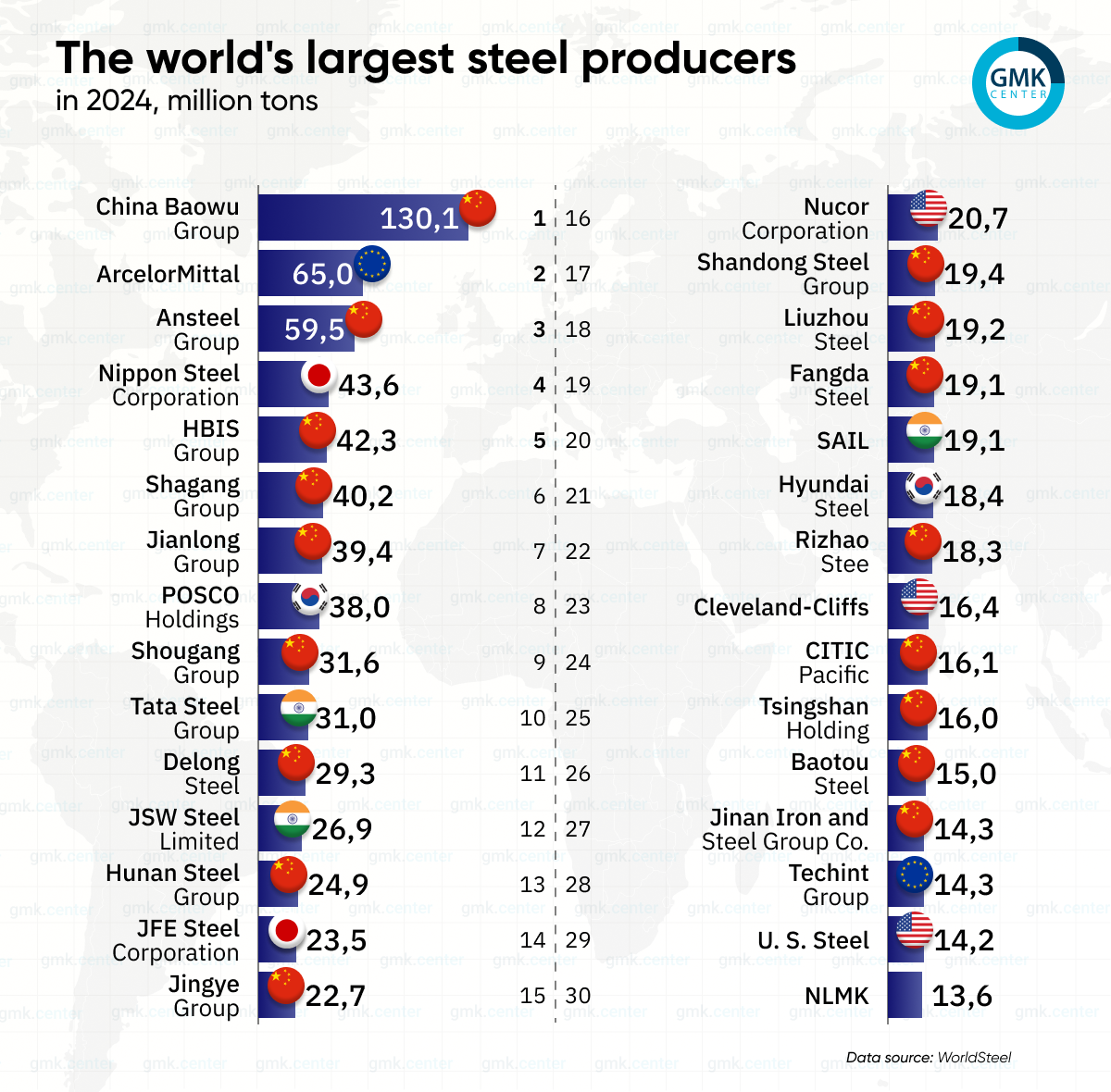

In the volatile world of global commodities, a “beat” is rarely just about the numbers; it is a signal of resilience. ArcelorMittal, the world’s second-largest steelmaker, has delivered first-quarter results that have caught the attention of analysts and investors alike, posting a financial performance that exceeded market expectations.

For those of us tracking the intersection of industrial output and macroeconomic policy, these figures are particularly telling. The company reported an EBITDA (earnings before interest, taxes, depreciation, and amortization) of $1.68 billion for the January-to-March period, edging past the $1.66 billion anticipated by financial analysts. While a difference of $20 million might seem marginal for a conglomerate of this scale, in the capital-intensive steel industry, such a variance often reflects critical efficiencies in operational management or a strategic pivot in regional pricing.

From my perspective as an economist, this performance underscores a pivotal moment for the steel sector. We are seeing a complex tug-of-war between softening demand in some traditional markets and a surprising robustness in others, particularly within North America. This quarterly snapshot provides more than just a balance sheet; it offers a glimpse into how the global industrial engine is humming—or sputtering—as we navigate a transition toward greener manufacturing processes.

The ability to outperform expectations in a climate of fluctuating raw material costs and geopolitical instability is a testament to the company’s current strategic positioning. As we dive deeper into the drivers behind these results, it becomes clear that the narrative is not just about the bottom line, but about where the growth is coming from and what it means for the future of global infrastructure.

Breaking Down the EBITDA Beat: Why the Numbers Matter

To understand the significance of the $1.68 billion EBITDA, one must first understand what EBITDA represents in the context of heavy industry. Unlike net income, which can be skewed by accounting decisions, tax jurisdictions, and the massive depreciation of blast furnaces and rolling mills, EBITDA provides a clearer picture of the company’s core operational profitability. When ArcelorMittal reports a result that exceeds analyst projections, it suggests that the company is extracting more value from its production chain than the market had priced in.

The beat to $1.68 billion, compared to the $1.66 billion forecast, indicates a tighter control over operational costs or a more favorable pricing environment than expected during the first three months of the year. According to the official regulatory news from ArcelorMittal, the company continues to navigate a landscape defined by price volatility and shifting demand patterns.

This financial resilience is critical because the steel industry is notoriously cyclical. Companies that can maintain margins during leaner periods are better positioned to invest in the next phase of industrial evolution. For ArcelorMittal, this “better than expected” result provides a necessary cushion for its ongoing capital expenditures, particularly as the company aggressively pursues its decarbonization goals.

The North American Engine

A significant portion of this quarterly success can be attributed to the company’s performance in North America. While European markets have struggled with higher energy costs and fluctuating demand, the North American segment has acted as a primary growth driver. This trend is often linked to sustained infrastructure spending and a regional push for domestic steel production to secure supply chains.

The strength in North America allows ArcelorMittal to offset headwinds in other geographies. When one region outperforms, it balances the portfolio, reducing the company’s vulnerability to any single national economy. This geographic diversification is a cornerstone of their current strategy, ensuring that a downturn in the Eurozone does not lead to a systemic collapse of quarterly earnings.

Steel Price Trends and Global Demand Dynamics

The heartbeat of any steelmaker is the price of the finished product relative to the cost of iron ore and coking coal. In the first quarter, the interplay between these variables played a decisive role in the results. The “beat” in EBITDA suggests that ArcelorMittal successfully managed its spreads—the difference between the cost of raw materials and the selling price of steel.

Global demand for steel is currently fragmented. In emerging markets, urbanization continues to drive volume, but in developed economies, the focus has shifted toward high-value, specialized steel for automotive and renewable energy projects. By focusing on higher-margin products, ArcelorMittal has been able to maintain profitability even when overall tonnage volumes remain stagnant.

the industry is grappling with the “China factor.” As the world’s largest producer and consumer of steel, any shift in Chinese domestic demand or export quotas sends ripples through global pricing. ArcelorMittal’s ability to exceed expectations suggests a successful navigation of these external pressures, utilizing a sophisticated hedging strategy and a flexible production schedule to avoid oversupply pitfalls.

The Transition to Green Steel: A Long-Term Financial Gamble

While the quarterly numbers are positive, the overarching story for ArcelorMittal is the transition to “Green Steel.” The company is investing billions into replacing traditional blast furnaces—which rely heavily on coal—with Direct Reduced Iron (DRI) plants and Electric Arc Furnaces (EAF) powered by renewable energy. This is not merely an environmental initiative; it is a financial necessity to avoid future carbon taxes and meet the growing demand for low-carbon materials from corporate clients.

The capital expenditure required for this transition is immense. This is why the Q1 EBITDA beat is so vital. Every extra million in operational profit can be diverted toward these long-term assets. The shift to green steel represents a fundamental change in the company’s cost structure. While the initial investment is high, the long-term goal is to decouple steel production from volatile fossil fuel prices, creating a more stable and predictable earnings profile.

Industry observers are closely watching how this transition affects the balance sheet. The challenge for ArcelorMittal is to maintain the current profitability—as seen in the first-quarter results—while simultaneously funding a complete overhaul of its industrial base. It is a high-stakes balancing act that requires precise financial discipline.

Stakeholder Impact: Who Wins?

The positive surprise in the first-quarter results has immediate implications for several key stakeholders:

- Shareholders: The beat often leads to increased investor confidence and potential upward revisions of stock price targets. When a company consistently outperforms analyst expectations, it signals a management team that is underpromising and overdelivering.

- Industrial Clients: For automotive manufacturers and construction firms, a stable and profitable ArcelorMittal means a more reliable supply chain. A company in financial distress is more likely to cut corners or experience production disruptions.

- Employees: Strong financial results provide a level of job security and the potential for continued investment in plant modernization, which often improves working conditions and safety.

- Environmental Regulators: Profitability gives the company the “green light” to accelerate its decarbonization projects, helping governments meet their national emissions targets.

What Happens Next?

The market now looks toward the second quarter to see if this momentum is sustainable. The key variables to watch will be the stability of North American demand and the evolution of energy prices in Europe. If ArcelorMittal can replicate this performance in Q2, it will confirm that the Q1 beat was not an anomaly but a trend of operational improvement.

Investors should maintain a close eye on the company’s next official quarterly filing and earnings call, where management will likely provide updated guidance on their capital expenditure for the remainder of the year. Specifically, any updates on the timeline for new DRI plant commissions will be a critical indicator of their long-term competitiveness.

| Metric | Analyst Expectation | Actual Reported | Variance |

|---|---|---|---|

| EBITDA | $1.66 Billion | $1.68 Billion | +$20 Million |

| Primary Driver | General Market Recovery | North American Strength | Positive Shift |

| Outlook | Neutral/Cautious | Resilient/Optimistic | Improved |

The next confirmed checkpoint for the company will be the release of its second-quarter results, typically published in mid-July. This report will reveal whether the company has successfully navigated the seasonal shifts in construction demand and if the North American engine continues to fire on all cylinders.

Do you believe the shift toward green steel will permanently alter the profitability of the global steel industry, or are the costs too high to sustain? Share your thoughts in the comments below or join the conversation on our social platforms.