Employer-sponsored health insurance remains the dominant form of coverage for working-age adults in the United States, with recent data showing it covered approximately 165.6 million people under age 65 as of March 2025. This figure, derived from the U.S. Census Bureau’s Annual Social and Economic Supplement of the Current Population Survey, underscores the system’s central role in the American healthcare landscape despite ongoing debates about affordability, access, and equity.

While employer-based plans continue to serve as a primary safety net for millions, recent trends reveal a shifting dynamic. Rising premiums, evolving workforce patterns, and policy changes are reshaping how and whether employers offer coverage, particularly for part-time, gig, and low-wage workers. Understanding these shifts is critical for employees navigating their options, policymakers assessing reform needs, and employers balancing cost containment with talent retention.

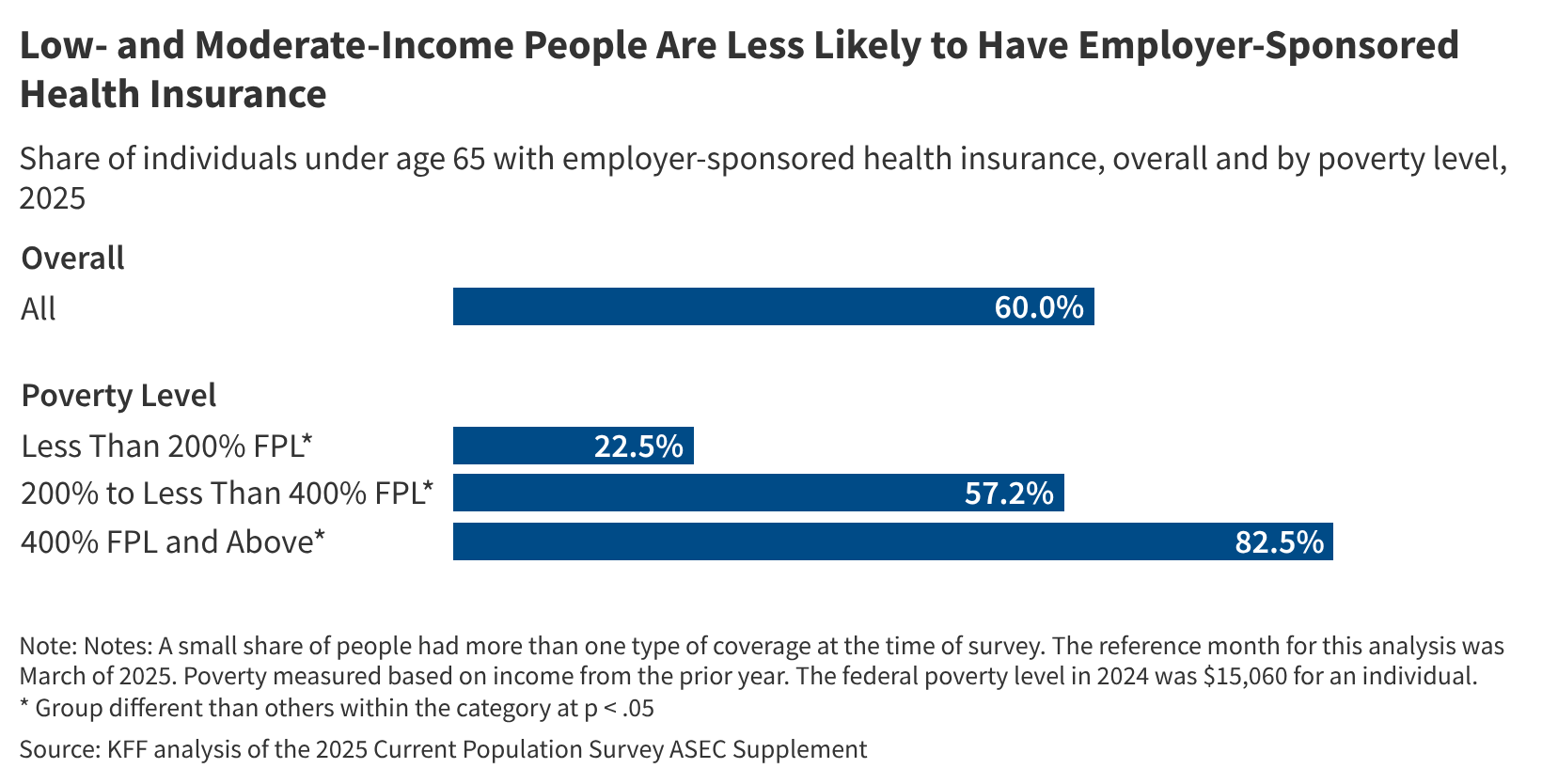

The persistence of employer-sponsored insurance reflects both historical precedent and structural incentives. Since World War II, when wage controls led companies to offer health benefits as a tool for attracting workers, the model has become deeply embedded in the U.S. System. Today, it covers more than half of the non-elderly population, far surpassing Medicaid, individual market plans, and other sources. However, its reach is not uniform, and gaps persist along lines of industry, occupation, and income.

According to the Kaiser Family Foundation’s 2024 Employer Health Benefits Survey, the average annual premium for employer-sponsored family coverage reached $25,572 in 2024, with workers contributing an average of $6,296 toward that cost. For single coverage, the average premium was $9,224, with employees paying $1,401 on average. These figures represent a 6% increase from the previous year, continuing a decade-long trend of outpacing wage growth and inflation. Kaiser Family Foundation

Despite rising costs, the offer rate of employer-sponsored coverage has remained relatively stable. In 2024, 57% of all firms offered health benefits to at least some employees, a figure that has fluctuated narrowly between 55% and 60% since 2010. However, offer rates vary dramatically by firm size: while 98% of firms with 200 or more workers provide coverage, only about 49% of modest firms (3–199 employees) do so. This disparity leaves many workers in smaller businesses without access to employer-based plans, pushing them toward marketplace coverage, Medicaid, or going uninsured.

Eligibility and take-up rates also reveal important nuances. Among workers employed at firms that offer coverage, about 79% are eligible for benefits, typically based on hours worked (often 30 or more per week) and waiting periods. Of those eligible, approximately 84% elect to enroll, meaning that roughly two-thirds of all workers at offering firms ultimately receive coverage through their employer. The remaining 16% may decline due to cost, access to alternative coverage (such as through a spouse’s plan), or eligibility for public programs like Medicaid.

One of the most notable recent developments is the growing use of tiered networks and high-deductible health plans (HDHPs) paired with health savings accounts (HSAs). In 2024, 31% of covered workers were enrolled in an HDHP/HSA option, up from just 4% in 2009. These plans feature lower premiums but higher out-of-pocket thresholds before coverage begins, shifting more financial responsibility onto employees. While they can encourage cost-conscious care, critics argue they may deter necessary treatment, particularly for low-income households.

Another emerging trend is the expansion of mental health and wellness benefits within employer plans. Driven by increased awareness of workplace stress and burnout, especially following the COVID-19 pandemic, more employers are enhancing coverage for therapy, psychiatric medications, and digital mental health tools. A 2023 survey by the International Foundation of Employee Benefit Plans found that 72% of employers had expanded mental health offerings in the prior two years, reflecting a broader shift toward holistic employee well-being.

Telehealth has also become a standard feature of most employer-sponsored plans. What began as a pandemic-era necessity has evolved into a permanent fixture, with over 90% of large employers now offering virtual care options for primary care, mental health, and chronic disease management. These services are valued for their convenience and potential to reduce absenteeism, though questions remain about long-term utilization patterns and equity of access for employees with limited digital literacy or broadband access.

Legislative and regulatory changes continue to influence the employer coverage landscape. The Affordable Care Act’s employer mandate, which requires applicable large employers (those with 50 or more full-time equivalent employees) to offer affordable, minimum-value coverage or face penalties, remains in effect. In 2024, the IRS adjusted the affordability threshold for employer-sponsored coverage to 9.02% of household income (up from 8.39% in 2023), reflecting premium growth. This change affects how employers calculate whether their plans meet the “affordability” standard under the ACA.

State-level actions are also playing an increasing role. Some states, such as California and Novel York, have implemented laws requiring certain employers to provide paid sick leave or expand dependent coverage beyond federal minimums. Others are exploring reinsurance programs or premium subsidies to stabilize small-group markets. While these initiatives do not replace federal policy, they illustrate growing experimentation at the state level to address gaps in employer-based coverage.

The rise of non-traditional work arrangements presents a persistent challenge to the employer-sponsored model. Gig workers, freelancers, and those in temporary or contract roles often fall outside traditional employment definitions and are less likely to be offered benefits. Although some platforms have begun offering stipends or access to association health plans, coverage remains inconsistent and often inadequate. Policy proposals to decouple health insurance from employment — such as expanding public options or enhancing marketplace subsidies — continue to gain traction among advocates who argue the current system leaves too many workers behind.

For employees seeking to understand their options, the first step is reviewing the Summary of Benefits and Coverage (SBC) provided by their employer during open enrollment. This standardized document outlines costs, covered services, and limitations. The U.S. Department of Labor also offers resources through its Employee Benefits Security Administration (EBSA), including guidance on COBRA continuation coverage and ERISA rights. Workers who lose job-based coverage may qualify for a special enrollment period in the ACA marketplace, typically lasting 60 days from the loss of coverage.

Looking ahead, the sustainability of employer-sponsored insurance will depend on how well it adapts to economic pressures, workforce evolution, and changing expectations about health and work. Employers are increasingly viewing benefits not just as a cost but as a strategic tool for recruitment, retention, and productivity. Innovations in value-based design, chronic disease management, and preventive care incentives are being tested to improve outcomes while controlling expenses.

The next major data point on employer coverage trends will come from the Kaiser Family Foundation’s annual Employer Health Benefits Survey, typically released each fall. The 2025 edition is expected to be published in September or October 2025 and will provide updated figures on premiums, offer rates, and plan features. Until then, the March 2025 Current Population Survey data offers the most recent comprehensive snapshot of who holds employer-based coverage in the United States.

Understanding the nuances of employer-sponsored health insurance is essential for anyone navigating the U.S. Healthcare system. While it remains a cornerstone of coverage for millions, its limitations and inequities highlight the require for ongoing evaluation and reform. As work continues to evolve, so too must the systems designed to support workers’ health and economic security.

We welcome your thoughts and experiences with employer-based health coverage. Have you noticed changes in your plan’s costs, benefits, or accessibility? Share your perspective in the comments below, and consider sharing this article with colleagues or networks interested in healthcare policy and workplace benefits.

Related reading