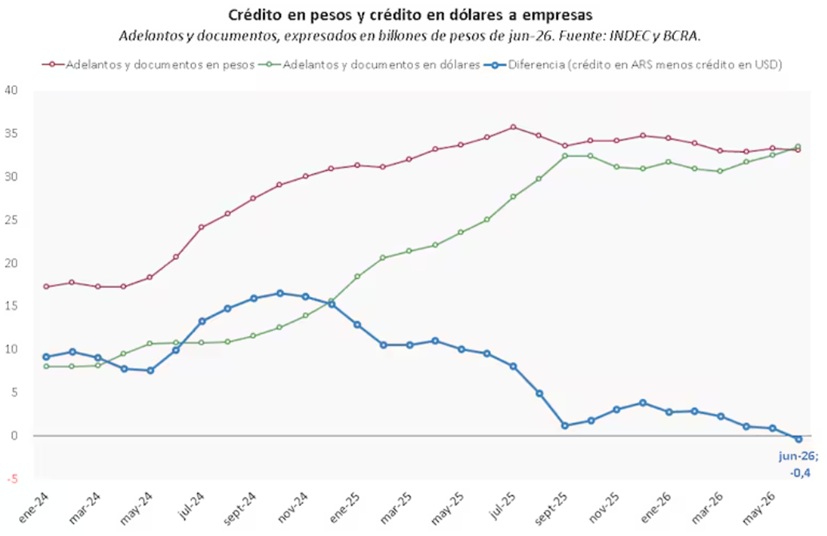

Corporate loans in US dollars have surpassed peso-denominated credit for Argentine businesses, marking a significant shift in how local firms manage liquidity and debt in a volatile economy. According to recent financial data, this transition is driven by companies seeking to hedge against rapid currency devaluation and persistent high inflation. This trend creates a stark divide in the private sector, benefiting export-oriented industries while increasing the financial vulnerability of domestic-focused companies that must service dollar debt using devaluing pesos.

The crossover point, where dollar-denominated corporate credit outweighed peso-based lending, reflects a strategic response to the macroeconomic instability in Argentina. As the local currency, the peso, continues to face downward pressure, businesses are increasingly opting for dollar-linked obligations to align their debt structures with their revenue streams or to protect their capital from the eroding effects of inflation.

Financial analysts monitoring the Central Bank of Argentina (BCRA) suggest that this shift is not merely a preference for a stable currency but a survival mechanism. For many large-scale enterprises, the cost of borrowing in pesos—often tied to high nominal interest rates intended to curb inflation—has become less predictable than the risks associated with managing dollar-denominated debt.

Why are Argentine companies shifting to dollar-denominated debt?

The primary driver behind the surge in dollar-denominated credit is the persistent mismatch between local currency earnings and the rising costs of domestic operations. In an environment where inflation frequently reaches triple digits, the real value of peso-denominated debt can fluctuate wildly. Companies that hold significant assets or revenue in dollars find it more efficient to match their liabilities to those same assets, a practice known as natural hedging.

Furthermore, the volatility of the Argentine peso makes long-term planning in local currency nearly impossible for large corporations. By securing credit in US dollars, firms can stabilize their long-term financial projections, provided their income is also linked to the dollar. This is particularly common in sectors that participate in international trade. For these entities, the risk of a sudden devaluation is mitigated because their revenue increases in peso terms as the dollar strengthens, helping to offset the increased cost of the debt service.

Interest rate spreads also play a critical role. While the Central Bank of Argentina has implemented various monetary policies to manage liquidity, the nominal rates for peso loans often fail to account for the rapid pace of devaluation. When the cost of borrowing in pesos becomes prohibitively high or too volatile, the relative attractiveness of dollar credit increases, especially for firms with access to international capital markets or specialized foreign exchange instruments.

Which sectors are emerging as the “winners” in this credit transition?

The “winners” in this new credit landscape are primarily those in the export-heavy sectors, where revenue is generated in foreign currency. The agribusiness sector remains a dominant player in this category. Large-scale grain and meat exporters operate almost entirely within a dollar-based economic framework. For these companies, taking on dollar debt is a logical extension of their business model, as it prevents the “currency mismatch” that often leads to insolvency during devaluations.

The energy sector, particularly companies involved in the development of the Vaca Muerta shale formation, also benefits from this shift. As Argentina seeks to increase its energy exports to generate much-needed foreign exchange reserves, the companies operating in this space are increasingly integrated into global financial flows. Their ability to earn US dollars makes dollar-denominated loans a stable and predictable component of their capital structure.

Technology and service firms that export intellectual property or software development services to international clients are also finding advantages. These “knowledge exporters” often maintain much of their cash flow in foreign currencies, allowing them to navigate the local inflationary environment with greater resilience than their domestic counterparts. For these firms, the shift to dollar credit is a way to institutionalize their existing financial reality.

How does the shift pose risks to domestic-focused businesses?

While exporters find stability in dollar debt, domestic-focused companies face what economists call “balance sheet risk.” Retailers, construction firms, and local service providers typically earn their revenue in pesos. When these businesses take on dollar-denominated loans, they create a direct exposure to exchange rate volatility. If the peso devalues sharply, the amount of local currency required to service the same amount of dollar debt increases proportionally, often leading to a liquidity crisis.

The construction and real estate sectors are particularly sensitive to this trend. These industries rely heavily on local demand and peso-based financing. A sudden spike in the cost of dollar debt can halt ongoing projects and reduce the ability of firms to invest in new developments. This creates a cycle of contraction where the rising cost of debt limits the very activity required to generate the cash flow needed to pay it back.

Small and medium-sized enterprises (SMEs) are also at a disadvantage. Unlike large exporters, SMEs often lack the sophisticated treasury departments required to manage complex currency hedges. For a local manufacturer or a regional distributor, a sudden shift in the exchange rate can turn a profitable quarter into a significant loss overnight. This vulnerability can lead to increased defaults and a more fragile domestic credit market.

What role does the Central Bank of Argentina play in this trend?

The Central Bank of Argentina (BCRA) maintains a complex relationship with this shift in credit dynamics. The bank’s primary mandate—to maintain price stability and manage the exchange rate—is directly challenged by the private sector’s move toward dollarization of debt. As more credit moves into dollars, the demand for foreign exchange can increase, putting further pressure on the bank’s reserves.

Monetary policy decisions, such as the adjustment of interest rates and the management of the “crawling peg” (the gradual devaluation of the peso), directly influence the decision of whether to borrow in pesos or dollars. If the BCRA maintains a policy that keeps the peso relatively stable, the incentive for dollar debt diminishes. However, if the bank allows for significant devaluations to align with market realities, the move toward dollar-denominated credit accelerates.

Regulators are also tasked with monitoring the systemic risk posed by this growing dollar-denominated debt. If a large portion of the corporate sector becomes heavily leveraged in dollars, a single major devaluation event could trigger a wave of corporate insolvencies. This would not only impact the banking sector but could also lead to broader economic instability, affecting employment and national tax revenues.

The following table compares the fundamental characteristics of peso-denominated vs. dollar-denominated corporate credit in the current Argentine context:

| Feature | Peso-Denominated Credit | Dollar-Denominated Credit |

|---|---|---|

| Primary Risk | High inflation and interest rate volatility. | Exchange rate devaluation and currency mismatch. |

| Typical Borrower | Domestic service and retail sectors. | Exporters (Agro, Energy, Tech). |

| Revenue Alignment | High alignment for local-market firms. | High alignment for export-oriented firms. |

| Impact of Devaluation | Reduces the real value of the debt. | Increases the real cost of debt service. |

As the Argentine economy continues to adjust to new fiscal and monetary frameworks, the balance between peso and dollar credit remains a critical indicator of corporate health and macroeconomic stability. Market participants are closely watching for updates from the Central Bank regarding liquidity provisions and potential changes to interest rate corridors.

The next major checkpoint for this trend will be the release of the next monthly report on private credit from the Central Bank of Argentina, which will provide updated figures on the exact ratio of peso to dollar debt held by the private sector.

What are your thoughts on the impact of currency-denominated debt on local business stability? Share your views in the comments below and share this article with your network.

Worth a look