Financial security for elderly individuals often relies on the vigilance of both families and the institutions entrusted with their assets. Recent reports concerning cases where senior citizens unexpectedly receive multiple credit cards they did not request have highlighted significant concerns regarding banking oversight and consumer protection. When an individual, particularly a senior with limited digital literacy or no history of using modern banking tools like ATM cards, suddenly finds themselves liable for multiple lines of credit, the emotional and financial toll on the family can be profound.

As families grapple with the complexities of managing the financial affairs of aging relatives, these incidents serve as a sobering reminder of the importance of proactive account monitoring. Navigating the aftermath of unauthorized financial activity requires a clear understanding of consumer rights and the specific steps necessary to rectify errors with financial institutions. For those impacted, the process involves immediate communication with banks to dispute unauthorized charges and secure vulnerable accounts against further exploitation.

Understanding Consumer Protections and Fraud Prevention

In the United Kingdom and internationally, financial institutions are governed by strict regulatory frameworks designed to protect consumers from unauthorized account openings and fraudulent activity. According to the Financial Conduct Authority (FCA), customers have clear rights when it comes to disputing transactions they did not authorize. When a consumer discovers that a credit card account has been opened in their name without their consent, they are encouraged to contact the issuing bank immediately to file a formal dispute.

The rise in sophisticated financial scams necessitates a multi-layered approach to protection. Families acting on behalf of elderly relatives should regularly review bank statements and credit reports to identify any irregularities. If a discrepancy is found, documenting every communication with the bank—including the names of representatives, dates of calls, and reference numbers for complaints—is essential for resolving the issue efficiently. Consumers can find guidance on identifying and reporting various forms of financial fraud through official resources like the USA.gov scam reporting tool, which helps direct individuals to the appropriate agencies based on the nature of the incident.

Steps to Take Following Unauthorized Account Activity

If you or a family member suspects that an account has been opened fraudulently, time is of the essence. The following steps are recommended by consumer protection experts to mitigate potential damages:

- Contact the Issuing Institution: Reach out to the bank or credit card issuer immediately. Request that the unauthorized accounts be closed and flagged as fraudulent.

- Request a Fraud Investigation: Formally request that the bank investigate the origin of the application. This is a critical step in clearing the victim’s credit history.

- Monitor Credit Reports: Regularly check credit reports from major bureaus to ensure no other accounts have been opened under the individual’s identity.

- Report to Authorities: If identity theft is suspected, file a report with local law enforcement or the relevant national consumer protection agency, such as the Federal Trade Commission (FTC) in the United States, to create an official record of the incident.

It is important to remember that banks have a duty of care to verify the identity of their applicants. If a bank has failed to implement robust Know Your Customer (KYC) procedures, the burden of proof regarding the unauthorized nature of the account should rest with the institution. Documentation, such as a lack of prior interaction with the bank or evidence that the senior citizen does not possess or use the technology required to apply for such cards, can be vital evidence in a dispute.

The Role of Family Advocacy

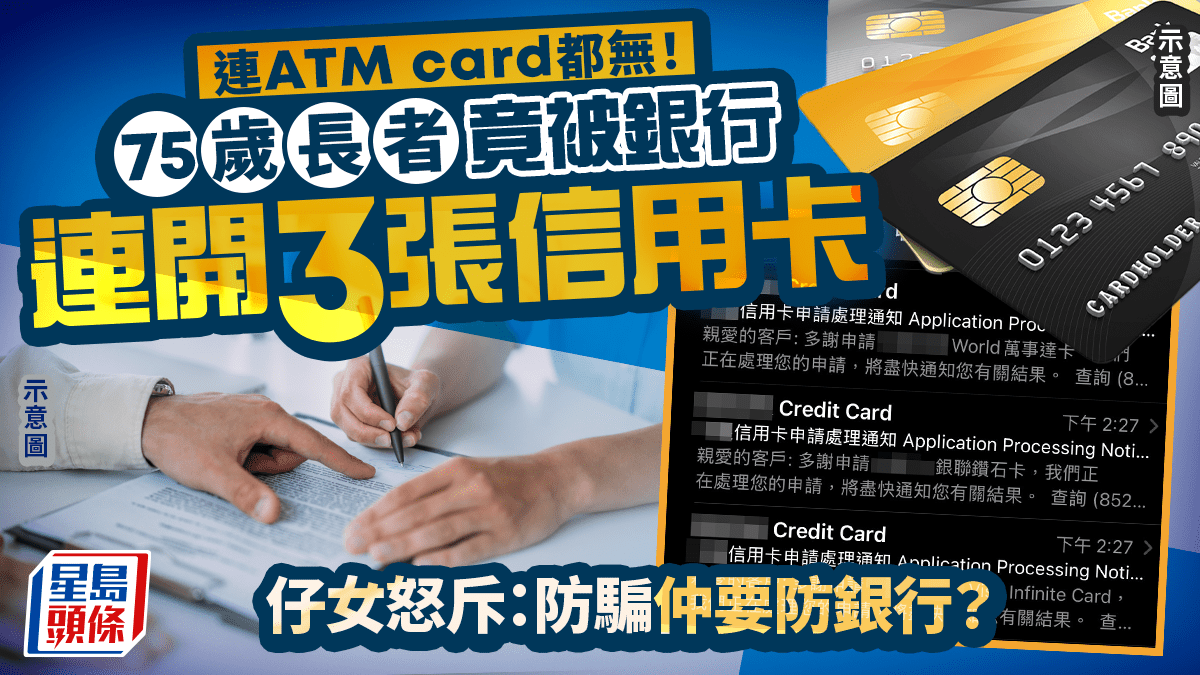

The frustration expressed by family members who discover such errors is often rooted in the perceived failure of institutions to protect their most vulnerable clients. When a 75-year-old who has never even used an ATM card is suddenly issued multiple credit cards, it raises questions about the rigor of the bank’s internal security checks. Advocacy from family members is often the catalyst for getting these errors corrected, as they can navigate the bureaucratic channels that may be overwhelming for the elderly account holder.

For those currently managing the finances of an aging parent or relative, maintaining open communication with the bank is paramount. By establishing a Power of Attorney where appropriate, families can gain the legal authority to monitor accounts more closely and intervene before fraudulent activity escalates. Ensuring that elderly relatives are aware of common scam tactics—such as individuals impersonating bank officials—further strengthens the protective barrier around their assets.

Looking Ahead: Ensuring Institutional Accountability

As the global financial landscape continues to digitize, the risk of identity theft and administrative errors remains a persistent challenge. Regulatory bodies are increasingly focusing on the responsibilities of banks to safeguard elderly customers. Future updates from financial ombudsmen and regulatory authorities will likely continue to emphasize the need for enhanced verification processes for credit card applications. Readers are encouraged to stay informed through official updates from their local financial regulatory bodies.

If you have experienced similar issues, the first step is always to secure your financial records and initiate a formal complaint process with the institution involved. Share your experiences in the comments below to help others stay vigilant, and ensure you are subscribed to our newsletter for the latest updates on consumer rights and financial security.

Worth a look