As global markets experience heightened volatility and shifting interest rate environments, retail banking institutions are increasingly re-evaluating the structures of their wealth management and savings products. Among the most significant shifts is the evolution of Equity Linked Deposits (ELDs), a financial instrument that has long served as a bridge for conservative investors looking to gain exposure to equity market performance while maintaining the principal protection typical of a traditional savings account.

In recent months, the landscape for these products has undergone a notable transformation. Financial institutions are increasingly moving away from traditional “knock-out” clauses in their ELD offerings. This shift is a direct response to the complexities faced by investors in a rapidly appreciating stock market, where hitting a predetermined ceiling can inadvertently nullify potential gains, leaving the depositor with only the base interest rate—or in some cases, a diminished return profile—at the end of the term.

Understanding the Mechanics of Equity Linked Deposits

An Equity Linked Deposit is a hybrid financial product that combines the security of a fixed-term deposit with the performance potential of a stock market index, such as the KOSPI 200 in South Korea or similar benchmarks globally. The core appeal of the ELD lies in its “principal protection” feature; regardless of how the underlying index performs, the investor’s initial capital is generally guaranteed by the issuing bank, provided the deposit is held to maturity.

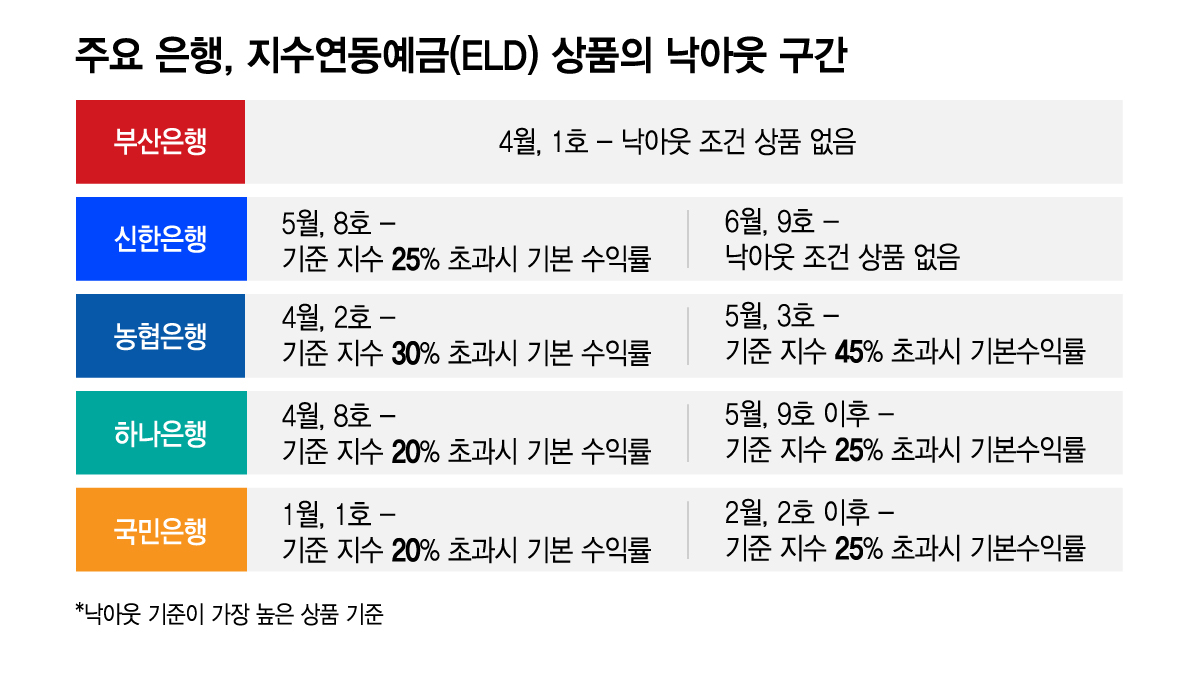

Traditionally, many of these products included a “knock-out” condition. This feature acts as a performance cap: if the underlying index rises above a specific threshold during the life of the deposit, the contract is essentially terminated or “knocked out.” The investor is then often locked into a predetermined, lower interest rate, regardless of how much further the market climbs. While this protects the bank against extreme market volatility, it has become a point of friction for investors in sustained bull markets, where the potential for significant upside is curtailed by the very design of the product.

Shifting Strategy: The Rise of Knock-Out Free Structures

The recent trend toward removing these barriers reflects a broader effort by financial institutions to align product offerings with the expectations of modern retail investors. By offering ELDs without knock-out conditions, banks are effectively allowing clients to capture a larger share of market growth without the risk of their participation being prematurely terminated.

This strategic pivot is particularly relevant as institutional and retail investors alike grapple with the challenges of inflationary pressure and the search for yield. For the banking sector, the introduction of these more flexible instruments serves a dual purpose: it maintains customer loyalty by offering a more competitive product, and it adapts to a market environment that is increasingly characterized by rapid, high-velocity movements in equity indices. As noted by financial regulators, transparency in product structure is critical to maintaining market integrity and ensuring that retail investors fully comprehend the risk-reward balance of their portfolios (Financial Services Commission of South Korea).

What This Means for the Retail Investor

For individuals considering these products, the removal of knock-out clauses represents a shift toward more favorable terms, though it is essential to conduct thorough due diligence. While the elimination of the cap allows for greater upside potential, investors should remain cognizant of how these products are priced. Banks typically fund the principal protection of an ELD through the purchase of zero-coupon bonds and the remaining capital is invested in derivatives to provide equity exposure.

When considering an ELD, investors should prioritize the following factors:

- Participation Rates: Understand the percentage of the index’s growth that the deposit will capture.

- Principal Protection Levels: Confirm the exact percentage of capital guaranteed at maturity.

- Term Duration: Evaluate whether the lock-in period aligns with your broader liquidity needs.

- Underlying Index Volatility: Assess the historical performance and volatility of the specific index tied to the deposit.

As the financial sector continues to innovate, the “new look” for ELDs is likely to focus on further customization. Whether through tiered interest structures or more granular control over the underlying assets, the goal for banks is to provide stability in an increasingly unpredictable economic climate. Investors are encouraged to monitor disclosures from their respective financial institutions and consult with certified financial planners to ensure that these products align with their long-term wealth management objectives.

The next major update regarding financial product transparency and retail investor protection standards is expected in the upcoming quarterly regulatory review. As always, I welcome your thoughts on how these shifts in banking products are impacting your own investment strategy—please feel free to share your perspectives in the comments section below.

- Melimelo veut ranger les courses, les rendez-vous et la charge mentale dans une seule application – Les Numériques

- Duchas portátiles y de emergencia: dignificar la higiene tras el terremoto – El Estímulo

- China’s AI Surge: Market Growth, Tech Distillation, and US Tension (archynewsy.com)

- Low Credit Limits: Why Banks Fail to Provide Explanations (world-today-news.com)