The Financial Services Commission (FSC) of South Korea continues to emphasize the importance of financial literacy, specifically regarding the mechanics of personal lending and debt management. Through its ongoing “Financial Life Talk” series, the regulatory body aims to clarify how various loan products, repayment structures, and credit management strategies impact the long-term financial health of consumers. Understanding these foundational concepts is essential for individuals navigating both formal banking systems and the risks posed by illegal lending practices, according to official guidance from the Financial Services Commission.

For many consumers, the distinction between credit-based loans and collateralized debt remains a primary point of confusion. The FSC notes that credit loans are generally granted based on an individual’s repayment capacity and credit score, while collateralized loans—such as mortgages—require an asset to be pledged as security. According to the Financial Supervisory Service (FSS), which works in tandem with the FSC to monitor market stability, consumers must carefully evaluate their debt-to-income ratios before committing to long-term repayment schedules. Failure to manage these obligations can lead to significant credit impairment and financial distress.

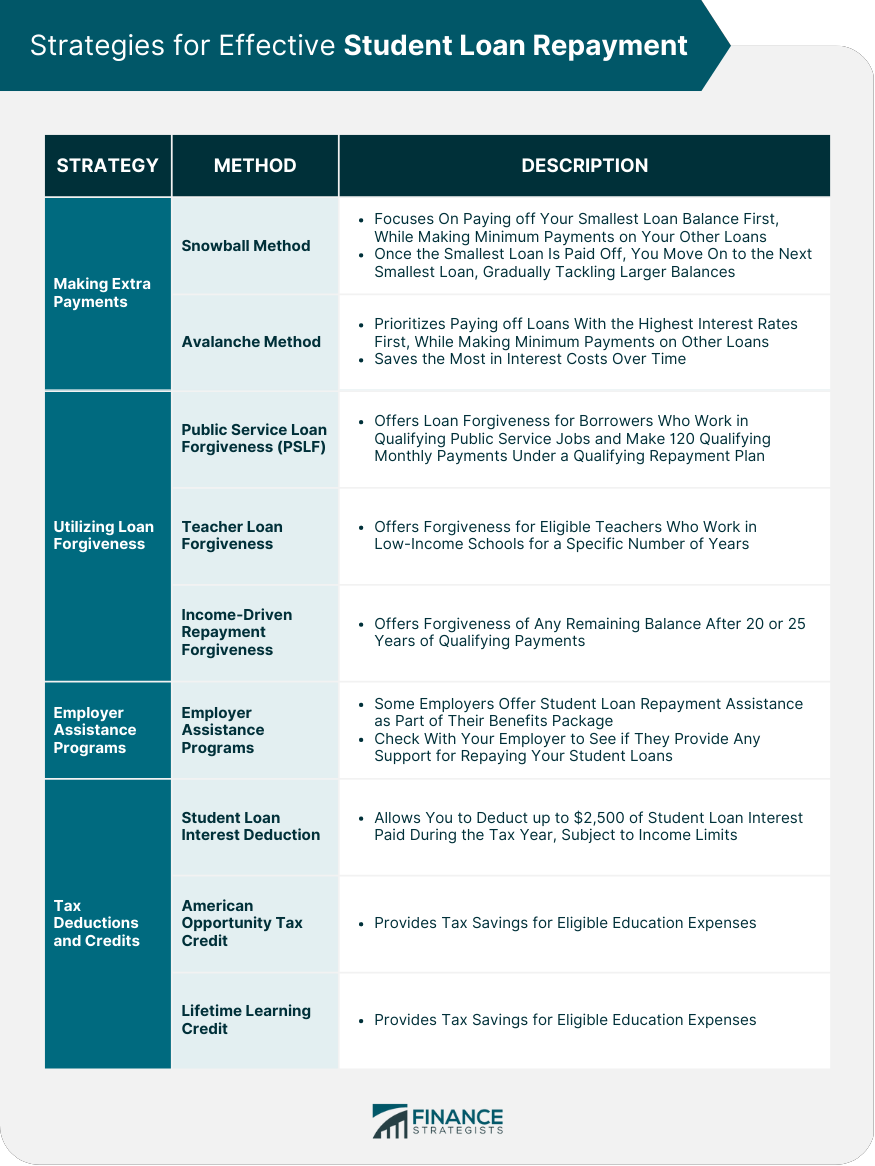

Understanding Loan Repayment Methods

Selecting an appropriate repayment method is as critical as securing the loan itself. Borrowers typically encounter three standard structures: lump-sum repayment at maturity, equal installment payments of principal and interest, and equal principal repayment. The FSC highlights that while lump-sum repayment may offer lower monthly costs initially, the full balance due at the end of the term can pose a liquidity risk for many households. Conversely, installment plans help spread the financial burden, though they require a disciplined monthly budget.

The Financial Supervisory Service advises that borrowers should verify the total cost of interest over the life of the loan before signing any agreement. By utilizing official online calculators provided by financial institutions, applicants can better predict how different interest rate environments—whether fixed or variable—will affect their total debt obligation. This level of transparency is a core objective of the regulatory framework designed to protect retail investors and borrowers from predatory terms.

Mitigating Risks of Illegal Lending

A significant portion of the FSC’s consumer protection mandate involves the prevention of illegal private lending. Consumers are frequently warned against entities that operate outside the scope of authorized financial institutions. The FSC defines illegal private lending as any financial transaction conducted by unregistered entities that often employ coercive collection tactics or charge interest rates that exceed the legal maximum set by the Interest Limitation Act.

To ensure personal safety and financial security, the government recommends the following steps when seeking credit:

- Verify the registration status of any lender through the official government portal before sharing personal financial information.

- Avoid platforms that guarantee loans regardless of credit history, as these are common hallmarks of fraudulent schemes.

- Report suspicious activities, such as aggressive debt collection or requests for upfront fees, to the Financial Supervisory Service reporting center.

The Role of Credit Management

Your credit score serves as the primary metric for determining the interest rates and borrowing limits available to you in the formal financial sector. The FSC emphasizes that maintaining a positive credit profile involves more than just timely payments; it includes managing the number of open accounts and avoiding excessive utilization of credit lines. According to the Korea Credit Bureau and other reporting agencies, even minor discrepancies in credit reporting can be corrected through official dispute channels, ensuring that a borrower’s financial reputation remains accurate.

As the economic landscape shifts, the FSC remains committed to providing updated guidance through its digital initiatives. For those seeking the most recent policy changes or specific advisories, the FSC Press Release section serves as the primary source for verified regulatory updates. Readers are encouraged to monitor these official channels and participate in the ongoing conversation regarding financial stability. Those interested in further analysis or who have questions regarding current lending regulations are welcome to share their thoughts or inquiries in the comments section below.