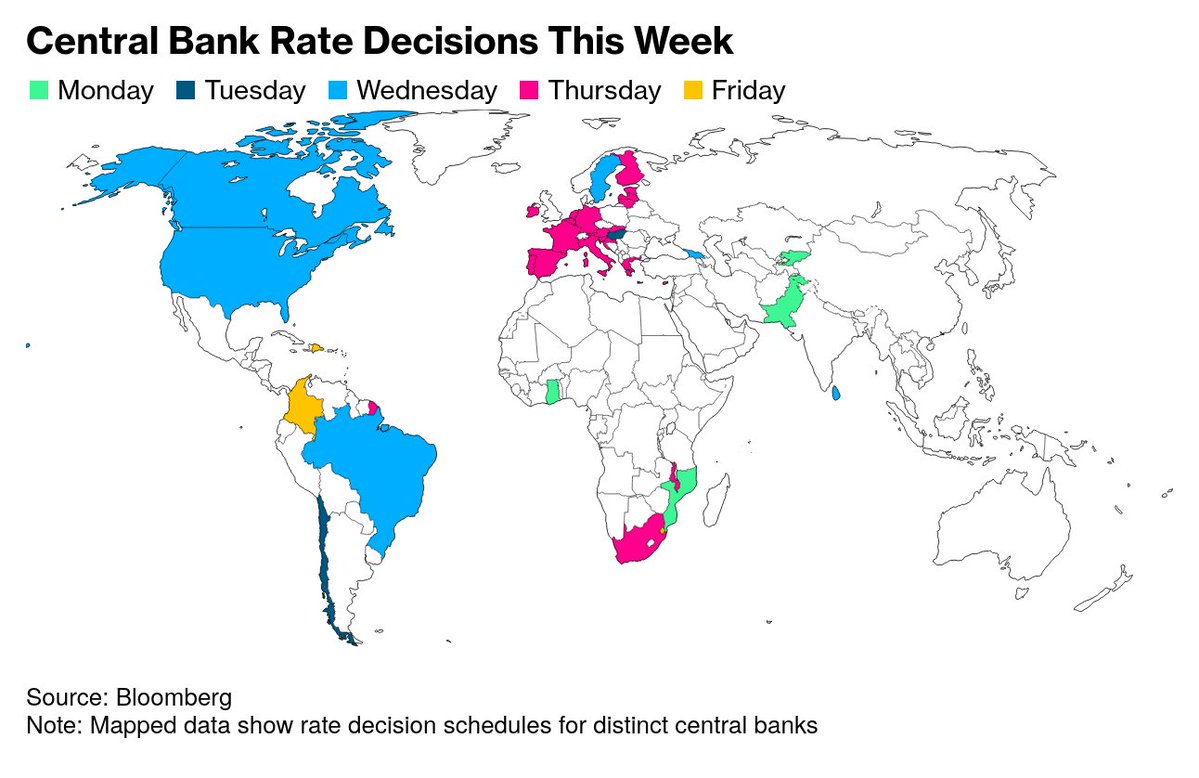

Central banks across the globe are preparing for a pivotal week of monetary policy decisions, with the Federal Reserve, European Central Bank, Bank of England and Bank of Japan all scheduled to announce their latest interest rate outlook between April 27 and April 29, 2026. This coordinated timing underscores the interconnected nature of global financial markets, where shifts in one major economy can ripple through others. As inflation pressures evolve and growth trajectories diverge, investors and policymakers alike are watching closely for signals about the future direction of monetary tightening or potential easing.

The Federal Reserve is set to conclude its two-day meeting on April 28, with Chair Jerome Powell expected to deliver a press conference outlining the U.S. Central bank’s stance on the federal funds rate. According to the latest data from Statista, the Fed has held its target range steady at 5.25%–5.50% since July 2023, marking the longest period without a change in over two decades. This pause has come amid mixed economic indicators, including persistent services inflation and a labor market showing signs of gradual cooling.

Meanwhile, the European Central Bank will announce its decision on April 29, following its Governing Council meeting. The ECB has maintained its main refinancing rate at 4.50% since September 2023, after a series of aggressive hikes aimed at curbing inflation that peaked above 10% in late 2022. Recent data shows eurozone inflation has eased to 2.4% as of March 2026, moving closer to the ECB’s 2% target, though core inflation remains stubbornly above 3%, prompting caution among policymakers.

The Bank of England is also scheduled to reveal its policy decision on April 29, with Bank Rate currently held at 5.25% after a series of increases from near-zero levels in late 2021. UK inflation has declined to 2.8% in the latest reading, but wage growth and services prices continue to exert upward pressure. Governor Andrew Bailey has emphasized that any future rate cuts will be data-dependent and gradual, reflecting concerns about second-round effects from persistent inflation in non-energy sectors.

In Asia, the Bank of Japan will conclude its policy meeting on April 28, maintaining its negative interest rate policy and yield curve control framework despite being the last major central bank to retain such accommodative measures. The BOJ has kept its short-term interest rate at -0.1% and continues to target 10-year government bond yields around 0%, a stance justified by Japan’s persistently low inflation and sluggish wage growth, though recent signs of price increases in services and tourism have sparked debate about a potential policy shift.

These concurrent decisions highlight the diverging paths of monetary normalization among advanced economies. While the Fed, ECB, and BoE are navigating the final stages of tightening cycles after years of historic rate hikes, the BOJ remains an outlier, still grappling with the challenge of achieving sustainable inflation above target without undermining fragile economic recovery. Market analysts note that any divergence in policy paths—particularly if the Fed signals cuts while the BOJ holds or tightens—could trigger significant movements in currency markets, especially the dollar-yen and euro-dollar exchange rates.

For global markets, the implications extend beyond interest rates. Currency fluctuations, bond yield spreads, and equity valuations are all sensitive to shifts in central bank tone. A more hawkish-than-expected stance from any of these institutions could strengthen its currency and pressure emerging markets with dollar-denominated debt. Conversely, signs of coordinated easing could boost risk appetite and lift global equities, though analysts warn that premature optimism could rekindle inflation fears if not grounded in sustained economic data.

Looking ahead, the next major checkpoint for global monetary policy will be the Federal Reserve’s June 10–11, 2026 meeting, followed by the ECB and BOE gatherings in mid-June. The Bank of Japan is expected to maintain its current schedule with a policy meeting in June as well. These upcoming decisions will provide further clarity on whether the recent trend toward policy divergence continues or if converging economic pressures lead to a more synchronized approach among the world’s most influential central banks.

Stay informed about these developments by visiting the official websites of the Federal Reserve (Federal Reserve), European Central Bank (European Central Bank), Bank of England (Bank of England), and Bank of Japan (Bank of Japan) for official statements, meeting minutes, and economic projections. Share your thoughts on how these decisions might affect your region or investments in the comments below, and help others understand the global implications by sharing this article.